If you want investment income without picking individual stocks, a dividend ETF is one of the simplest tools available. It bundles dozens or hundreds of dividend-paying companies into a single fund, then passes the income on to you. But “high yield” can mean very different things — a steady 3% grower behaves nothing like a 10% covered-call fund. This guide to the best high-yield dividend ETFs for 2026 breaks down five popular funds, how they generate income, and how to choose the one that fits your goals.

What Counts as a “High-Yield” Dividend ETF?

A dividend ETF’s yield is the income it pays over a year divided by its share price. Broadly, there are two ways a fund pushes that number higher. The first is simply holding stocks that pay above-average dividends, like utilities, energy, and financials. The second is layering an options strategy — usually covered calls — on top of a stock portfolio to manufacture extra income.

That distinction matters more than the headline percentage. A traditional high-dividend fund yielding 3% can still grow your income every year as companies raise their payouts. A covered-call fund yielding 9% delivers more cash today, but typically caps how much you gain when the market rallies. Neither is “better” in the abstract; they solve different problems.

How to Choose a Dividend ETF: 4 Things That Matter

Before comparing tickers, it helps to know which numbers actually drive your long-term result. Four factors do most of the work.

1. Dividend Yield (Income Today)

Yield tells you how much income you collect right now relative to what you invest. A higher yield is not automatically safer or better — unusually high yields can signal extra risk or a strategy that trades away future growth for present cash. Read yield alongside, not instead of, the points below.

2. Expense Ratio (What You Pay)

The expense ratio is the annual fee the fund charges, taken quietly out of returns. The gap between a 0.04% and a 0.35% fund may look trivial, but on a long-held position it compounds into real money. Index-tracking dividend ETFs are usually the cheapest; actively managed, options-based funds cost more.

3. Dividend Growth and Quality

A fund that screens for financially strong companies with a record of raising dividends tends to deliver a rising income stream over time. That growth is easy to overlook because today’s yield looks modest, yet a payout that climbs year after year can overtake a flashier static yield within a decade.

4. Taxes and Account Type

Where you hold a dividend ETF affects how much you keep. Qualified dividends from traditional dividend funds are taxed at favorable long-term rates, while income from covered-call funds is often taxed less efficiently. As a rule of thumb, options-income funds frequently fit better inside tax-advantaged accounts. If you are still building the foundation, our beginner’s guide to asset allocation shows where dividend ETFs sit alongside the rest of your portfolio.

The Best High-Yield Dividend ETFs for 2026: 5 Top Picks

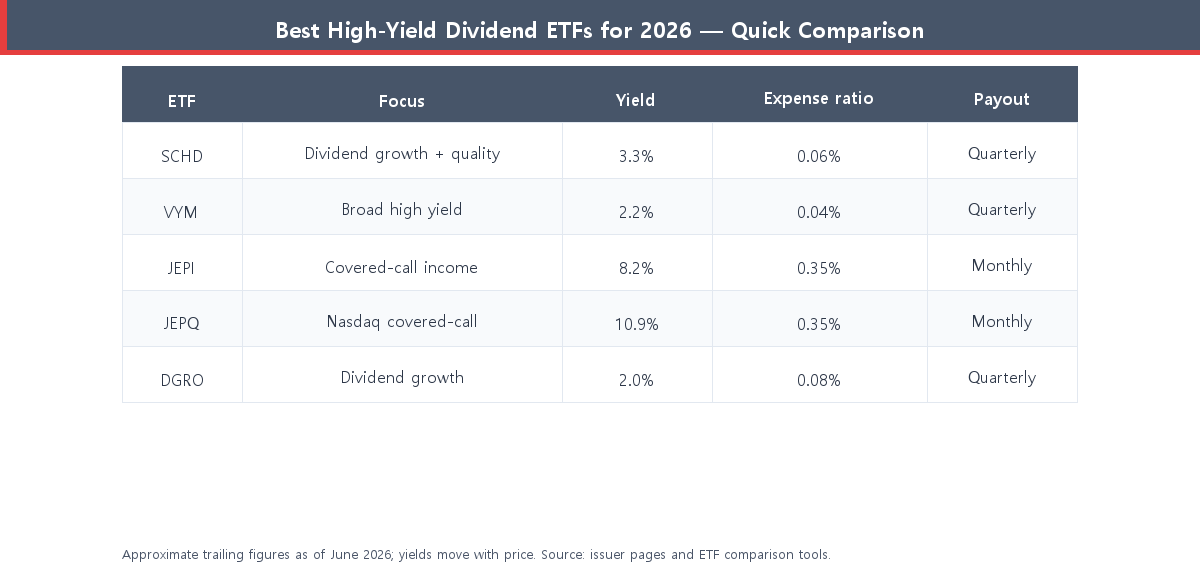

The table below compares five of the most widely held dividend ETFs on the metrics that matter: focus, trailing yield, expense ratio, and how often they pay. Figures are approximate trailing numbers as of mid-2026 and will move with markets.

SCHD — Best All-Around Dividend Grower

The Schwab U.S. Dividend Equity ETF (SCHD) tracks about 100 quality U.S. companies screened for financial strength and consistent payouts. With a yield near 3.3%, a rock-bottom 0.06% fee, and a strong record of double-digit annual dividend growth, it is widely treated as the default core dividend holding. The trade-off is a lower starting yield than the covered-call funds.

VYM — Cheapest Broad High-Yield Fund

The Vanguard High Dividend Yield ETF (VYM) holds more than 500 dividend-paying U.S. stocks and charges just 0.04%, the lowest fee on this list. Its yield sits around 2.2%, but the very broad diversification and minimal cost make it a low-maintenance choice for investors who want simplicity over a headline number.

JEPI — High Monthly Income From Covered Calls

The JPMorgan Equity Premium Income ETF (JEPI) is actively managed and writes covered calls on a defensive stock portfolio to generate income paid every month. That pushes its yield to roughly 8%, far above traditional dividend funds. The catch: the options overlay caps upside, so in a strong bull market JEPI will likely lag a plain stock index.

JEPQ — Highest Yield, Tech-Tilted

JEPQ applies the same covered-call approach to a Nasdaq-100-style portfolio, producing the highest reported yield here — near 11% — also paid monthly. The higher income comes with more concentration in technology names and the same capped-upside trade-off. It suits investors who prioritize current cash flow and accept extra volatility.

DGRO — A Dividend-Growth Core Holding

The iShares Core Dividend Growth ETF (DGRO) emphasizes companies that consistently raise dividends rather than those with the highest current yield. At roughly a 2% yield and a 0.08% fee, it is less about income today and more about a steadily rising payout — a natural complement to higher-yielding funds.

The video below walks through why SCHD remains a popular core dividend pick heading into 2026 and what to watch.

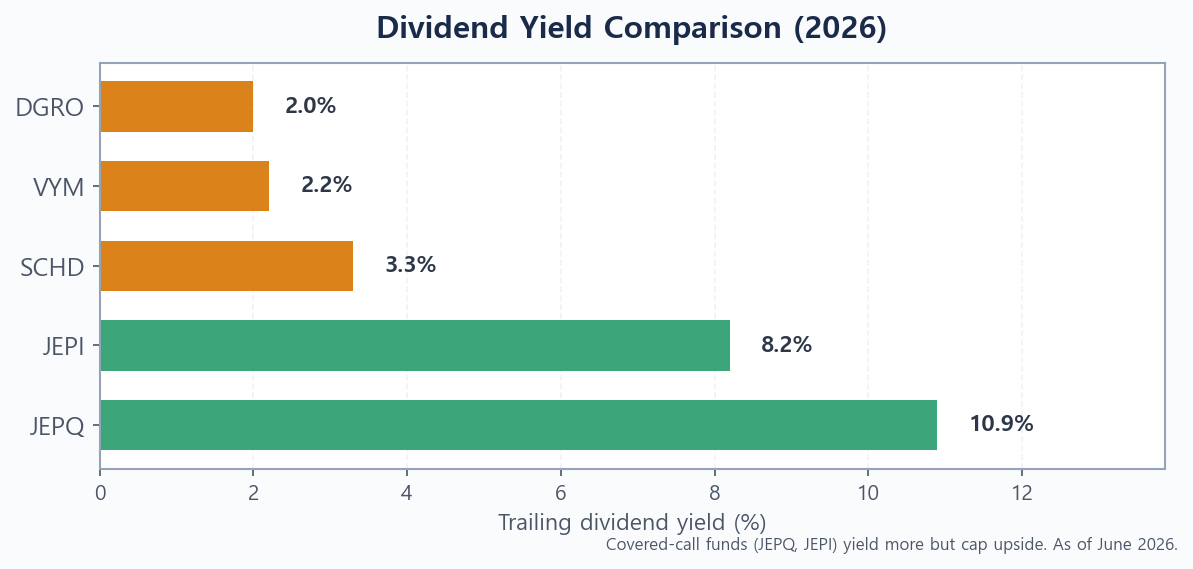

Yield vs. Cost: Comparing the Numbers

Yield is the first thing most people look at, so it is worth seeing the spread side by side. The covered-call funds (JEPI and JEPQ) sit far above the traditional dividend funds — but remember that gap reflects a different strategy, not free money.

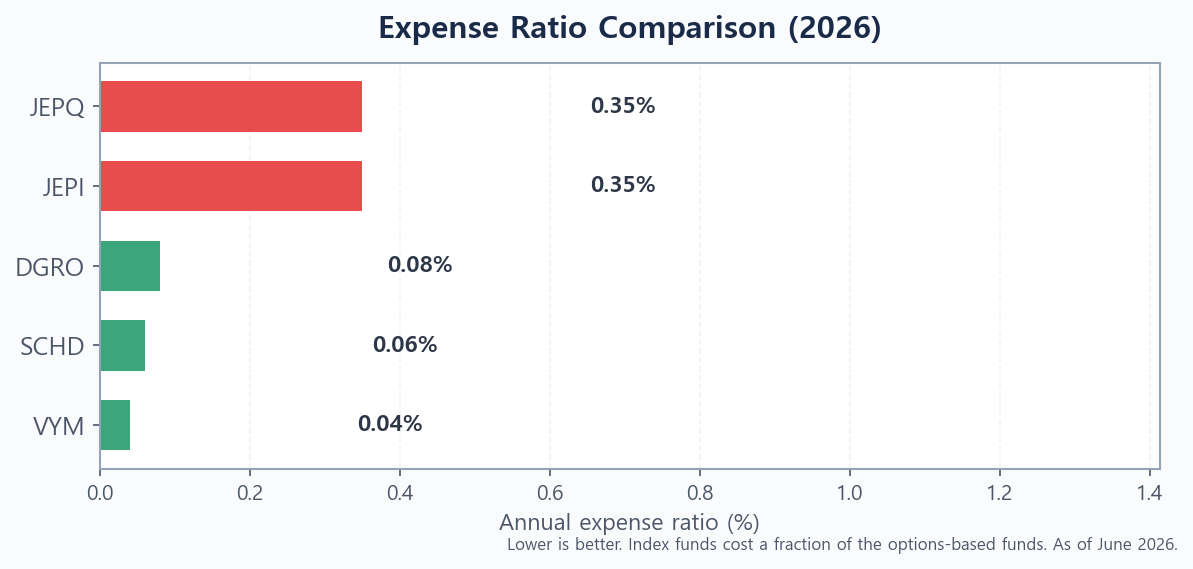

What You Pay: Expense Ratios

Fees tell the opposite story. The index funds cost a small fraction of the actively managed, options-based funds. Over many years, that difference is a real headwind the higher-fee funds must overcome with performance.

(Source: fund yield and expense-ratio data compiled from issuer pages and ETF comparison tools, as of June 2026.)

Which Dividend ETF Is Right for You?

If you have a long horizon and want a growing income stream, a quality dividend-growth fund like SCHD or DGRO usually makes the most sense — you accept a lower yield today in exchange for payouts that compound. If you need maximum cash flow now, for example in retirement, the monthly income from JEPI or JEPQ can be attractive, provided you understand the capped upside and hold them in a tax-smart account.

Many investors blend both: a low-cost growth fund as the foundation, with a slice of covered-call income on top. If you are just getting started, see our walkthrough on how to start investing with only $100, and if you are weighing income options beyond stocks, compare them with short-term bonds vs. high-yield savings.

Final Thoughts

The best high-yield dividend ETFs for 2026 are not a single winner but a small toolkit: SCHD and DGRO for growing income, VYM for cheap broad exposure, and JEPI or JEPQ for high monthly cash flow. Match the fund to your goal, weigh yield against fees and tax treatment, and resist chasing the biggest number for its own sake. Found this useful? Bookmark it so you can revisit when you rebalance.

This article is for informational purposes only and is not investment advice. Do your own research before making any investment decision.