Eight times a year, a small committee in Washington announces a number — and within seconds, trillions of dollars in stock value can move. That number is the federal funds rate, and the way a Fed rate decision affects the stock market is one of the most important relationships in investing to understand. The connection is real, but it is also widely misunderstood: stocks do not simply rise when the Fed cuts and fall when it hikes. This guide walks through the actual channels that link the Fed to your portfolio, where rates stand in 2026, and what a long-term investor should genuinely do about any of it.

What the Fed Actually Decides — and Why Markets Care

The Federal Reserve (the “Fed”) is the central bank of the United States. At each meeting of its Federal Open Market Committee (FOMC), it sets a target range for the federal funds rate — the interest rate banks charge one another for overnight loans. The Fed does not set mortgage rates or stock prices directly, but this single benchmark ripples outward into almost every borrowing cost in the economy, from credit cards to corporate debt.

Markets care because that ripple eventually reaches corporate profits and the value investors place on those profits. Just as important, investors care about the Fed’s guidance — the signals it gives about where rates are headed next. Often the words in the press conference move stocks more than the rate change itself.

The Four Channels: How Rate Decisions Move Stocks

A rate decision does not affect share prices through magic. It travels through four fairly mechanical channels, each of which can push stocks up or down.

1. Borrowing costs and corporate profits

When rates rise, companies pay more to borrow for expansion, equipment, and refinancing existing debt. Higher interest expense eats into profits and can slow growth plans. When rates fall, borrowing gets cheaper, which can free up cash for investment and support earnings.

2. The discount rate on future earnings

A stock’s price is, in theory, the value today of all the profits a company will earn in the future. To convert future profits into a present value, investors “discount” them using prevailing interest rates. Higher rates mean a steeper discount, so distant future earnings are worth less today — which is why high-growth, long-duration stocks (think unprofitable tech) often fall hardest when rates rise. Lower rates do the reverse.

3. Competition from bonds and cash

Stocks always compete with safer alternatives. When the Fed holds rates high, a Treasury bill or savings account paying around 4% looks attractive next to the national average savings rate of roughly 0.6% (Source: Bankrate, as of June 2026). That pulls some money out of stocks. When rates fall, those safe yields shrink and cash becomes less appealing, nudging investors back toward equities.

4. Sector rotation

Rate moves do not hit every stock equally. Financials, value stocks, and cyclicals often hold up better — or even benefit — when rates rise, while growth-focused and income-oriented stocks tend to do relatively better when rates fall (Source: U.S. Bank / Nasdaq, 2026). This is why a single Fed decision can lift one part of the market while pressuring another.

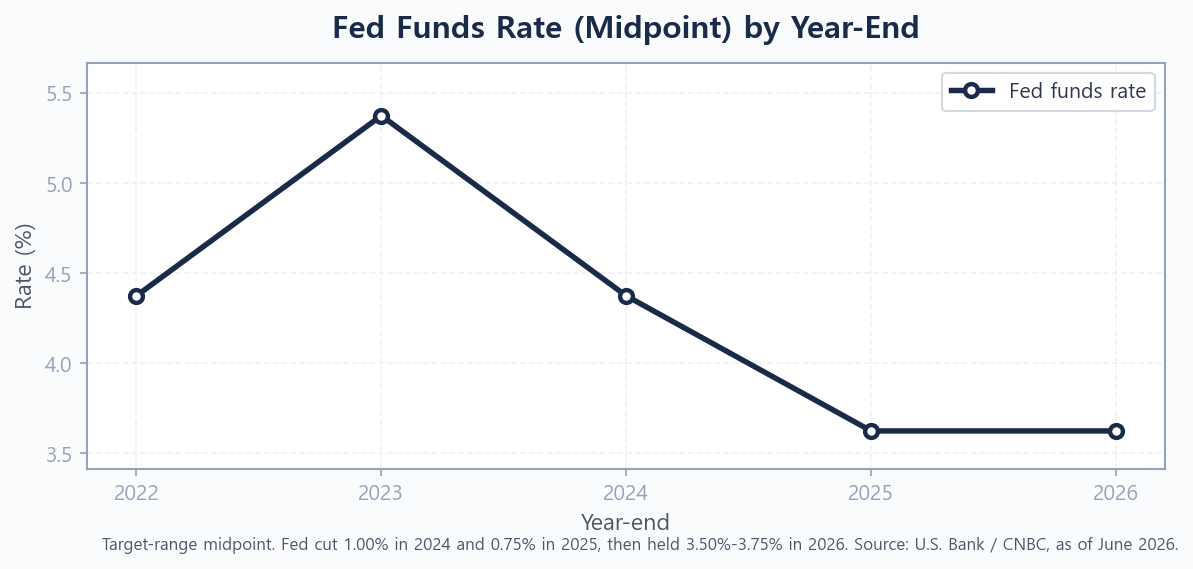

Where Fed Rates Stand in 2026

Context matters, because the same rate decision lands differently depending on where rates already are. After an aggressive hiking cycle, the Fed cut rates by a full 1.00% in 2024 and another 0.75% in 2025. It then held its target range at 3.50%–3.75% through its first meetings of 2026, with markets pricing in roughly one possible additional cut this year as inflation risks linger (Source: U.S. Bank / CNBC, as of June 2026).

The chart shows the arc clearly: a sharp climb into 2023, a steady descent through 2024 and 2025, and a plateau in 2026. For investors, the key takeaway is that we are no longer in an emergency-policy environment in either direction — which is part of why markets have grown more sensitive to the Fed’s tone than to any one move. To see where this “macro” picture fits into a real portfolio, read our beginner’s guide to asset allocation.

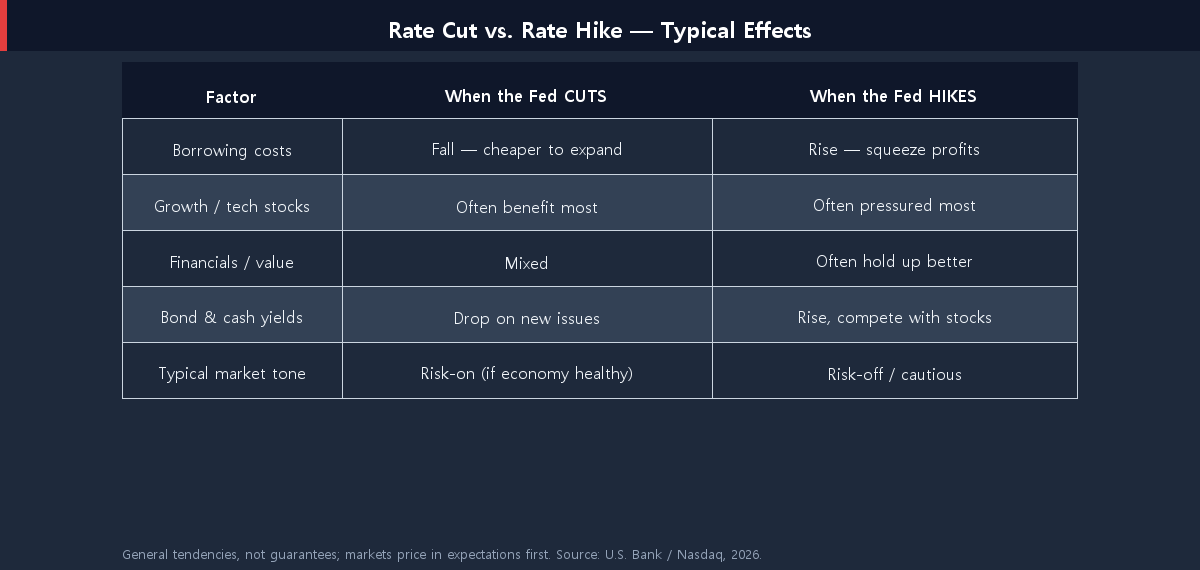

Cuts vs. Hikes: What Each Means for Your Portfolio

It helps to line up the two directions side by side. The table below summarizes the typical tendencies — not guarantees, because markets price in expectations long before decisions land.

Notice that income-generating assets sit on both sides of this table. When rates fall, the yields on new bonds and savings drop, which is when reliable equity income gets more valuable — one reason many investors look at the best high-yield dividend ETFs for 2026. When rates are high, by contrast, the case for parking cash strengthens, as covered in short-term bonds vs. high-yield savings.

Why the Market Sometimes Falls on a Rate Cut

Here is the part that confuses most people. If lower rates are good for stocks, why do shares sometimes drop on the very day the Fed cuts? The answer is expectations. Markets are forward-looking machines: by the time a decision is announced, traders have usually spent weeks betting on the outcome, and that expectation is already baked into prices — the market has “priced it in.”

What actually moves stocks is the surprise relative to those expectations. A few examples:

- A cut that was fully expected may cause little reaction — or even a sell-off if investors hoped for a bigger cut.

- A “hawkish cut,” where the Fed lowers rates but signals fewer cuts ahead, can disappoint markets even though rates went down.

- Why the Fed is cutting matters too. Cuts aimed at supporting a healthy economy are welcomed; emergency cuts during a downturn can signal trouble and unsettle investors.

This is why trying to trade around Fed meetings is so difficult: you are not betting on the decision, but on how the decision compares to what everyone else already assumed.

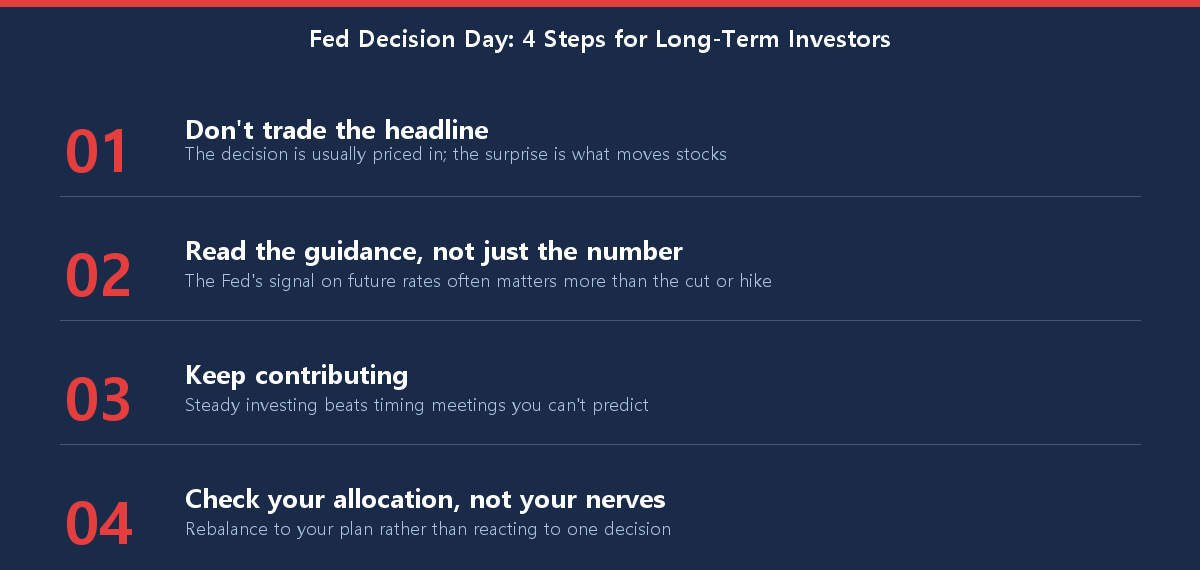

What Long-Term Investors Should Actually Do

For anyone investing on a horizon of years rather than days, the practical answer is reassuringly boring. The Fed sets the backdrop, but it should rarely drive your buy-and-sell decisions. Use the checklist below as a calm-headed routine for Fed weeks.

The investors who do best around Fed decisions are usually the ones who do the least. Stock performance rarely depends on a single variable — earnings, valuations, fiscal policy, and global events all share the stage with the Fed (Source: U.S. Bank, 2026). If you are still building the habit of investing through the noise, how to start investing with only $100 is a useful next step.

Conclusion: The Fed Sets the Weather, Not Your Destination

Understanding how a Fed rate decision affects the stock market turns a scary headline into something you can reason about. Rates move stocks through borrowing costs, the discount applied to future earnings, competition from cash and bonds, and rotation between sectors — but markets trade on expectations, which is why the reaction so often defies the simple “cut good, hike bad” story. In 2026, with rates plateauing in the 3.50%–3.75% range, the Fed remains a powerful force on market weather. Your destination, though, is still set by a sensible plan and the patience to stick with it.

Found this useful? Bookmark it and revisit on the next Fed decision day — the context here holds up no matter which way rates move.

This article is for informational purposes only and is not investment advice. Do your own research.