You have a meaningful pile of cash to invest — a bonus, an inheritance, a maturing deposit, or a 401(k) rollover — and one nagging question: put it all in today, or feed it into the market a little at a time? That is the dollar-cost averaging vs. lump-sum investing debate, and in 2026 it matters as much as ever with markets near record highs and headlines warning of the next pullback. The honest answer is backed by decades of data, and it is probably not the one your gut wants to hear.

The Two Strategies in Plain English

Lump-sum investing means putting your entire available amount to work at once. If you have $60,000, it all goes into your chosen funds today, at today’s prices.

Dollar-cost averaging (DCA) means splitting that same amount into equal slices and investing them on a fixed schedule — say, $10,000 a month for six months, or $5,000 a month for a year — regardless of what the market is doing. By buying at different prices, you smooth out your average entry point and avoid putting everything in on a single unlucky day.

One important distinction: this debate is only about money you already have. Investing each paycheck as it arrives is not DCA — that is simply investing as you earn, and it is the right move for almost everyone. The real choice is what to do with a sum that is sitting in cash right now.

What the Data Says: Lump-Sum Usually Wins

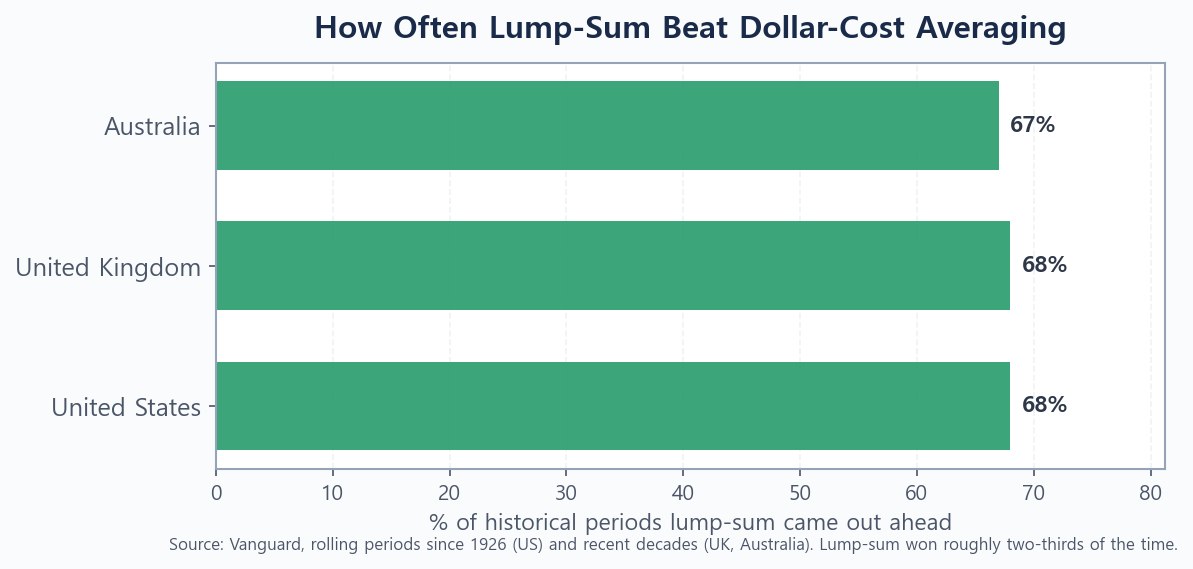

Vanguard ran the definitive study on this, comparing the two approaches across rolling historical periods in the United States going back to 1926, plus more recent decades in the United Kingdom and Australia. The result was consistent across all three markets: investing a lump sum immediately beat dollar-cost averaging roughly two-thirds of the time.

When lump-sum won, it also won by a useful margin — on average about 2.3% more wealth after 10 years for a balanced portfolio. The study also found a clear pattern: the longer you stretch out the DCA window, the worse DCA tended to perform. Spreading purchases over 12 months lagged more than spreading them over 6. The video below from analyst Ben Felix walks through the same evidence and the psychology behind it.

Why Lump-Sum Comes Out Ahead More Often

The logic is simple once you state it. Markets rise more often than they fall. The S&P 500 has finished higher in roughly three of every four calendar years over the long run. If the market is more likely to be up than down on any given day, then the sooner your money is invested, the more days it spends growing. Cash held back to “average in” spends those days earning little, missing the dividends and compounding it could have captured.

In other words, dollar-cost averaging only wins when the market falls during your rollout — when your later, cheaper purchases drag your average price down. That happens, but historically it is the minority case. Holding cash on the sidelines is itself a bet that prices will be lower later, and that bet loses most of the time.

When Dollar-Cost Averaging Makes Sense

None of this makes DCA a mistake. It is a deliberate trade: you give up some expected return in exchange for a smoother emotional ride and protection against the worst-case timing. That trade can be the right one in a few situations:

- You would panic-sell after a drop. A 20% fall the week after you invest everything could shake you out of the market entirely. If DCA is what keeps you invested at all, its lower expected return beats abandoning stocks.

- The sum is huge relative to your net worth. Going all-in with money you cannot afford to see fall sharply is a risk-management question, not just a returns question.

- You are genuinely unsure of your your overall asset allocation. Spreading entry over a few months buys time to settle on a stock/bond mix you can hold for years.

Crucially, both DCA and lump-sum investing handily beat the third option people actually choose: leaving the money in cash while waiting for a “better” moment. The gap between the two strategies is modest; the gap between either of them and doing nothing is enormous.

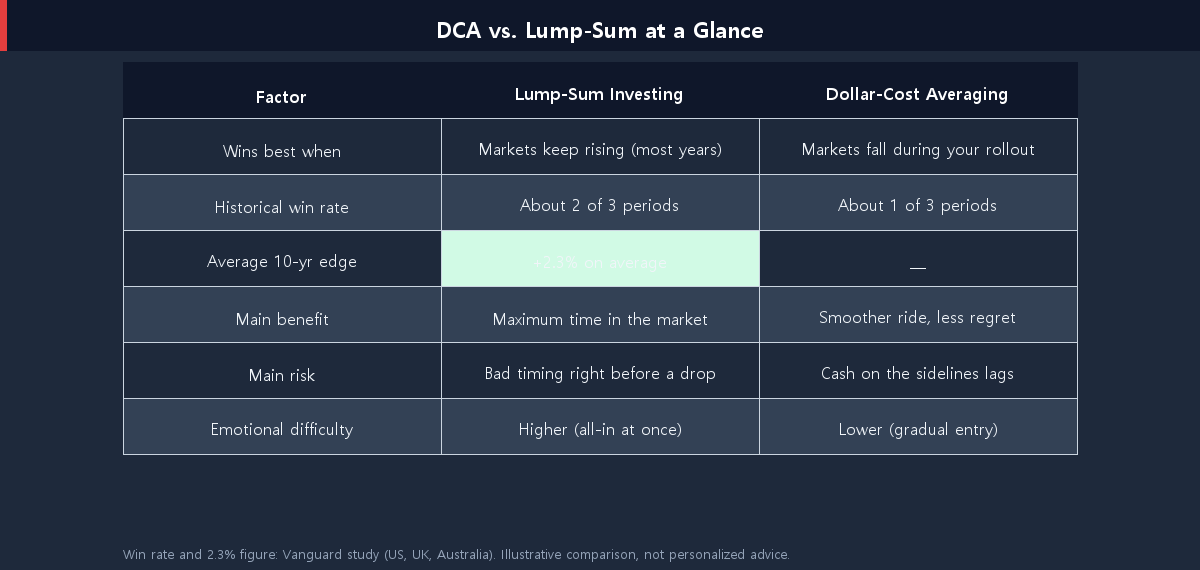

Head-to-Head: DCA vs. Lump-Sum at a Glance

The table below summarizes how the two strategies compare on the factors that matter most when you are deciding what to do with cash in 2026.

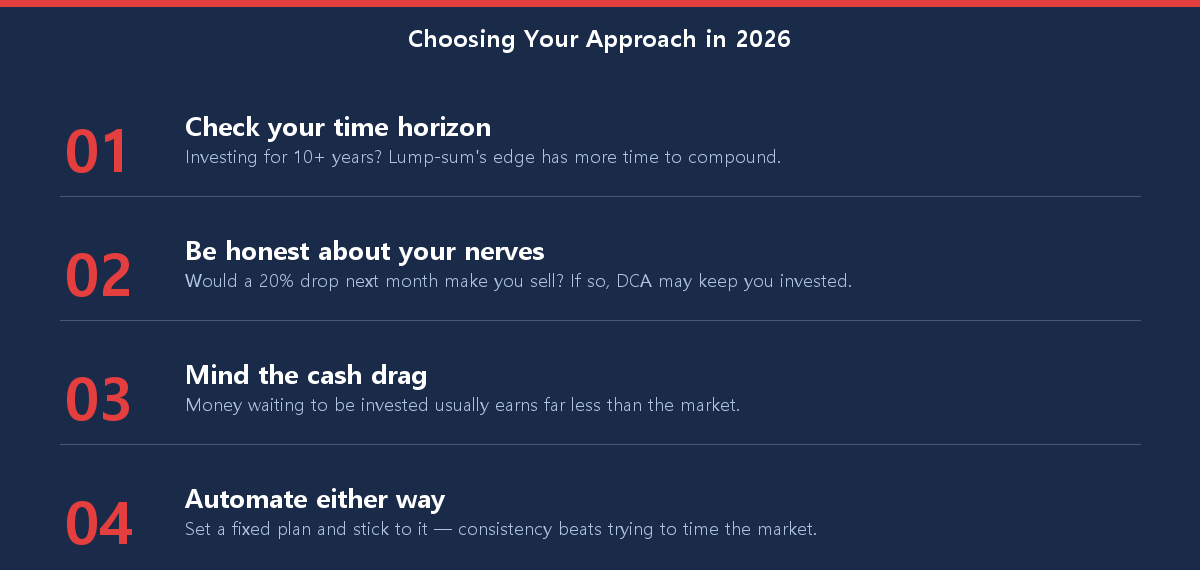

How to Decide in 2026

There is no need to overthink this. Your time horizon and your temperament settle most of the question. If you are investing for a decade or more and can stomach short-term swings, the math favors putting the money in now. If the thought of a sharp drop right after investing would keep you up at night, a short DCA schedule — three to six months, not several years — is a reasonable compromise. Whichever route fits, the key is to automate it; you can even start small while you build the habit, as we cover in our guide to starting with as little as $100.

Conclusion: The Best Strategy Is the One You’ll Stick With

So which wins in 2026? On the numbers, lump-sum investing wins about two of every three times and by a meaningful margin, because time in the market beats timing the market. But dollar-cost averaging remains a sensible choice for anyone who would otherwise freeze or sell in a downturn — a smaller expected return is far better than a portfolio you abandon. The worst strategy of all is the one that feels safest: leaving the cash uninvested. Pick the approach that gets your money working and lets you sleep at night, then let compounding do the rest.

Found this dollar-cost averaging vs. lump-sum breakdown useful? Bookmark it and check back as we publish more practical, data-backed investing guides.

This article is for informational purposes only and is not investment advice. Do your own research.