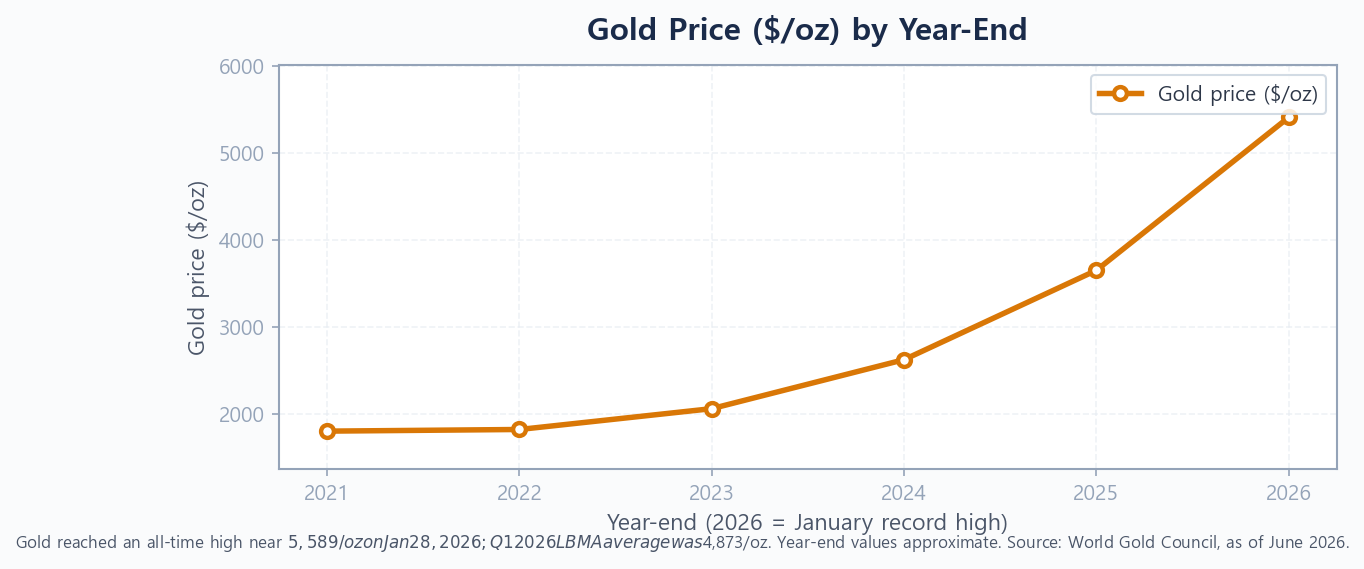

Gold has spent 2026 doing the one thing it is famous for: making headlines. After a historic run, the metal touched an all-time high near $5,589 an ounce in late January before settling back, and central banks are still buying it at a record pace. If you are watching all of this and wondering whether you are missing out — and how much gold should you hold in your portfolio in 2026 — you are asking exactly the right question. The honest answer is not “as much as possible.” For most long-term investors, gold works best as a small, deliberate slice rather than a big bet. This guide explains why, and how to land on a number you can actually stick with.

Why Gold Is Suddenly in Every Headline

Gold’s rise has not come out of nowhere. Three forces have stacked up at once: persistent geopolitical uncertainty, expectations that the Federal Reserve will keep easing, and a weaker US dollar that makes dollar-priced gold cheaper for the rest of the world. On top of that, central banks have become relentless buyers — they added 244 tonnes to global reserves in the first quarter of 2026 alone, and 95% of them told the World Gold Council they expect to keep accumulating, the highest share ever recorded (Source: World Gold Council, Q1 2026 Gold Demand Trends).

The chart makes the story plain: a fairly flat metal through 2021–2022, then a steady climb that accelerated sharply into 2025 and 2026. A lot of that final leg is tied to the falling dollar — gold and the dollar often move in opposite directions, a link we cover in how a weak dollar affects your portfolio. The takeaway for you is not “buy because it went up.” It is the opposite: a record-high price is precisely when sizing matters most.

What Gold Actually Does in a Portfolio

Before choosing a number, it helps to understand the job you are hiring gold to do. Gold is not a growth engine and it is not income — it pays no dividend and no interest. What it offers is a low, sometimes negative, correlation to stocks: it often holds or gains value when equities fall. That makes it a diversifier and a crisis hedge, not a wealth builder.

The case for holding some gold

The strongest argument for gold is behavioral and structural at the same time. Because it tends to zig when stocks zag, a modest gold position can reduce a portfolio’s overall swings. Research cited across the industry suggests that adding around 10% gold to a traditional 60/40 stock-and-bond portfolio has historically trimmed volatility by roughly 15–20% while keeping long-term returns broadly comparable (Source: industry allocation studies, 2026). For an investor who panic-sells in downturns, that smoother ride can be worth more than a slightly higher headline return.

The honest case against gold

Here is the part the gold ads leave out. Over the very long run, gold’s real (after-inflation) expected return is close to zero — it preserves purchasing power rather than compounding it. Every dollar in gold is a dollar not in stocks, which have produced real growth over time, or in bonds, which at least pay a yield. Skeptics like analyst Ben Felix have shown that historically, swapping a 10% gold sleeve for 10% bonds often produced both higher returns and better risk-adjusted returns. None of this means gold is useless — it means gold earns its place as a hedge, not as a core holding. That single distinction is what keeps your allocation sensible.

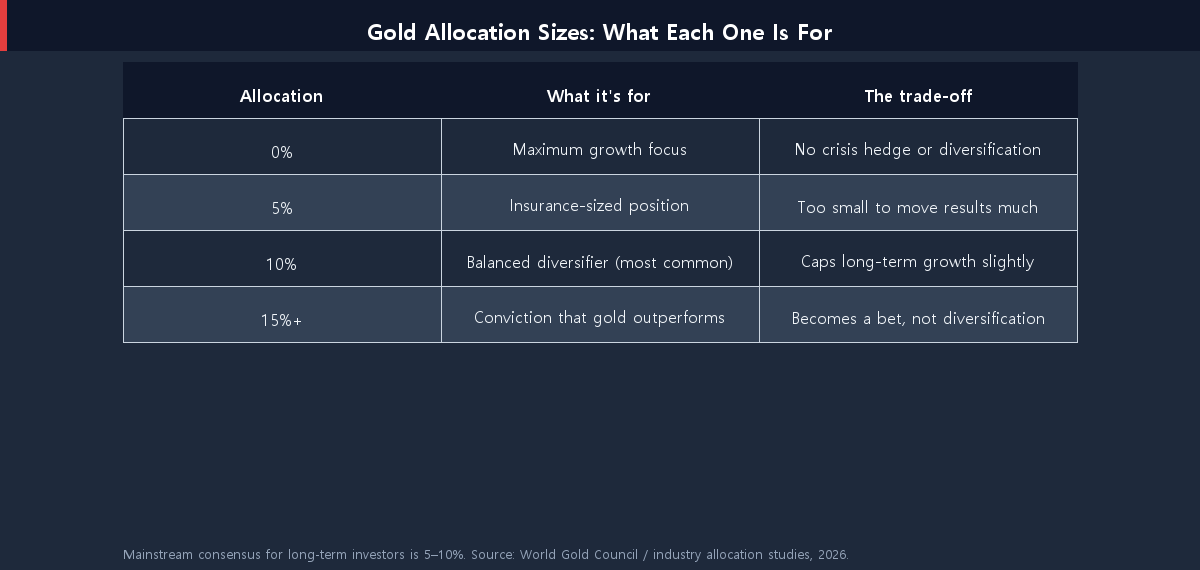

So How Much Gold Should You Hold?

For the vast majority of long-term investors, the evidence and the mainstream consensus point to the same range: roughly 5% to 10% of your portfolio, with 10% as a sensible upper bound for most people. Below is how to think about each size rather than guessing.

Notice that the table is built around purpose, not prediction. A 5% position is “insurance” — small enough to barely matter if gold stalls, but real enough to help in a crisis. A 10% position is the classic balanced diversifier. Anything above 15% stops being diversification and becomes a conviction bet that gold will outperform — a forecast no one can make reliably, least of all at record prices.

The video below walks through the same question from an evidence-based angle and is a useful sanity check before you commit to a number.

One more framing helps: decide where gold’s slice comes from. If you carve it out of your defensive holdings, compare it honestly against high-quality bonds — see our 10-year Treasury yield outlook for 2026, because a 4%-plus yield is a real competitor to a zero-yield metal. If you carve it from stocks, accept that you are trading some long-term growth for stability.

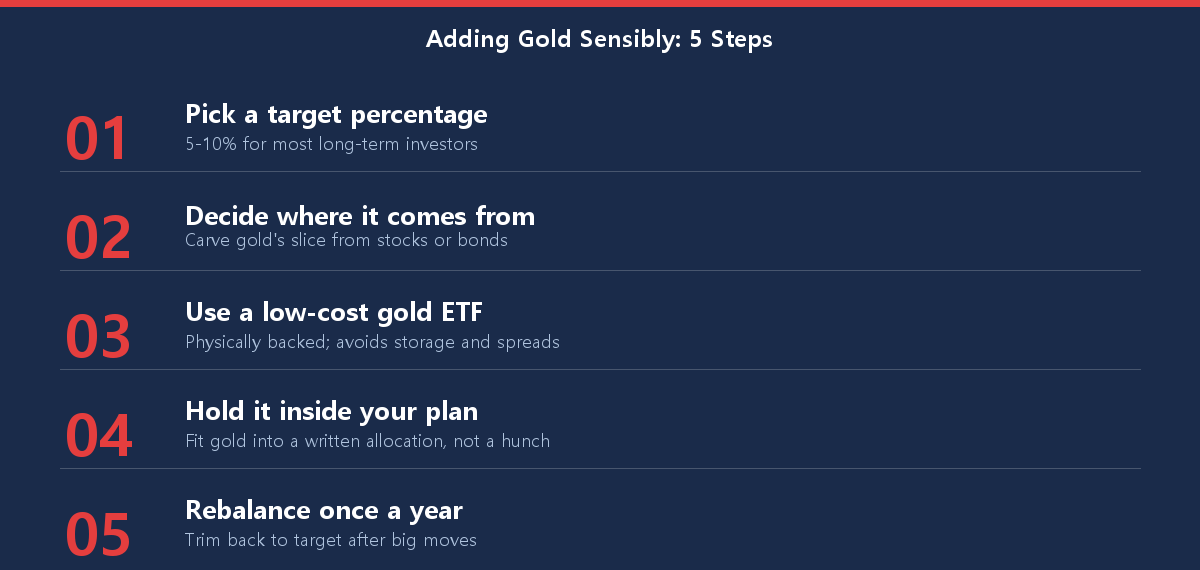

How to Add Gold Without Overcomplicating It

Choosing a percentage is the hard part; implementing it is easy. A few disciplined steps keep the position doing its job instead of becoming a distraction.

Most investors are best served by a low-cost, physically backed gold ETF held inside their existing brokerage account — it avoids storage, insurance, and the wide buy-sell spreads of physical coins. Whatever you choose, fit gold into a written plan rather than chasing it. If your overall split between stocks, bonds, and real assets is unclear, start with our beginner’s guide to asset allocation, which shows how a gold sleeve sits inside a complete portfolio. And remember the other 90%: the bulk of long-term growth still comes from productive assets such as the best high-yield dividend ETFs for 2026.

Conclusion: A Slice, Not a Bet

So, how much gold should you hold in your portfolio in 2026? For most long-term investors, somewhere between 5% and 10% — enough to cushion the bad years, small enough that gold’s lack of yield won’t quietly drag on your wealth. Resist the pull of record-high headlines to go bigger; the right time to size a hedge is calmly, in advance, not in the middle of a rally. Pick a number that matches your temperament, rebalance back to it once a year, and let the rest of your portfolio do the heavy lifting of growing your money.

Found this useful? Bookmark it so you can revisit the next time gold makes headlines.

This article is for informational purposes only and is not investment advice. Do your own research before making any investment decision.