If you have cash sitting on the sidelines in 2026 — an emergency fund, a house deposit, or money you simply don’t want in stocks — you have probably noticed two options shouting for attention: short-term bonds and high-yield savings accounts. Both promise a safe place to earn around 4% with very little risk, which makes the choice genuinely confusing. The honest answer is that short-term bonds vs high-yield savings accounts is rarely about which one “wins” outright; it is about taxes, access to your money, and how much effort you want to spend. This guide breaks down the real differences with current numbers so you can match the right tool to your cash.

What’s the Difference Between Short-Term Bonds and Savings?

A high-yield savings account (HYSA) is a bank deposit, usually from an online bank, that pays far more interest than a traditional savings account. Your balance is insured by the FDIC up to $250,000 per depositor, and you can deposit or withdraw almost any time. The rate is variable — the bank can change it whenever it likes.

“Short-term bonds” in this context usually means Treasury bills (T-bills) — debt issued by the US government that matures in one year or less (4, 8, 13, 26, or 52 weeks). You buy them at a discount and receive the full face value at maturity; the difference is your yield. They are backed by the US government and the rate is locked in the moment you buy. The same logic extends to short-term bond ETFs that hold a basket of these bills and notes.

So the core trade-off is this: a savings account is endlessly flexible with a rate that floats, while a short-term Treasury locks your rate for a set term and adds a quiet tax advantage. If you want the full walkthrough on purchasing them, see our guide on how to buy US Treasury bonds.

2026 Yields: How the Numbers Actually Compare

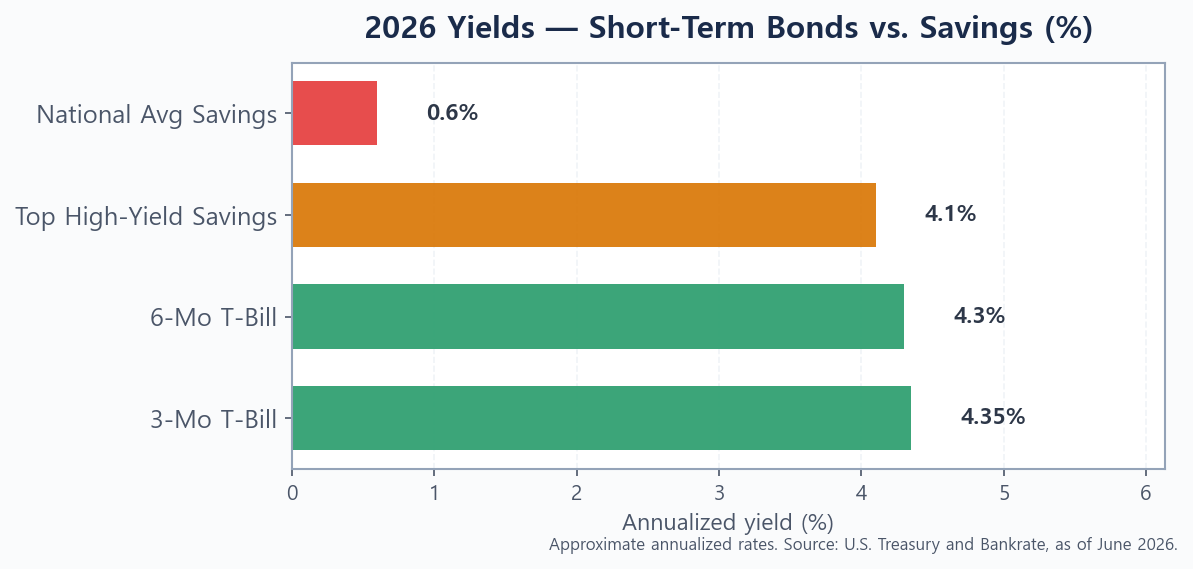

In mid-2026, short-term Treasuries and the best savings accounts are paying remarkably similar headline rates. Short-term T-bills are yielding roughly 4.2% to 4.4% depending on maturity, while the top high-yield savings accounts advertise around 4.1% APY — with a handful of promotional offers reaching higher. The gap between them is often just a few tenths of a percent (Source: U.S. Treasury and Bankrate, as of June 2026).

The chart makes one thing obvious: both short-term bonds and high-yield savings crush the national average savings rate of around 0.6%. The difference between a big-bank savings account and either of these options is measured in hundreds of dollars a year on a $20,000 balance. Between a T-bill and a top HYSA, though, the raw yield gap is small — which is exactly why the tiebreakers below matter so much.

Side-by-Side: Treasury Bills vs. High-Yield Savings

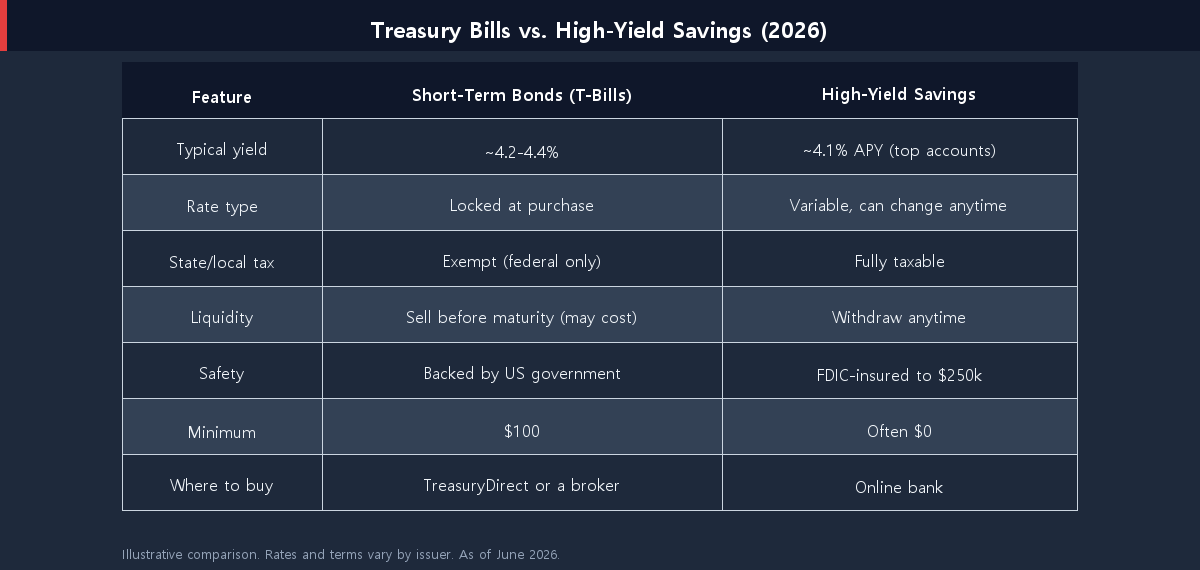

Headline yield is only one column. When you line these two up across the features that actually affect your money, a clearer picture emerges.

The pattern is consistent: the high-yield savings account wins on simplicity and instant access, while the short-term Treasury wins on rate certainty and tax treatment. Neither is “safer” in any meaningful way — FDIC insurance and the full faith of the US government are both about as solid as it gets for cash.

The Tax Twist That Changes the Math

Here is the detail most quick comparisons skip. Interest from a high-yield savings account is fully taxable — federal, state, and local. Interest from Treasury bills is exempt from state and local income tax; you only owe federal tax (Source: TreasuryDirect, 2026).

That exemption can flip a close race. If you live in a high-tax state, a T-bill yielding 4.3% can leave more in your pocket than a savings account yielding even 4.5%, once state tax is taken out. A simple way to compare apples to apples is the tax-equivalent yield:

- The rule of thumb: divide the T-bill yield by (1 − your state tax rate) to see what a savings account would need to pay to match it.

- Example: a 4.3% T-bill for someone in a 6% state bracket is worth about 4.57% in pre-state-tax terms.

- If you live in a no-income-tax state (e.g., Texas or Florida), this advantage disappears and the comparison comes down to yield and convenience.

None of this is a reason to chase the last basis point — but on a large cash balance, the state-tax break is a real, repeatable edge for short-term bonds.

Which One Fits Your Cash? A Simple Decision Guide

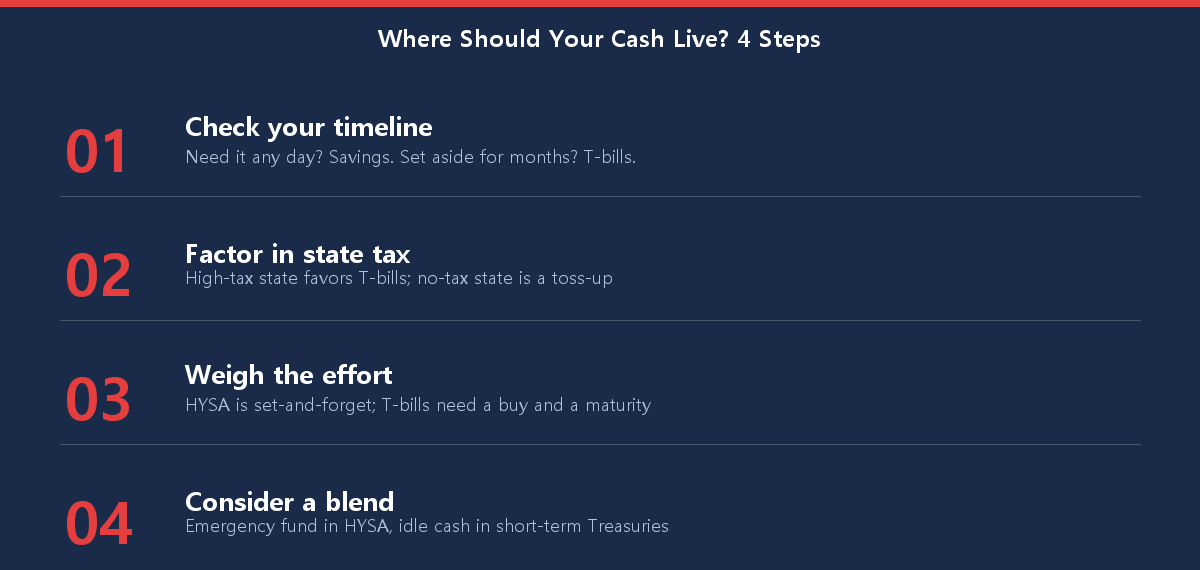

The best choice depends less on the rate and more on when you’ll need the money and how much you’d rather not think about it. Walk through the steps below to match the tool to the job.

For most people the answer is a blend: keep your true emergency fund in an HYSA for instant access, and move cash you won’t touch for several months into T-bills to capture the locked rate and tax break. To see where this slice of “safe money” fits in your overall plan, read our beginner’s guide to asset allocation.

Three Mistakes People Make When Parking Cash

- Leaving cash in a big-bank savings account. Earning 0.6% when 4%+ is available is the single most expensive habit on this list.

- Locking up the emergency fund. Selling a T-bill before maturity is possible but can cost you; money you might need tomorrow belongs in an HYSA.

- Ignoring taxes entirely. Comparing a savings APY to a T-bill yield without adjusting for the state-tax exemption gives the savings account an edge it may not deserve.

Conclusion: It’s Not Either/Or

When you weigh short-term bonds vs high-yield savings accounts in 2026, the headline yields are close enough that the decision really comes down to access, taxes, and effort. A high-yield savings account is the better home for money you might need at a moment’s notice, while a short-term Treasury rewards you with a locked rate and a state-tax break on cash you can set aside for a few months. Used together, they let your idle money work hard without taking on stock-market risk. If you’re just getting your footing, how to start investing with only $100 is a useful next step.

Found this helpful? Bookmark it and revisit when rates move — the right place for your cash can change as the Fed does.

This article is for informational purposes only and is not investment advice. Do your own research.