You’ve heard the advice a hundred times: “Just buy index funds.” But which ones? How much of each? And how do you actually sit down and do it? The 3-fund portfolio — three broadly diversified index funds that together cover the entire global stock and bond market — is the answer most serious long-term investors eventually land on. It’s not a compromise. It’s the destination.

This guide walks you through exactly how to build a simple 3-fund portfolio in 2026: which ETFs or mutual funds to pick at Vanguard, Fidelity, or Schwab; how to split your money by age; and how to get everything set up in under 30 minutes. No jargon, no upsells — just the practical steps. Before diving in, our A Beginner’s Guide to Asset Allocation is a useful starting point if you’ve never thought about how to split money across asset classes.

What Is the 3-Fund Portfolio?

The 3-fund portfolio is a passive investing strategy popularized by the Bogleheads community — followers of Vanguard founder Jack Bogle, the father of index investing. The core idea is radical in its simplicity: instead of picking individual stocks, sector bets, or complex strategies, you own three things.

- The entire U.S. stock market

- The entire international stock market

- The entire U.S. bond market

That’s it. Together, these three funds hold over 10,000 securities across 50+ countries — a level of diversification that no actively managed fund can realistically replicate. The 3-fund portfolio works because:

- Cost is minimal: Expense ratios range from 0.00% to 0.07%.

- Tax efficiency is high: Broad index funds rarely trigger capital gains distributions.

- Behavioral risk is low: Simple portfolios are dramatically easier to stick with during market crashes.

- Long-run performance is competitive: Over 20-year periods, the 3-fund approach has historically matched or beaten more than 80% of actively managed funds (Source: S&P SPIVA Report, 2025).

In 2026, with U.S. stock valuations still historically stretched and international markets trading at half the U.S. price-to-earnings multiple, the case for owning all three funds — not just a U.S.-only portfolio — is stronger than it has been in years.

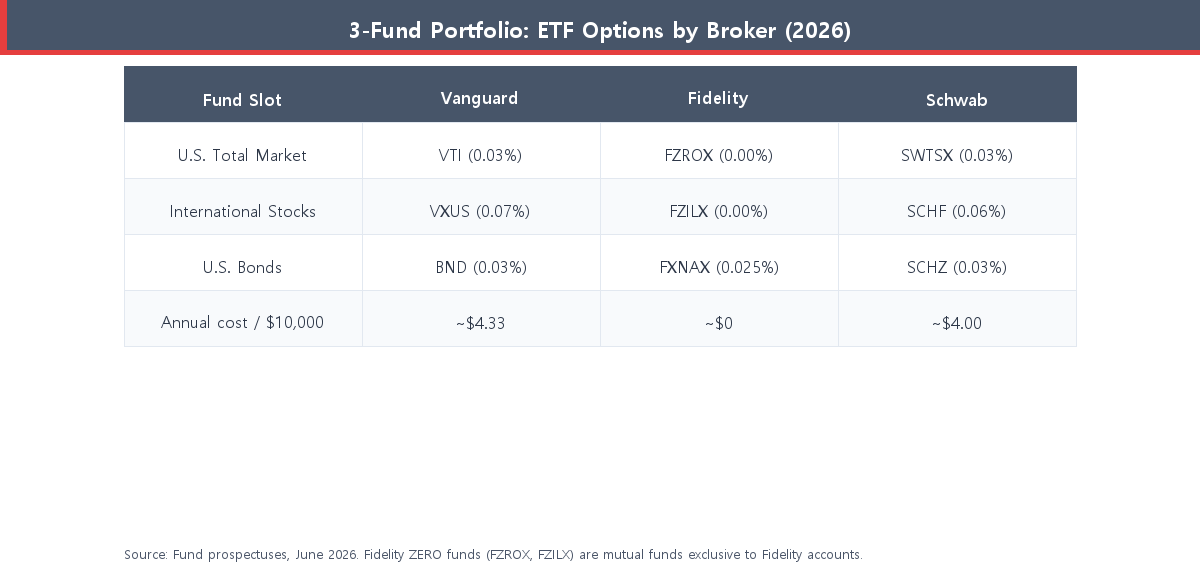

The Best ETFs for Each Fund Slot in 2026

There is no single “right” fund. The best choice depends on which brokerage you already use. The table below maps the top low-cost option at each of the three major brokers — Vanguard, Fidelity, and Schwab — across all three fund slots.

Fund 1 — U.S. Total Market

Goal: Own every publicly traded U.S. company — large-cap, mid-cap, and small-cap — in a single fund.

- Vanguard: VTI (Vanguard Total Stock Market ETF) — Expense ratio: 0.03%. Holds ~3,700 U.S. stocks, the gold standard since 2001.

- Fidelity: FZROX (Fidelity ZERO Total Market Index Fund) — Expense ratio: 0.00%. Genuinely free — no expense ratio at all. It’s a mutual fund (not an ETF), so it can only be held at Fidelity, but for Fidelity customers it’s the obvious pick.

- Schwab: SWTSX (Schwab Total Stock Market Index Fund) — Expense ratio: 0.03%. A solid, low-cost mutual fund option for Schwab accounts.

Fund 2 — International Stocks

Goal: Own developed and emerging market stocks outside the U.S. — Europe, Japan, South Korea, emerging Asia, Latin America, and more.

- Vanguard: VXUS (Total International Stock ETF) — Expense ratio: 0.07%. Covers roughly 7,800 international stocks across 47 countries.

- Fidelity: FZILX (Fidelity ZERO International Index Fund) — Expense ratio: 0.00%. Free international exposure for Fidelity customers.

- Schwab: SCHF (Schwab International Equity ETF) — Expense ratio: 0.06%. Covers developed markets (excludes emerging markets); investors wanting broader coverage can pair with SCHE.

Why own international stocks at all? In 2026, international developed markets trade at a cyclically adjusted P/E (CAPE) ratio of approximately 16–18, compared to the U.S. S&P 500 at roughly 26 (Source: Barclays Research, mid-2026). That’s the cheapest relative valuation for international stocks versus U.S. stocks in over a decade. History shows cheaper markets tend to deliver better forward returns. You don’t need to overweight international — but owning both is meaningful diversification.

Fund 3 — U.S. Bonds

Goal: Add portfolio stability and income via the entire U.S. investment-grade bond market — Treasuries, corporate bonds, and mortgage-backed securities.

- Vanguard: BND (Total Bond Market ETF) — Expense ratio: 0.03%. Yield as of mid-2026: approximately 4.3–4.6% annually (Source: Vanguard, June 2026).

- Fidelity: FXNAX (US Bond Index Fund) — Expense ratio: 0.025%. Tracks the same Bloomberg U.S. Aggregate Bond Index as BND.

- Schwab: SCHZ (US Aggregate Bond ETF) — Expense ratio: 0.03%. Nearly identical to BND in structure and holdings.

An important 2026 note: bonds are no longer dead weight. BND’s ~4.4% yield is the highest sustained level since 2007. The bond slot in your 3-fund portfolio now generates real income — providing both a cushion during equity downturns and meaningful return in its own right. To understand how even small differences in expense ratios compound over time, see our explainer: What Is an ETF Expense Ratio?

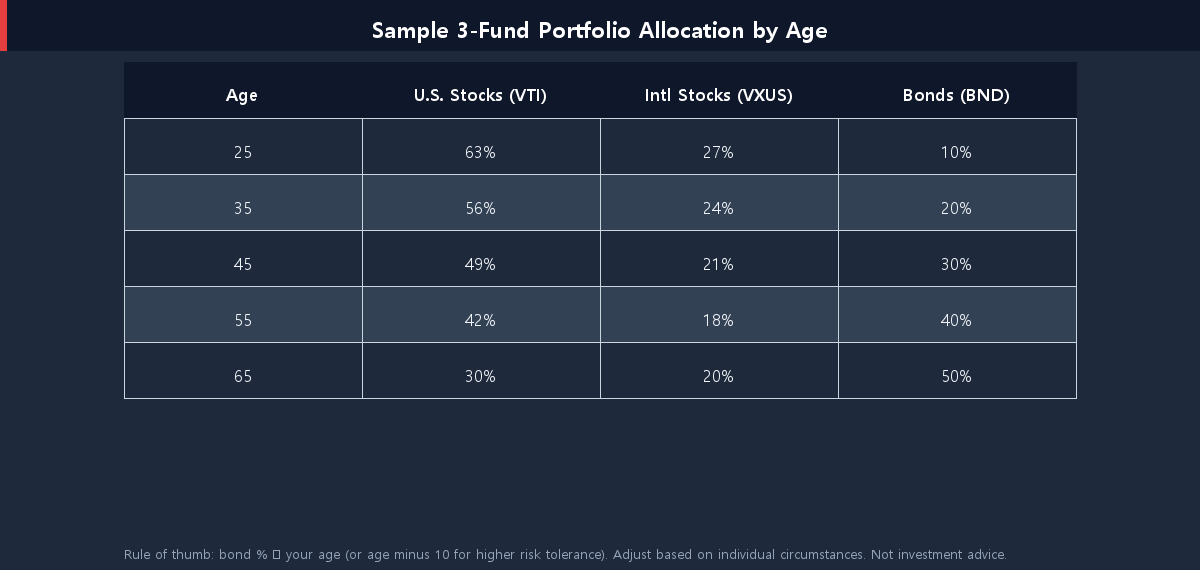

How to Split Your Money: Allocation by Age

The classic rule of thumb is “your age in bonds.” A 30-year-old holds 30% bonds; a 60-year-old holds 60% bonds. Modern guidance often softens this — many financial planners now suggest “age minus 10” in bonds for investors with longer time horizons or higher risk tolerance — but the core logic is sound: bonds should increase as you near retirement.

Within the stock portion, a common starting split is 70% U.S. / 30% international, which roughly reflects global market capitalization. Some investors prefer 80/20 (higher U.S. comfort); the Bogleheads community often recommends market-weight (~60% U.S. / 40% international). Neither is wrong — pick a split you’ll actually hold through a rough year for one region.

A quick allocation guide by life stage:

- Under 35: 85–90% stocks (split ~70/30 U.S./intl), 10–15% bonds

- 35–50: 70–80% stocks, 20–30% bonds

- 50–60: 60–70% stocks, 30–40% bonds

- 60+ (near retirement): 50–60% stocks, 40–50% bonds

The most important thing is not to agonize over the exact split. An allocation you’ll stick with during a 30% market drop is worth far more than a theoretically optimal one you’ll abandon.

Step-by-Step: How to Build Your 3-Fund Portfolio

Here’s how to go from zero to invested in under 30 minutes:

- Open a brokerage account. Choose Vanguard, Fidelity, or Schwab. All three are reputable, have no trading commissions on their own funds, and offer the index funds you need. Fidelity’s ZERO funds have no expense ratio but are exclusive to Fidelity — a meaningful edge for long-term holders.

- Fund your account. Link your bank and transfer your initial amount. There are no account minimums for ETFs at any of the three brokers; Fidelity’s zero-cost mutual funds also have no minimums.

- Choose your stock/bond split. Use your age as a starting guide, then adjust based on your risk tolerance. Write it down.

- Choose your U.S./international split. Start with 70% U.S. / 30% international within your stock allocation. Adjust over time if you have strong views.

- Place your purchases. For a $10,000 account with an 80% stock / 20% bond split and a 70/30 U.S./international split within stocks:

- U.S. stocks (VTI / FZROX): $5,600

- International stocks (VXUS / FZILX): $2,400

- U.S. bonds (BND / FXNAX): $2,000

- Automate contributions. Set up a recurring transfer from your bank. Directing new money toward whichever fund has drifted below target is the simplest form of rebalancing.

Not sure whether to invest your money all at once or gradually? Our data-backed comparison — Dollar-Cost Averaging vs. Lump-Sum: Which Wins in 2026? — shows that lump-sum beats dollar-cost averaging roughly two out of three times historically, though DCA reduces regret for risk-averse investors.

The video below from personal finance author Rob Berger addresses the most common misconceptions people have about the 3-fund portfolio — well worth watching before you place your first order.

How and When to Rebalance

Rebalancing means selling a portion of whatever has grown above its target weight and using the proceeds to buy what has lagged — restoring your original allocation. This is the only maintenance the 3-fund portfolio really needs.

Two practical rebalancing triggers:

- Calendar-based: Once per year on a fixed date (January 1st, your birthday, tax filing day). Simple and low-cost.

- Threshold-based: Rebalance any time an individual fund drifts more than 5 percentage points from its target. This catches large market moves without requiring constant monitoring.

Practical tips to minimize tax drag:

- Rebalance inside tax-advantaged accounts first: Selling inside a 401(k) or IRA generates no taxable event. Exhaust this option before touching a taxable brokerage account.

- Use new contributions to rebalance: Direct new money to whichever fund is below its target weight. Often this is enough to stay on track without selling anything.

- Don’t over-rebalance: Rebalancing quarterly or monthly creates unnecessary trading costs and potential tax events. Once a year — or when a 5-point drift occurs — is enough.

In a year when U.S. equities have significantly outpaced international, rebalancing mechanically forces you to trim U.S. exposure (selling high) and add to international (buying low) — a disciplined version of the contrarian investing ideal, without requiring any market-timing judgment.

Why the 3-Fund Portfolio Still Makes Sense in 2026

A common objection: “Is three funds really enough in 2026? Shouldn’t I add sector ETFs, REITs, commodities, gold, or crypto for diversification?” You can — but research consistently shows complexity rarely beats simplicity.

The 3-fund portfolio captures 100% of global market returns. No sector or strategy persistently beats the total market over long periods after fees and taxes. Adding narrower funds typically increases concentration risk, not diversification. The Vanguard VBTLX and its equivalents also now yield more than most dividend-focused equity strategies — making the “bonds are boring” argument weaker than it’s been in 15 years.

The 3-fund approach also scales seamlessly — the strategy that works for a 25-year-old contributing $200 a month also works for a 55-year-old managing an $800,000 IRA. If you’re building from a very small starting amount, How to Start Investing With Only $100 shows how fractional shares make the 3-fund portfolio accessible from your very first deposit.

The Bottom Line

Three funds. Two asset classes. One annual rebalance. That’s the complete 3-fund portfolio. It’s not the most exciting investing strategy — and that’s exactly the point. Boring portfolios stay invested. Invested portfolios compound. Compounding builds wealth.

Pick your broker, decide your allocation, make your first purchase, and automate your contributions. The rest is patience.

This article is for informational purposes only and is not investment advice. Investment decisions and their outcomes are the sole responsibility of the reader. Past performance does not guarantee future results.