With short-term Treasury yields still sitting above 5% and 10-year notes near 4.5% as of mid-2026, retirees and pre-retirees have a rare opportunity: US government bonds are actually paying meaningful income again. The question is how to capture that income most effectively. Two strategies dominate the conversation — building a Treasury bond ladder or buying a bond ETF. Each has a legitimate place in a retirement portfolio, but they work very differently. This guide lays out the mechanics of each, runs a real $100,000 ladder example using 2026 yields, and gives you a clear framework for deciding which fits your situation. If you are new to Treasuries, start with our guide on How to Buy US Treasury Bonds before diving in here.

What Is a Treasury Bond Ladder — and How Does It Work?

A bond ladder is a portfolio of individual bonds with staggered maturity dates, each one representing a “rung.” When the shortest-dated rung matures, you receive the full face value back. You then reinvest that principal into a new long-dated bond at the far end of the ladder, extending the rungs forward by one year. The result is a self-renewing stream of income that also returns your original capital on a predictable schedule.

The core appeal for retirees is control. You know exactly when each bond matures, exactly what coupon you locked in, and exactly how much principal you will recover — none of which is true with a bond fund. There is no “net asset value” that can fall 10% in a rising-rate year. Each rung simply pays its coupon and returns par at maturity.

How to Build a 5-Rung Treasury Ladder (Step by Step)

- Decide on ladder length and rung count. A 5- to 7-year ladder covering core living expenses is a common starting point. More rungs smooth reinvestment risk.

- Divide your capital equally. For a 5-rung ladder, split your investment into five equal portions — one per maturity year.

- Buy Treasuries at each maturity. Use TreasuryDirect.gov, a brokerage, or a Treasury ETF with a fixed maturity date (iBond iBonds ladder funds). Choose T-Bills (under 1 year), T-Notes (2–10 years), or T-Bonds (20–30 years) depending on your rungs.

- Collect semiannual coupons. T-Notes and T-Bonds pay interest every six months. Add these to your monthly income budget or reinvest them.

- Reinvest maturing rungs. When a rung matures, buy a new bond at the long end of your target horizon, keeping the ladder alive.

Example: A $100,000 Treasury Ladder at 2026 Yields

The table below shows what a five-rung $100,000 Treasury ladder looks like using approximate yields from the U.S. Treasury curve as of June 2026.

| Rung | Maturity | Allocation | Yield (2026) | Annual Income |

|---|---|---|---|---|

| 1 | 1-Year T-Note | $20,000 | 4.8% | $960 |

| 2 | 2-Year T-Note | $20,000 | 4.6% | $920 |

| 3 | 3-Year T-Note | $20,000 | 4.4% | $880 |

| 4 | 5-Year T-Note | $20,000 | 4.3% | $860 |

| 5 | 7-Year T-Note | $20,000 | 4.4% | $880 |

| Total | — | $100,000 | 4.5% blended | ~$4,500/year |

That $4,500 in annual coupon income represents a 4.5% blended yield on your $100,000 — and in 2026 that is entirely from US government-backed bonds with no credit risk (Source: U.S. Treasury, June 2026). State-income-tax exemption on Treasury interest adds a further edge for residents of high-tax states.

What Is a Bond ETF — and Why Do Retirees Use Them?

A bond ETF is a fund that holds a diversified basket of bonds — Treasuries, agency bonds, corporate bonds, or some mix — and trades on a stock exchange like a single share. The fund manager continuously buys and sells bonds to maintain a target duration or index, so unlike a bond ladder, a bond ETF has no fixed maturity date. You can buy or sell your position any trading day at the market price.

The appeal is simplicity. One ticker gives you exposure to hundreds or thousands of individual bonds at an expense ratio as low as 0.03%. Dividends accumulate from the underlying coupons and are paid out monthly. For investors who prefer a hands-off approach, bond ETFs are hard to beat on convenience and diversification.

How Bond ETF Income Works (vs. Coupon Payments)

A bond ETF distributes income monthly, drawn from the weighted average coupons of the bonds it holds. That sounds similar to ladder coupons, but there is a key structural difference: the ETF’s net asset value (NAV) can fall significantly when interest rates rise, because the underlying bond prices decline. In a rising-rate environment, you might collect a 4.5% distribution yield while simultaneously seeing your principal erode 6–8% — a net loss for the year. A ladder holder in the same rate environment simply holds to maturity and receives full par back, insulated from price volatility.

Top Bond ETFs for Retirement Income in 2026

| ETF | Focus | 30-Day SEC Yield | Expense Ratio |

|---|---|---|---|

| BND | Total US Bond Market | 4.5% | 0.03% |

| AGG | US Aggregate Bond | 4.4% | 0.03% |

| VGIT | Intermediate-Term Treasury | 4.5% | 0.04% |

| GOVT | Broad US Treasury | 4.5% | 0.05% |

| TLT | 20+ Year Treasury | 4.9% | 0.15% |

(Source: Fund providers, as of June 2026. Yields fluctuate; check current rates before investing.) Note that TLT’s higher yield comes with significantly higher duration risk — a 1% rise in rates moves TLT’s NAV by roughly 17%. Read our Why Short-Duration Bonds Win analysis for context on managing duration in the current environment.

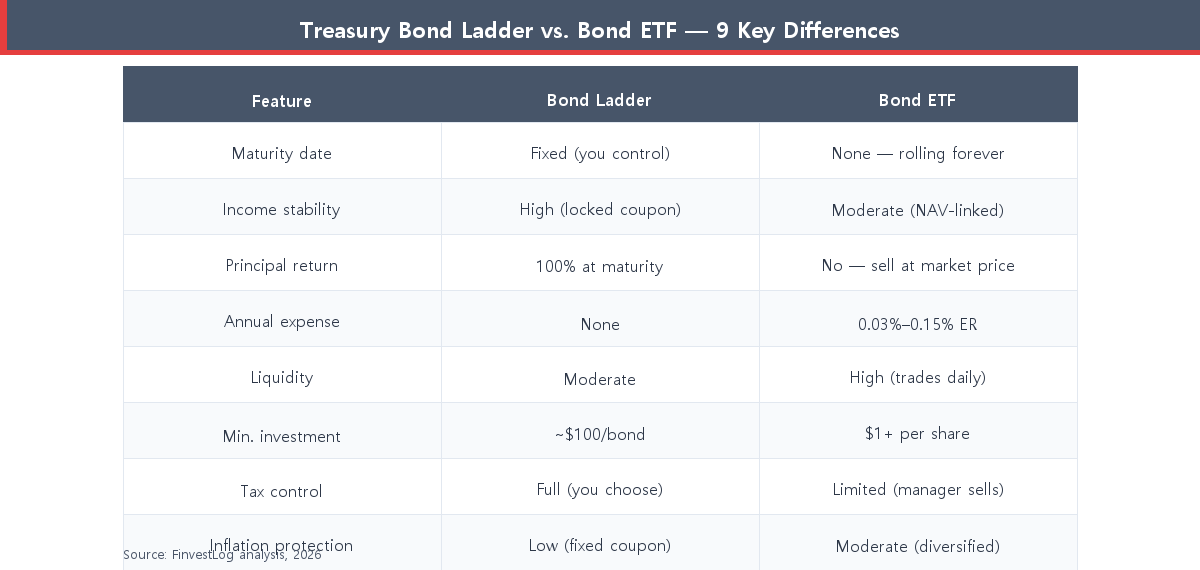

Bond Ladder vs. Bond ETF — Head-to-Head Comparison

The nine-point table below captures the most decision-relevant differences between building a Treasury bond ladder and holding a bond ETF as your retirement income vehicle. The right choice depends on which attributes matter most for your cash-flow needs.

One dimension the table cannot fully convey is credit risk. Both Treasury ladders and Treasury-focused ETFs (BND, VGIT, GOVT) carry essentially zero default risk. But if you venture into corporate bond ETFs for extra yield, you take on credit spread risk that a pure-Treasury ladder sidesteps. Our deep dive on Corporate Bonds vs. Treasuries quantifies how much additional yield is actually worth the extra risk in 2026.

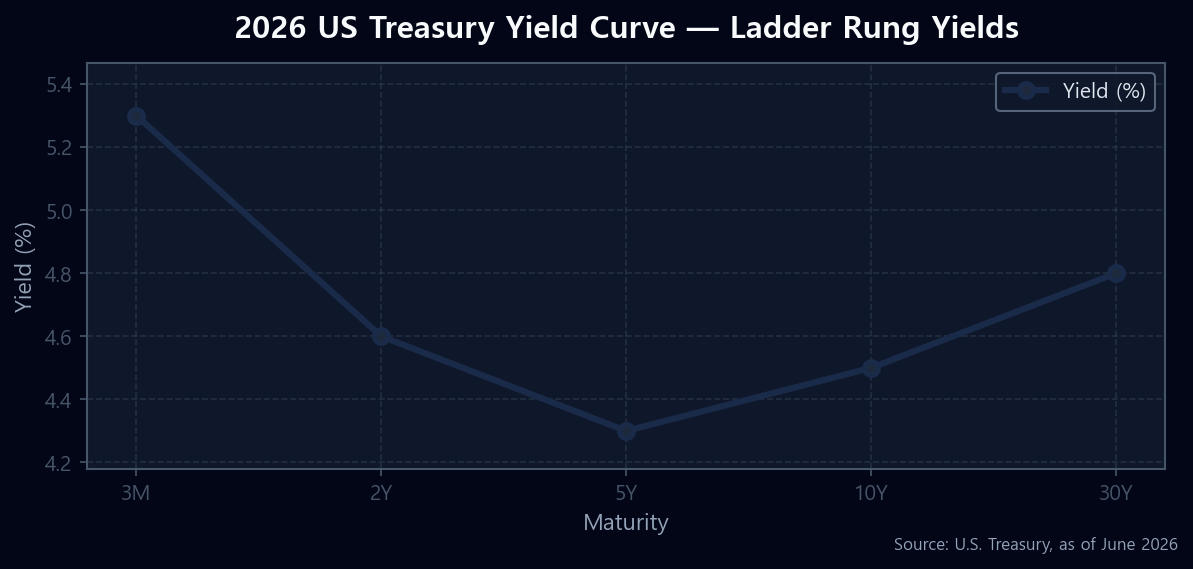

2026 Treasury Yield Curve: What You Actually Lock In With a Ladder

Understanding the current yield curve shape is essential before committing to a ladder structure. As of June 2026, the US Treasury curve is mildly inverted at the short end and then slopes upward into longer maturities, with the following approximate yields (Source: U.S. Treasury, June 2026): 3-Month T-Bill at 5.3%, 2-Year at 4.6%, 5-Year at 4.3%, 10-Year at 4.5%, and 30-Year at 4.8%. The chart below plots these ladder rung yields so you can visualize exactly what you are locking in at each maturity point.

The near-flat shape between the 2-year and 10-year maturities (4.6% vs. 4.5%) means there is little “term premium” for extending duration right now — a consideration that favors shorter-to-intermediate ladders over locking into 20–30 year maturities at only marginally higher yields. See our 10-Year Treasury Yield Outlook 2026 for a full breakdown of where forecasters expect the curve to move by year-end. The Barron’s Streetwise video below covers the ladder-vs-fund decision and the TIPS angle in an accessible format:

Which Is Better for Retirement Income in 2026?

There is no universal winner. The right tool depends on four personal factors: your need for income certainty, your tolerance for NAV volatility, the size of your investable capital, and how much time you want to spend managing the portfolio.

Choose a Bond Ladder If…

- You need guaranteed income on a fixed schedule. Knowing Rung 3 matures in 2029 and returns $20,000 in principal makes cash-flow planning straightforward.

- You are sensitive to principal loss. A ladder held to maturity returns 100 cents on the dollar regardless of what rates do after you buy.

- You have enough capital to diversify rungs. A meaningful ladder typically needs $50,000–$100,000+ to cover multiple rungs without concentrating too much in any single maturity.

- You want precise tax control. You decide when to recognize gain or loss by choosing which rung to sell if you ever need to liquidate early.

- You are in a high-income-tax state. Treasury interest is exempt from state income tax, which a broad bond ETF (holding some corporate/agency bonds) may not fully replicate.

Choose a Bond ETF If…

- You want simplicity. One ticker, automatic monthly income, no reinvestment decisions to make each time a rung matures.

- You are starting small. You can buy a share of BND for the price of a single share, while a TreasuryDirect purchase minimum is $100 per bond.

- You need maximum liquidity. An ETF can be sold in seconds during market hours; individual Treasury bonds have bid-ask spreads that widen in volatile markets.

- You want built-in diversification. BND holds more than 10,000 bonds across maturities — your exposure is never concentrated in one maturity date.

- You are comfortable with NAV fluctuation. If you will not need to sell the fund in the next 3–5 years, short-term price declines matter less than the income stream.

The Hybrid Approach: Ladder + ETF Core

Many retirement portfolios benefit from combining both strategies. A common approach: build a 3–5 year Treasury ladder to cover essential expenses with predictable, principal-protected cash flows, then hold a low-cost bond ETF (BND or VGIT) for the remainder of your fixed-income allocation. The ladder provides certainty; the ETF provides liquidity, diversification, and ease of management for the longer-horizon portion of your bond allocation.

Conclusion

A Treasury bond ladder gives you income certainty, principal protection, and full tax control — at the cost of more upfront effort and higher capital requirements. A bond ETF gives you simplicity, diversification, and daily liquidity — at the cost of NAV volatility and no guaranteed return of par. In 2026’s elevated-but-flattening yield environment, a 5-rung Treasury ladder blended at roughly 4.5% is a compelling income option for retirees who want to match cash flows to known expenses. For those who prefer a hands-off approach, low-cost ETFs like BND or VGIT deliver similar headline yields at virtually zero management burden.

Neither approach requires sacrificing much yield for the other’s convenience — which is what makes the treasury bond ladder vs bond ETF decision a genuine preference match rather than a clear winner. Build the decision around your cash-flow certainty needs, not just the yield number.

Worth reading next: if inflation protection is a concern alongside your income strategy, our comparison of TIPS vs. I Bonds walks through which inflation-linked bond works best in 2026. Found this useful? Bookmark it so you can revisit when the market moves.

This article is for informational purposes only and is not investment advice. Do your own research before making any investment decisions.