Inflation has cooled from its 2022 peak, but it hasn’t gone away — and after watching prices climb for years, plenty of savers want a piece of their portfolio that can’t be quietly eaten by a rising cost of living. The US Treasury sells two products built for exactly that job: Treasury Inflation-Protected Securities (TIPS) and Series I savings bonds (I Bonds). They share the same inflation index, yet they behave very differently once you own them. Deciding between TIPS vs I Bonds for 2026 comes down to three things most articles gloss over: the guaranteed yield on top of inflation, how each is taxed, and how much you’re allowed to buy. This guide lines them up with current numbers so you can pick the right inflation shield for your cash.

What Are TIPS and I Bonds, Exactly?

Both are backed by the full faith and credit of the US government, and both are designed so that inflation can’t erode what you’ve saved. The difference is how they apply the inflation adjustment.

I Bonds adjust their interest rate. Every six months the Treasury resets a composite rate built from two parts: a fixed rate that never changes for the life of your bond, plus a variable rate tied to the latest inflation reading. For bonds bought between May and October 2026, the fixed rate is 0.90% and the composite rate is 4.26% for the first six months (Source: TreasuryDirect, May 2026). You buy them directly from the government and they accrue value quietly — no price swings, no secondary market.

TIPS adjust their principal. The face value of a TIPS rises with the Consumer Price Index every day, and your fixed coupon is paid on that growing principal. Because TIPS trade on the open market, their price moves with interest rates, and you can buy or sell any amount through a broker. When a TIPS matures you receive the inflation-adjusted principal or the original principal, whichever is higher.

In short: an I Bond is a set-and-forget savings instrument with a rate that floats, while a TIPS is a tradable bond whose value tracks inflation in real time. If the broader bond market is new to you, our walkthrough on how to buy US Treasury bonds covers the mechanics of the Treasury market more generally.

2026 Rates: The Real Yield That Actually Compares

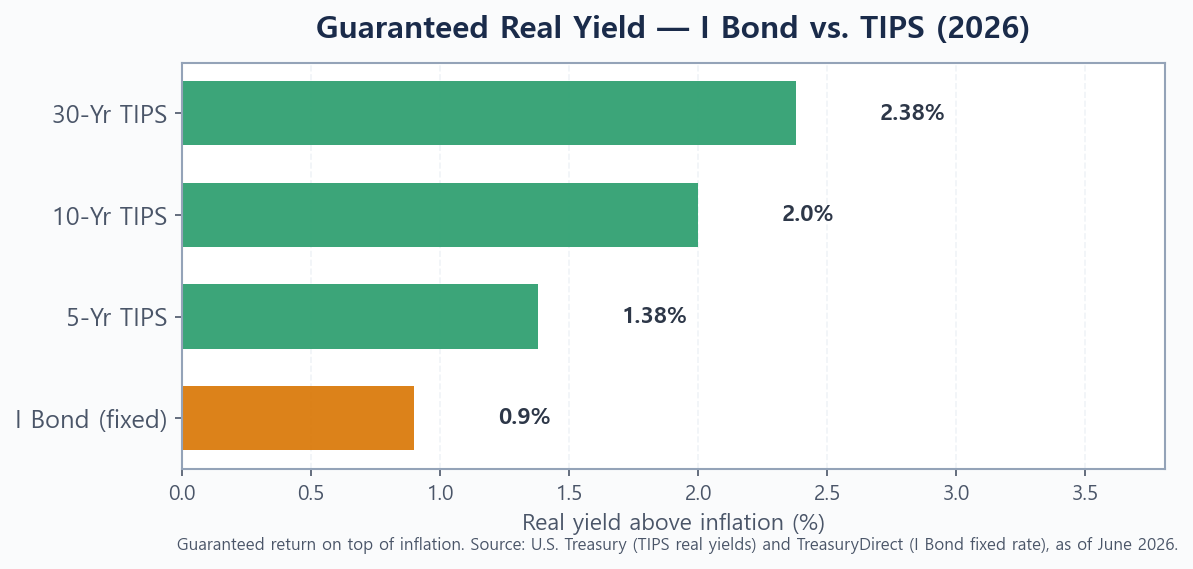

Here’s the trap in most head-to-head comparisons: people pit the I Bond’s headline 4.26% composite rate against a TIPS yield and declare a winner. That’s apples to oranges. The 4.26% already includes inflation; a TIPS real yield does not. To compare fairly, you have to look at the guaranteed return above inflation — the fixed rate on an I Bond versus the real yield on a TIPS.

On that basis, TIPS currently pay more. The I Bond’s fixed rate is locked at 0.90%, while a 5-year TIPS offers a real yield of about 1.38% — roughly 48 basis points higher — and longer TIPS pay more still, ranging up to about 2.38% on the 30-year (Source: U.S. Treasury, as of June 2026). For pure guaranteed yield over inflation, the TIPS is the stronger number in 2026. Both, however, comfortably beat parking cash; for that comparison, see short-term bonds vs. high-yield savings. To understand why real yields sit where they do, it helps to read our 10-Year Treasury yield outlook for 2026.

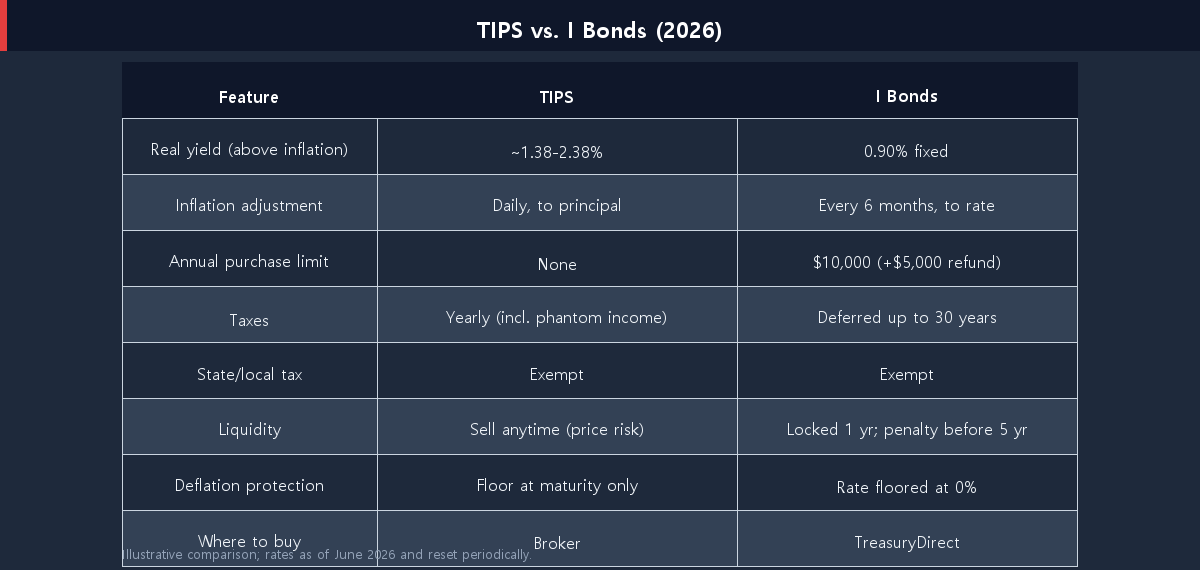

Side-by-Side: TIPS vs. I Bonds at a Glance

Yield is only one column. When you compare the features that actually affect your money — limits, taxes, liquidity, and deflation protection — each instrument wins in different places.

The pattern is clear: I Bonds win on tax deferral and downside protection, while TIPS win on yield, flexibility, and how much you can buy. Neither is “safer” in a meaningful sense — both carry the government’s guarantee. The video below breaks the same trade-off down visually if you prefer to hear it explained.

The Three Differences That Decide It

Most people don’t choose based on a 0.5% yield gap. They choose based on these three practical differences.

Taxes: Defer for 30 Years vs. Pay Every Year

This is the biggest swing factor. I Bond interest is federal-tax-deferred — you owe nothing until you redeem, up to 30 years later, and it’s always exempt from state and local tax. TIPS are taxed every year on both the coupon and the inflation adjustment to principal, even though that adjustment is “phantom” income you haven’t received in cash yet. That’s why TIPS are usually best held inside a tax-advantaged account. If you’re weighing where to keep them, our guide on Roth IRA vs. a taxable brokerage account is a useful companion.

Purchase Limits: $10,000 vs. Unlimited

I Bonds are capped at $10,000 per person per year through TreasuryDirect, plus up to $5,000 more if you direct a tax refund into paper I Bonds (Source: TreasuryDirect, 2026). For anyone trying to build a serious inflation hedge, that ceiling is a real constraint. TIPS have no purchase limit — you can buy as much as your budget allows through any broker, which makes them the only realistic option for larger sums.

Liquidity and Deflation Protection

I Bonds can’t be redeemed at all in the first 12 months, and cashing out before five years costs you the last three months of interest. But they can never lose value — even in deflation, the rate is floored at 0%. TIPS can be sold any day on the secondary market, but their price can fall if real rates rise, and their principal can be adjusted down during deflation (though you’re protected at maturity). So I Bonds offer a hard floor with a lock-up period, while TIPS offer daily liquidity with day-to-day price risk.

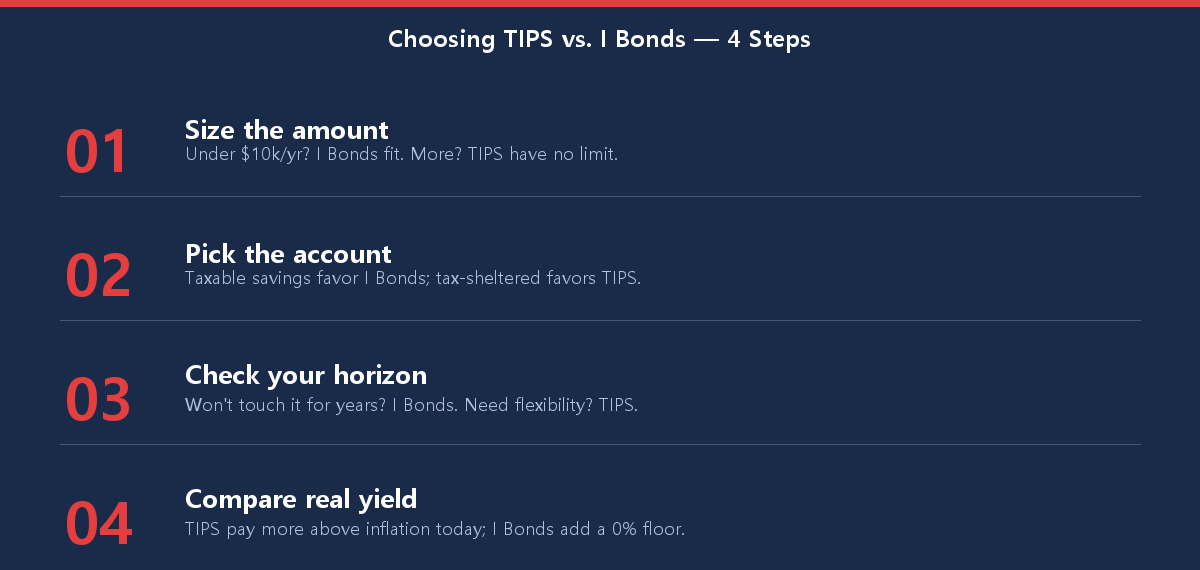

Which Inflation-Protected Investment Fits You?

The “better” choice depends on how much you’re investing, the account you’ll hold it in, and when you’ll need the money. Walk through the steps below to match the tool to the job.

For many savers the answer is a blend: use your annual I Bond allowance for tax-deferred, deflation-proof savings you won’t touch for years, then add TIPS in a retirement account for any inflation protection beyond that $10,000 cap. To see how this slice of “inflation-protected money” fits your overall mix, read our beginner’s guide to asset allocation.

Conclusion: It’s Often Both, Not Either

When you weigh TIPS vs I Bonds as the best inflation-protected investment for 2026, there’s no single winner — there’s a winner for each job. I Bonds reward patience with tax deferral and a guaranteed floor, making them ideal for a modest, long-horizon inflation buffer. TIPS pay a higher real yield, carry no purchase limit, and trade freely, making them the workhorse for larger sums and tax-sheltered accounts. The fixed rate and real yields reset regularly, so the gap between them will shift — bookmark this page and check back when the Treasury announces its next reset.

This article is for informational purposes only and is not investment advice. Rates cited are as of June 2026 and change over time; verify current figures at TreasuryDirect before investing, and do your own research.