Most new investors spend hours hunting for the “best” stock or fund. Yet decades of research point to a less glamorous decision as the real driver of long-term results: asset allocation, or how you split your money across stocks, bonds, and cash. This beginner’s guide to asset allocation breaks down what that split means, why it matters more than picking winners, and how to choose a mix you can actually stick with.

What Asset Allocation Actually Means

Asset allocation is simply the percentage of your portfolio you put into each major type of investment. Instead of asking “which fund should I buy?”, you first ask “how much of my money should sit in growth assets versus safer assets?” That high-level split shapes both your potential return and how much your portfolio will swing in value.

The Three Core Building Blocks

- Stocks (equities): A share of ownership in companies. Historically the highest long-term growth, but also the largest short-term drops.

- Bonds (fixed income): Loans to governments or companies that pay regular interest. More stable than stocks and a cushion when markets fall. If you want to understand this slice in detail, see our walkthrough on starting small with bonds.

- Cash and cash equivalents: Money market funds, short T-bills, and savings. Highly stable and liquid, but the lowest long-run return.

Why Allocation Matters More Than Stock Picking

Your asset allocation decides how much risk your portfolio carries. A 90% stock portfolio and a 40% stock portfolio behave completely differently in a bad year — the first might fall 30% while the second falls closer to 12%. No amount of clever fund selection changes that basic fact.

For a beginner, this is good news. You don’t need to predict the next hot company. You need a sensible split that matches your goals and nerves, then the discipline to leave it alone. Getting the allocation roughly right matters far more than getting the individual picks perfect.

How Much Risk Can You Take? Start With Your Time Horizon

Risk tolerance is part math, part psychology. The math is your time horizon: the longer until you need the money, the more short-term volatility you can ride out, so the more stocks you can hold. The psychology is honesty about how you would react to a 30% drop — a portfolio you panic-sell at the bottom is worse than a calmer one you keep.

A classic rule of thumb is to subtract your age from 110 to estimate your stock percentage. A 30-year-old lands near 80% stocks; a 60-year-old near 50%. Treat it as a starting point, not a law. The video below explains why simple “lifecycle” rules are worth questioning as you refine your own plan.

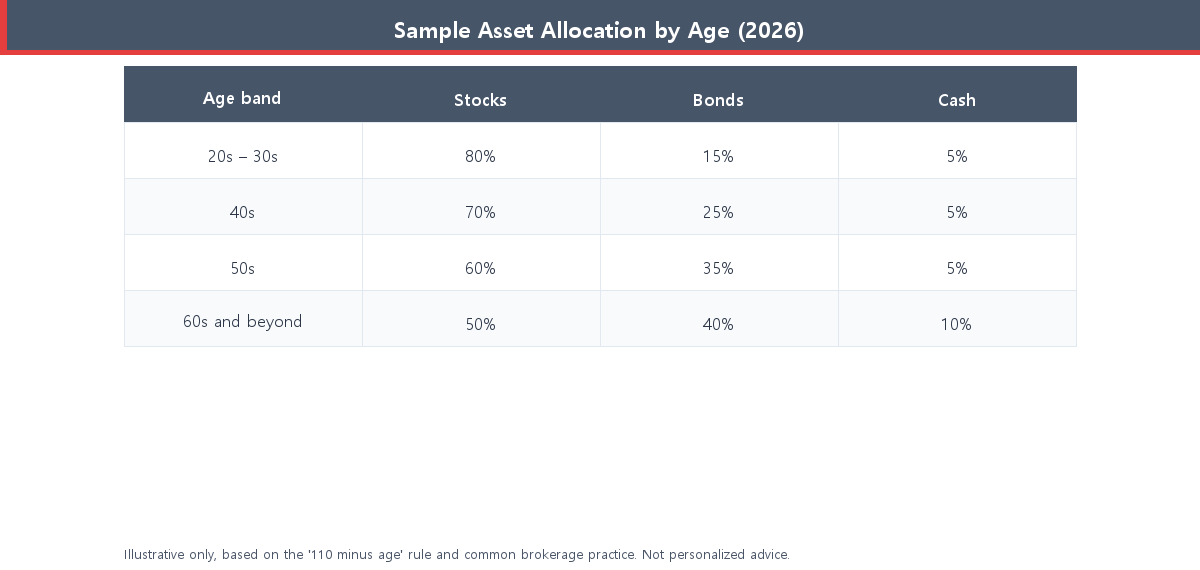

Sample Asset Allocation by Age (2026)

The table below shows illustrative stock/bond/cash mixes by age band, blending the “110 minus age” idea with common practice from major brokerages. These are examples to anchor your thinking, not personalized advice — your own job stability, savings rate, and goals should adjust them.

Long-Run Returns of Each Asset Class

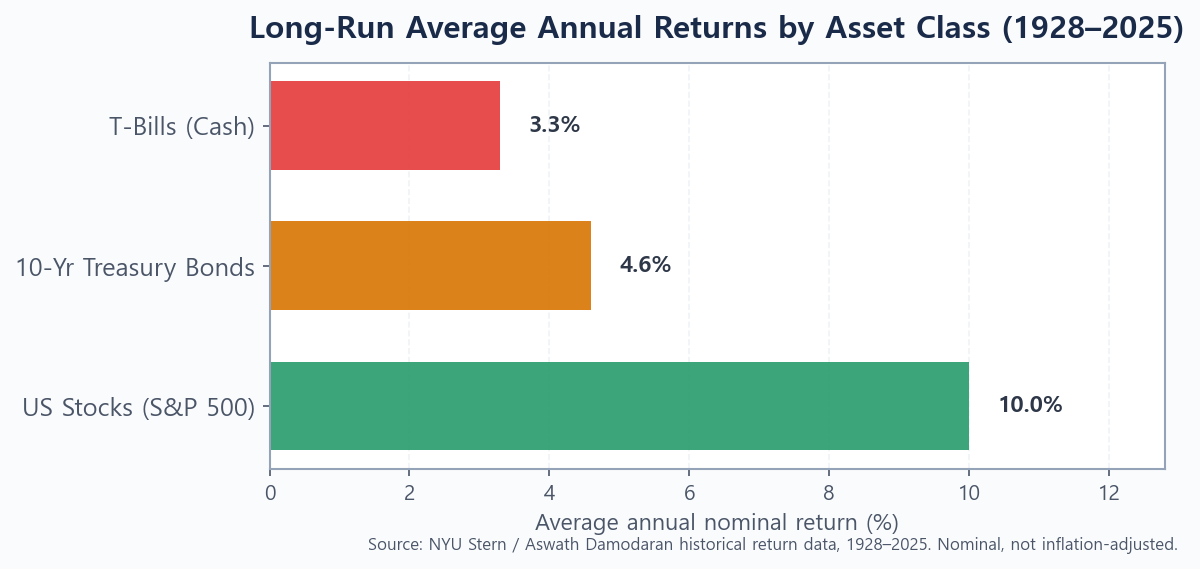

Why hold any stocks at all if they are so volatile? Because over long periods they have paid the most. The chart below shows long-run average annual nominal returns from 1928 to 2025 for US large-cap stocks, 10-year Treasury bonds, and 3-month T-bills (a cash proxy). Higher returns came bundled with bigger swings — that trade-off is exactly what your allocation is meant to balance.

The gap between roughly 10% for stocks and about 3% for cash compounds dramatically over decades. That is the cost of sitting entirely in “safe” assets when you have a long horizon — and the reason a thoughtful mix usually beats hiding in cash. (Source: NYU Stern / Aswath Damodaran historical return data, 1928–2025.)

Building and Rebalancing Your First Portfolio

Once you have chosen a target mix, the implementation can be refreshingly boring. Low-cost, broadly diversified index funds or ETFs let you buy thousands of stocks and bonds in a couple of holdings. The harder part is maintenance: as markets move, your mix drifts away from target, and rebalancing brings it back.

A Simple 4-Step Starter Plan

- Set your target mix. For example, 80% stocks / 15% bonds / 5% cash for a long horizon.

- Pick low-cost funds. A total-market stock fund plus a broad bond fund can cover most of it.

- Automate contributions. Invest a fixed amount on a schedule, regardless of headlines.

- Rebalance about once a year. If stocks grow to 88% of the portfolio, sell a little back toward 80% (or steer new contributions there).

That rebalancing step quietly enforces “buy low, sell high”: you trim what has run up and top up what has lagged, without trying to time the market.

Conclusion: Pick a Mix You Can Hold Through a Downturn

Asset allocation is the closest thing investing has to a free lunch: a deliberate split across stocks, bonds, and cash that shapes your returns and your risk far more than any single pick. For beginners, the winning move is to choose a mix that fits your time horizon and temperament, build it with low-cost funds, and rebalance once a year. The best allocation is not the one with the highest theoretical return — it is the one you can calmly hold when markets fall.

Found this beginner’s guide to asset allocation useful? Bookmark it so you can revisit when the market moves, and check back as we add more practical investing breakdowns.

This article is for informational purposes only and is not investment advice. Do your own research.

6 thoughts on “A Beginner’s Guide to Asset Allocation (2026 Edition)”