For most of the 2010s, the 10-year Treasury yield was a sleepy number that hovered between 1% and 3%. That world is gone. In mid-2026 the 10-year yield sits near 4.5%, and the entire 10-year Treasury yield outlook 2026 now revolves around one question: are we living in a “4% world” that is here to stay? This guide explains where yields stand right now, why a sustained 4%-plus environment changes the math for bond investors, what the 2026 yield curve is signaling, and how the major forecasters see the rest of the year playing out.

Where the 10-Year Treasury Yield Stands in 2026

As of mid-June 2026, the benchmark 10-year Treasury note yields roughly 4.45%–4.49%, down slightly from a one-year high of 4.61% touched on May 18 (Source: CNBC / U.S. Treasury, as of June 15, 2026). The short end of the curve is anchored by the Federal Reserve, which has held its policy rate at a target range of 3.50%–3.75% (Source: Federal Reserve, FOMC, June 2026).

What is striking is how durable the 4% handle has become. Since early March 2026, the 10-year has mostly traded in a 4.0%–4.5% band. Three forces keep it there: sticky inflation that refuses to fall cleanly to target, large federal deficits that flood the market with new bond supply, and a patient Fed in no hurry to cut. For the yield to break back below 4%, the economy would likely need to weaken meaningfully — which is exactly why the “4% world” label has stuck.

What a “4% World” Means for Bond Investors

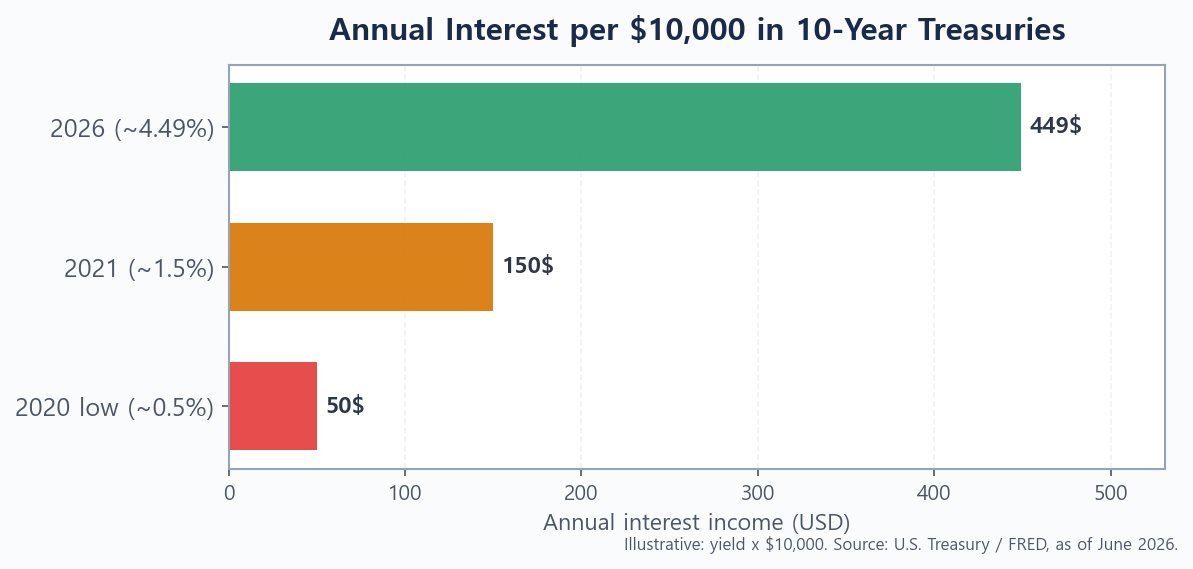

A 10-year yield near 4.5% is not just a headline number — it reshapes the role bonds play in a portfolio. After a decade of near-zero rates, fixed income can finally do its traditional job: pay you a real, meaningful income. The chart below shows just how dramatic the shift has been.

Higher income, at last

At a 4.49% yield, a $10,000 position in 10-year Treasuries throws off about $449 a year in interest. In the 2020 low-rate era, the same $10,000 earned closer to $50. That is roughly nine times more income for holding the same “risk-free” asset. For retirees and conservative savers, this is the most investor-friendly bond environment in over a decade. It is also why parking cash has become a real decision — our comparison of short-term bonds vs. high-yield savings breaks down where to keep money you may need soon.

Price risk cuts both ways

The catch is duration. Bond prices move inversely to yields, and a 10-year note is sensitive to rate changes. If yields rise another half-point, the market price of an existing 10-year bond falls; if yields drop, that bond gains value. In a 4% world, you are being paid a healthy coupon to accept that risk — but you should hold longer maturities only if you can ride out the swings or intend to hold to maturity. Where bonds belong alongside stocks and cash is covered in our beginner’s guide to asset allocation.

The 2026 Yield Curve, Decoded

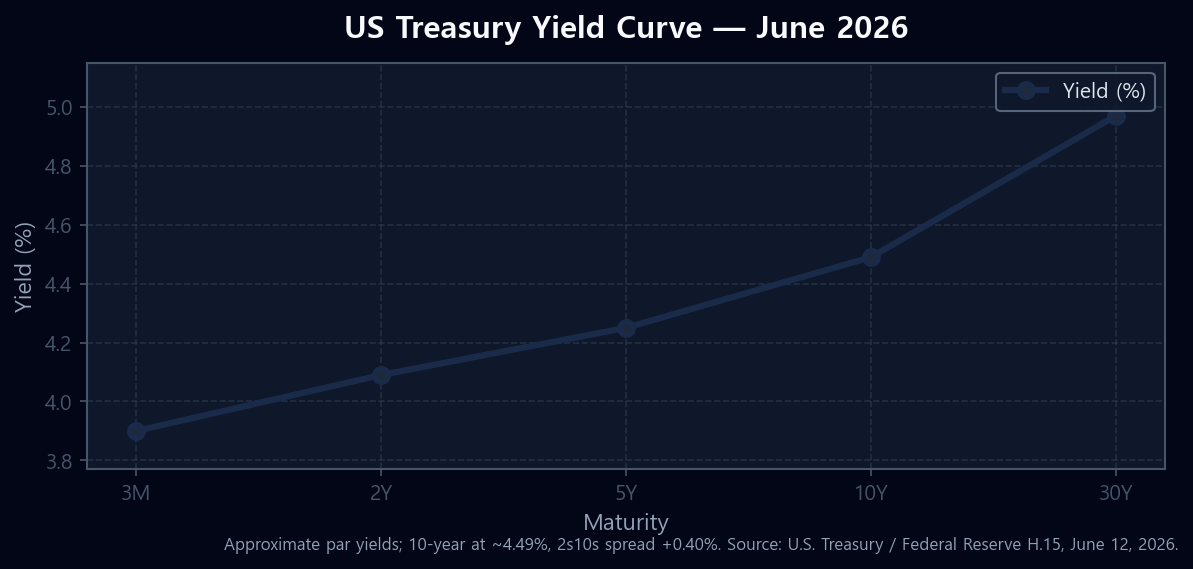

The yield curve — the line connecting Treasury yields from 3-month bills to 30-year bonds — tells you how the market is pricing the future. After being inverted for much of 2023–2024, the 2026 curve has normalized: it now slopes gently upward, with the 10-year (4.49%) yielding more than the 2-year (4.09%), a positive 2s10s spread of about +0.40% (Source: U.S. Treasury / Federal Reserve H.15, June 12, 2026).

A normal, upward-sloping curve is generally read as a healthier signal than an inverted one — the recession alarm that an inverted curve sounds has quieted. The steep climb out to the 30-year (4.97%) also reflects investors demanding extra compensation to lend for decades amid deficit and inflation worries. The video below walks through how Treasuries work and how to think about buying across the curve.

Where Forecasters See the 10-Year Yield Heading

No one knows exactly where the 10-year will end 2026, and the major firms disagree. The table below summarizes their year-end views and the reasoning behind each. Notice that even the most dovish forecast still lands near 3.75% — nobody is calling for a return to the ultra-low yields of the past decade.

The common thread: the path of the 10-year hinges on the Fed and on inflation. If price pressures cool and the Fed eases its policy rate toward a “neutral” level near 3%, yields drift toward the lower end of these ranges. If inflation stays sticky, 4%-plus is the base case. For a deeper look at the rate path itself, see our analysis of whether the Fed will cut rates in 2026 and how Fed rate decisions affect the stock market.

How to Position a Bond Portfolio for a 4% World

You cannot control where yields go, but you can control how your portfolio is built to handle them. A few practical principles for a 4% environment:

- Lock in income with intent. If you believe yields will fall, longer maturities let you secure today’s ~4.5% for years. If you are unsure, shorter notes keep you flexible.

- Use a bond ladder. Spreading purchases across maturities (1, 3, 5, 10 years) smooths reinvestment risk and gives you cash coming due at regular intervals.

- Match duration to your time horizon. Don’t hold a 30-year bond for a 3-year goal; the price swings can hurt if you must sell early.

- Treat Treasuries as ballast, not a bet. Their job is to steady a portfolio when stocks fall — the 4%-plus coupon is a bonus on top of that role.

- Mind the after-tax, after-inflation return. A 4.5% yield is attractive, but what matters is the real return after inflation and taxes.

If you are outside the US and wondering how to actually access these bonds, our guide on how to buy US Treasury bonds as a foreigner covers the practical steps and the tax rules that work in a foreign buyer’s favor.

The Bottom Line on the 2026 Treasury Outlook

The 10-year Treasury yield outlook 2026 points to a market that has settled into a “4% world”: yields near 4.5%, a normalized upward-sloping curve, and forecasts clustered between roughly 3.75% and 4.5% for year-end. For bond investors, that is mostly good news — it means real income is back — as long as you respect duration risk and match maturities to your goals. The single biggest swing factor remains the Fed and the path of inflation, so keep one eye on each FOMC meeting.

This article is for informational purposes only and is not investment advice.