You have money to invest every month and two places to put it: a Roth IRA, the account the tax code clearly favors, and a taxable brokerage account, which lets you invest as much as you want, whenever you want. So which should you fund first? For the large majority of investors in 2026, the answer is refreshingly clear — the Roth IRA wins the first dollar — but there are real exceptions worth knowing before you set up your automatic contributions. This guide walks through the Roth IRA vs. taxable brokerage decision in plain English, gives you a simple funding priority ladder, and shows you exactly when the usual order should flip.

The Short Answer: Fund the Roth IRA First

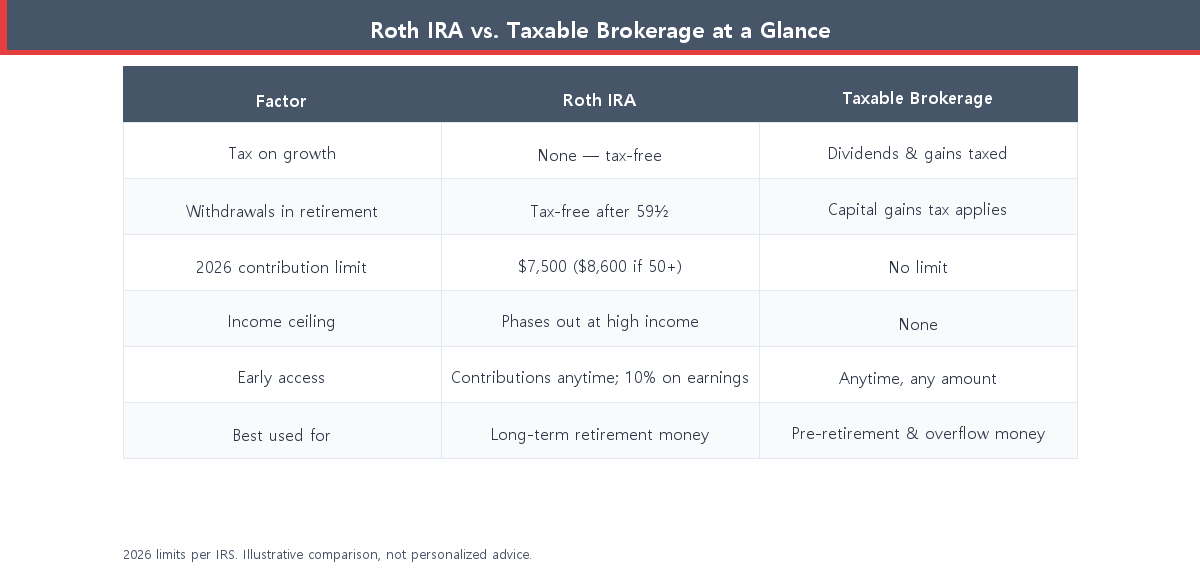

If you have already captured any employer 401(k) match and you are free of high-interest debt, the Roth IRA should generally get your investing dollars before a taxable brokerage account. The reason is simple: a Roth IRA gives you tax-free growth and tax-free withdrawals in retirement, while a taxable brokerage account taxes your dividends and capital gains along the way. Same investments, same market — but one account hands the IRS a slice of your returns every year, and the other does not. When two accounts hold identical funds and only one is taxed, you fund the untaxed one first.

Roth IRA vs. Taxable Brokerage in Plain English

A Roth IRA is a retirement account you fund with money you have already paid income tax on. Once it is inside, your investments grow tax-free, and qualified withdrawals after age 59½ are completely tax-free. The trade-off is rules: there is an annual contribution limit, an income ceiling above which you cannot contribute directly, and a 10% penalty on earnings withdrawn early. One underrated feature — you can always withdraw your own contributions (not the earnings) at any time, tax- and penalty-free.

A taxable brokerage account is the opposite in spirit: total flexibility, no perks. You can invest any amount, add or withdraw whenever you like, and use the money for any goal — a house, a sabbatical, early retirement. The cost of that freedom is taxes. You owe tax on dividends each year and on capital gains when you sell, although investments held longer than a year qualify for lower long-term capital gains rates.

Why the Roth IRA Usually Wins the First Dollar

Put the two side by side and the Roth IRA’s edge is hard to ignore. The advantage is not that the Roth holds better investments — you can buy the same low-cost index funds in either account — but that it shelters those investments from a yearly tax drag that quietly compounds against you. Keeping that drag near zero is one of the highest-return moves an ordinary investor can make, right alongside the decision to keep fund costs low.

Notice what the comparison does not say: the taxable account is never useless. It is the right tool for goals before retirement and for money beyond what the Roth can hold. The point is ordering. When you can only fund one this month, the tax-free account should fill up first.

The Funding Priority Ladder

Financial planners tend to agree on a rough order for where each new dollar should go. It is less about Roth-versus-brokerage in isolation and more about making sure the highest-value dollars get claimed before the flexible-but-taxable ones. Here is the ladder most investors can follow in 2026.

The taxable brokerage account sits at the bottom of this ladder for a reason — not because it is bad, but because everything above it offers a tax break or a guaranteed return (an employer match is an instant 50–100% on your money; paying off a 22% credit card is a guaranteed 22%). You reach the brokerage account once those better deals are exhausted. If you are just getting going and the ladder feels intimidating, you can begin small — even starting with as little as $100 builds the habit that matters most.

The Real Cost of Skipping the Roth

The yearly tax drag on a taxable account sounds trivial until you let it compound for decades. Consider an investor who contributes the 2026 Roth limit of $7,500 a year for 30 years and earns a 7% annual return. In a tax-free Roth, that grows to roughly $708,000. In a taxable account where taxes on dividends and gains shave the effective return to about 6%, the same contributions grow to roughly $593,000 — a gap of about $115,000, created by nothing but taxes.

These figures are illustrative — your real numbers depend on your tax bracket, the funds you hold, and how often they distribute gains — but the direction never changes. The longer your time horizon, the more the tax-free account pulls ahead. That is precisely why the Roth deserves your dollars first when retirement is the goal.

When a Taxable Brokerage Should Come First

The standard order flips in a few legitimate situations. Fund the taxable brokerage account first when:

- You will need the money before retirement. Saving for a home down payment, a wedding, or a career break in five years? The Roth’s early-withdrawal penalty on earnings makes a taxable account the cleaner choice for goals you’ll spend on before 59½.

- You have already maxed the Roth IRA. The 2026 contribution limit is $7,500 ($8,600 if you are 50 or older). Once you’ve hit it, additional long-term money has nowhere to go but a taxable account — and that is exactly what it is for.

- Your income is above the Roth limit. Direct Roth contributions phase out for single filers between $153,000 and $168,000 of modified adjusted gross income in 2026, and for married couples filing jointly between $242,000 and $252,000. Above those ranges you’ll need a different route (such as a “backdoor” Roth) or you’ll lean on the taxable account.

- You want true flexibility. No contribution caps, no withdrawal rules, and access to long-term capital gains rates make the taxable account a strong complement once the tax-advantaged space is full.

2026 Roth IRA Limits You Need to Know

Before you set your automatic contribution, check the current numbers so you don’t accidentally over- or under-fund. For 2026, the IRS set the Roth IRA contribution limit at $7,500 for those under 50, with an extra $1,100 catch-up contribution for those 50 and older, bringing their total to $8,600 (Source: IRS, 2026 limits). Direct contributions phase out at the income ranges noted above. Whichever account you prioritize, what you hold inside it — and how you balance stocks and bonds — matters just as much; if you haven’t settled that yet, start with your overall asset allocation.

Conclusion: Tax-Free First, Flexible Second

So, Roth IRA vs. taxable brokerage — which should you fund first? For most investors saving for retirement in 2026, the Roth IRA comes first: it shelters your growth from a tax drag that can quietly cost six figures over a working lifetime. The taxable brokerage account earns its place right after, as the flexible home for money beyond the Roth’s limits or money you’ll need before retirement. Capture your employer match, clear high-interest debt, fill the Roth, then let the taxable account carry the rest. Get that order right and you keep more of every dollar your investments earn.

Found this Roth IRA vs. taxable brokerage breakdown useful? Bookmark it and check back as we publish more practical, data-backed investing guides.

This article is for informational purposes only and is not investment advice. Do your own research.