For most of the last decade, a strong US dollar was the quiet backdrop to almost every investing decision. In 2025 and 2026 that backdrop changed: the dollar posted its steepest first-half decline in more than fifty years and slid to a near four-year low. If you hold stocks, gold, or any international funds, a weak dollar affects your investment portfolio in ways that rarely make the headlines — sometimes helping you, sometimes quietly eroding what your money can buy. This guide explains, in plain terms, what a falling dollar does to each asset you own and what a long-term investor should sensibly do about it.

What “A Weak Dollar” Actually Means

A “weak” or “strong” dollar is always relative to other currencies. The most common measure is the US Dollar Index (DXY), which tracks the dollar against a basket of major currencies like the euro, yen, and pound. When the DXY falls, it takes more dollars to buy the same euro or yen — the dollar has weakened. When it rises, the dollar buys more.

Why does this matter to an investor who only buys US stocks? Because the value of the dollar quietly reprices almost everything: the foreign earnings of American companies, the dollar price of gold and oil, the returns on your international funds, and the real-world purchasing power of your cash. A currency move is not a side issue — it is a force acting on your whole portfolio at once.

Where the Dollar Stands in 2026

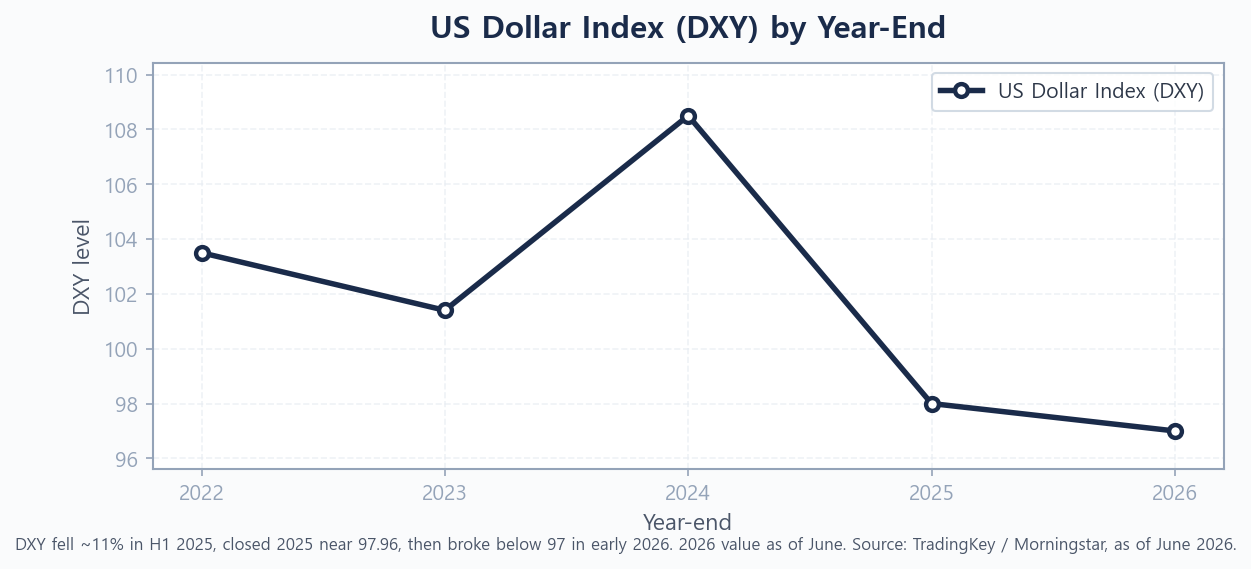

Context explains why this topic is suddenly everywhere. After years of strength, the dollar index fell roughly 11% in the first half of 2025 — its worst first-half performance since 1973. It closed the year near 97.96, then broke below the key 97 level in early 2026, briefly touching a near four-year low around 95.5 before settling into a 97–100 range as safe-haven demand ebbed and flowed (Source: TradingKey / Morningstar, as of June 2026).

The chart makes the turn obvious: a firm dollar through 2022–2024, then a sharp drop into 2025 and 2026. Much of this slide is tied to expectations that the Federal Reserve will keep easing — currencies tend to weaken when their interest rates are expected to fall. If you want the mechanics behind that link, see will the Fed cut rates in 2026 and how Fed rate decisions affect the stock market.

How a Falling Dollar Moves Each Part of Your Portfolio

A weaker dollar does not push every holding in the same direction. It travels through your portfolio asset by asset, and the effects can pull against one another.

US stocks (the S&P 500) — a mixed picture

Roughly 40% of S&P 500 revenue is earned outside the United States (Source: Morningstar, 2026). When those foreign sales are converted back into a falling dollar, they translate into more dollars — a tailwind for large multinational exporters like technology and consumer-brand companies. The flip side: firms that import goods or earn mostly at home gain little, and a falling dollar can add to inflation, which complicates the picture. So a weak dollar is generally a mild positive for US large-caps as a group, but it is far from a guarantee.

International and emerging-market stocks — the clearest winner

This is where the effect is most direct. When you own an unhedged international or emerging-market fund, you hold assets priced in foreign currencies. If those currencies rise against the dollar, your returns get an extra boost on top of the local market’s gains. Emerging-market equities often trade as a near-mirror image of the dollar index, and history rhymes here: during the 2002–2007 weak-dollar cycle, the MSCI Emerging Markets index roughly quadrupled (Source: J.P. Morgan AM / BlackRock, 2026). A weak dollar is the single strongest argument for not keeping 100% of your stocks at home.

Gold and commodities

Gold is priced in dollars worldwide, so when the dollar falls, gold becomes cheaper for buyers using other currencies — which tends to lift demand and price. That dynamic helped drive gold to repeated record highs, trading well above $4,600 an ounce in 2026 (Source: World Gold Council / Advantage Gold, 2026). The same logic applies to globally priced commodities like oil and copper: a cheaper dollar often means firmer commodity prices.

Bonds and cash

For bonds, the dollar’s path matters most through interest rates. The same rate cuts that weaken the dollar tend to support existing bond prices, while reducing the yield on new bonds and savings. Your US cash, meanwhile, faces a subtle problem covered below. If you are weighing where to park safer money in this environment, short-term bonds vs. high-yield savings and how to buy US Treasury bonds as a foreigner both walk through the trade-offs.

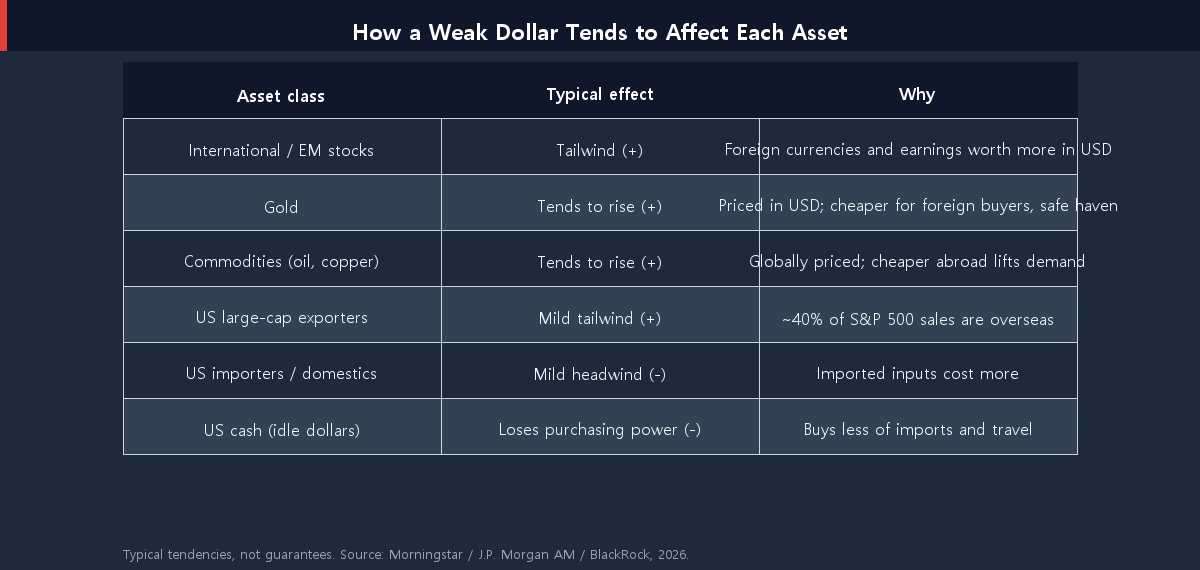

Winners and Losers at a Glance

It helps to line up the typical tendencies side by side. The table below summarizes how each asset class usually responds to a sustained dollar decline — tendencies, not promises, since markets price in expectations early.

Notice that income-oriented and international assets cluster on the “tailwind” side. That is one reason many investors revisit their global mix — and their income holdings such as the best high-yield dividend ETFs for 2026 — when the dollar turns lower.

The Hidden Risk No One Mentions: Your Purchasing Power

Here is the part that rarely appears in market commentary. Even if your portfolio’s dollar value holds steady, a weaker dollar quietly reduces what those dollars can buy. Imported goods, overseas travel, and globally priced commodities all cost more when the dollar falls. In other words, a flat account balance during a falling-dollar year is not really flat — it has lost some real-world purchasing power.

This is why “keep everything in dollars and cash” can feel safe while quietly costing you. Cash carries no market risk, but in a weak-dollar, higher-inflation regime it carries currency risk. The antidote is not to panic-sell dollars; it is to make sure some of your portfolio is denominated in other currencies or in real assets that historically hold value when the dollar slips. That is a diversification decision, not a trade.

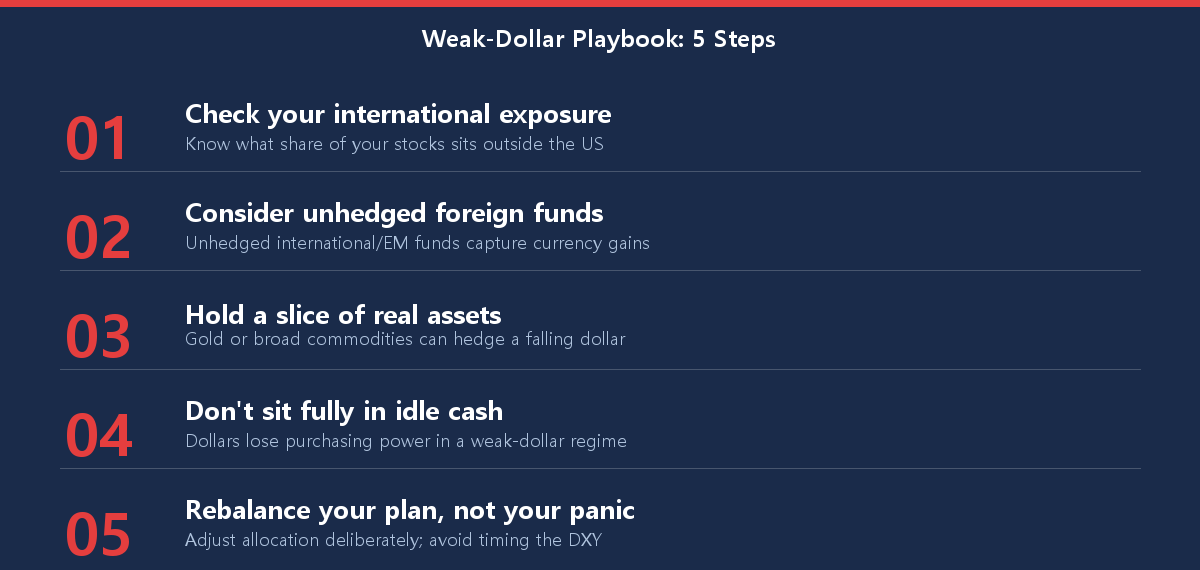

What Long-Term Investors Can Actually Do

You do not need to become a currency trader. A few measured adjustments capture most of the benefit while keeping risk in check.

The throughline is simple: a weak dollar rewards investors who already hold a globally diversified mix and punishes those who are unknowingly all-in on the dollar. If your current split between US, international, and real assets is unclear, the cleanest starting point is our beginner’s guide to asset allocation, which shows how a currency tilt fits into a complete plan rather than being chased on its own.

Conclusion: A Weaker Dollar Is a Tilt, Not an Alarm

A weakening dollar is not a crisis to flee — it is a shift in the wind that tilts your portfolio’s returns. It tends to help international stocks, gold, commodities, and US exporters, while quietly eroding the purchasing power of idle cash. The investors who handle it best are not the ones who time the DXY week to week; they are the ones who already hold a sensible global mix and simply make sure they are not accidentally concentrated in a single currency. Check your international exposure, hold a slice of real assets, and let diversification do the work.

Found this useful? Bookmark it so you can revisit when the dollar makes headlines again.

This article is for informational purposes only and is not investment advice. Do your own research before making any investment decision.