Most investors walked into 2026 expecting rate cuts. Six months later, the question has flipped: will the Fed hike rates in 2026 instead? After an energy-driven inflation scare, the latest projections show a committee that has quietly stopped talking about cuts and started pricing in a higher-for-longer world — one that changes the math on your bonds, your cash, and your stocks.

This guide breaks down what actually shifted, what the June 2026 dot plot says, and how a higher-for-longer scenario filters down to a normal portfolio — without you having to predict the Fed’s next move.

Why a Rate Hike Is Suddenly on the Table

At the June 17, 2026 meeting — Chair Kevin Warsh’s first — the Federal Open Market Committee (FOMC) held its target range at 3.50%–3.75% in a unanimous 12–0 vote (Source: Federal Reserve FOMC statement / CNBC, June 2026). On the surface, “no change” sounds calm. The real story was in the projections that came with it.

The catalyst was inflation. After the February 27, 2026 onset of the U.S.–Iran conflict, an energy and supply shock pushed prices back up, away from the Fed’s 2% goal. When inflation re-accelerates, the central bank’s job description tilts from “support growth with cuts” to “defend price stability” — and that is exactly the pivot the market is now bracing for. It is the same transmission mechanism we explain in how Fed rate decisions affect the stock market: rates set the price of money for everyone.

What the June 2026 Dot Plot Actually Shows

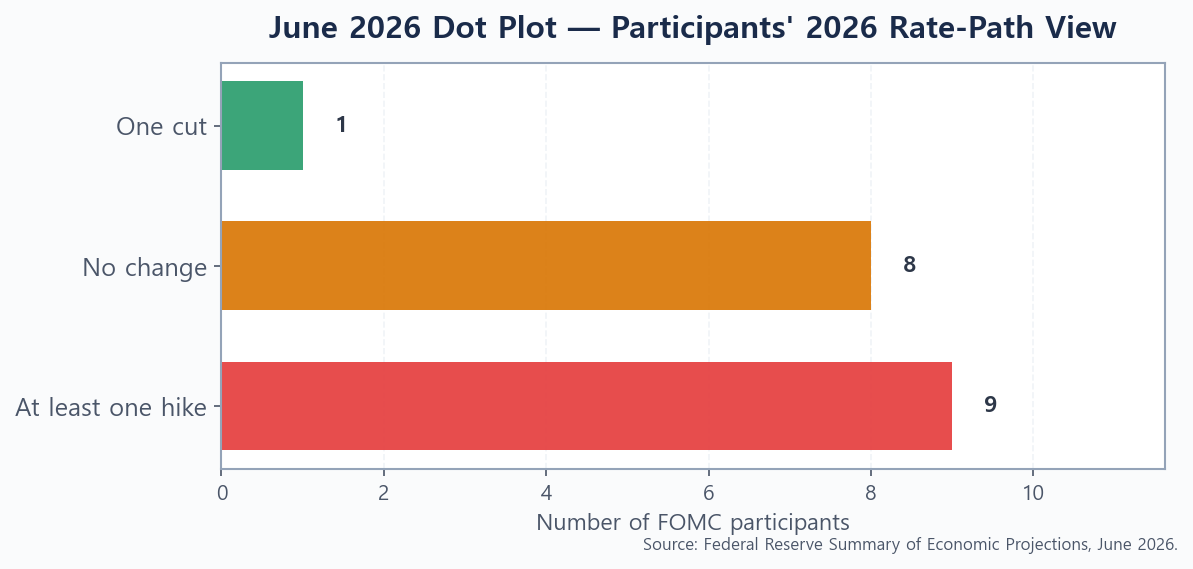

The dot plot — part of the Fed’s quarterly Summary of Economic Projections — lets each official mark where they think the policy rate should sit. In June 2026 it told a striking story: the median participant now expects rates to end the year higher than today, a full reversal from March, when the median still implied a cut. Most officials now see the year-end benchmark landing between 3.6% and 4.1% (Source: Federal Reserve SEP / StockTitan, June 2026).

The median flipped from a cut to a hike

The split among participants captures how decisively the mood changed: 8 expected no change, just 1 still saw a cut, and 9 anticipated at least one hike in 2026 (Source: Federal Reserve SEP, June 2026). When a committee that was forecasting easing three months ago now has a near-majority penciling in tightening, that is not noise — it is a genuine regime shift in expectations. This is the mirror image of the question we tackled earlier in will the Fed cut rates in 2026; the same dots that once pointed down now point up.

Markets now price one hike by October

Investors are not waiting for confirmation. Fed funds futures now price in roughly one 25-basis-point hike by October 2026, with no further moves expected through 2027 (Source: CNBC, June 2026). Bond markets moved first: the 10-year Treasury yield closed at 4.48% on June 17, and the 30-year topped 5.19% in May — the highest in years. A higher-for-longer path is what cements the kind of elevated-yield environment we map out in the 10-year Treasury yield outlook for 2026.

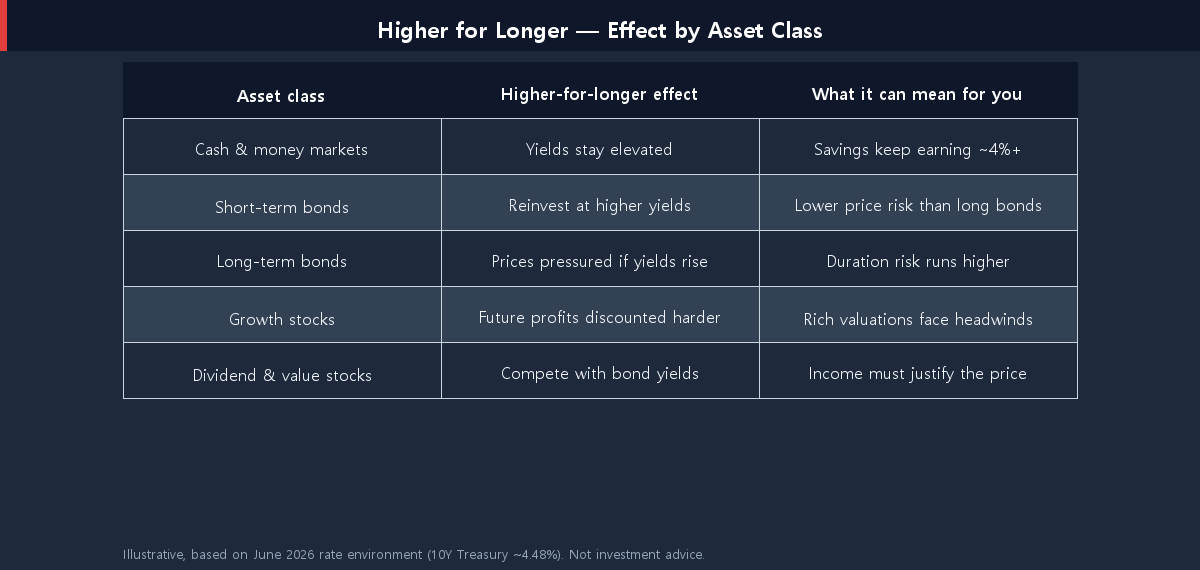

What “Higher for Longer” Means for Your Portfolio

“Higher for longer” is shorthand for a simple idea: instead of rates falling back toward the lows of the past decade, they stay elevated for an extended stretch — and might even nudge up. That single assumption ripples through every asset class differently.

For savers, the news is mostly good: cash and money-market yields stay generous, which keeps the trade-off in short-term bonds vs. high-yield savings firmly in play. For bondholders, duration is the dividing line — short maturities reinvest at attractive rates, while long bonds carry more price risk if yields climb. For stocks, higher rates discount future profits more heavily, which is why richly valued growth names tend to wobble while income-paying and value stocks — including some of the best high-yield dividend ETFs for 2026 — can hold up better when bonds are competing for your dollars.

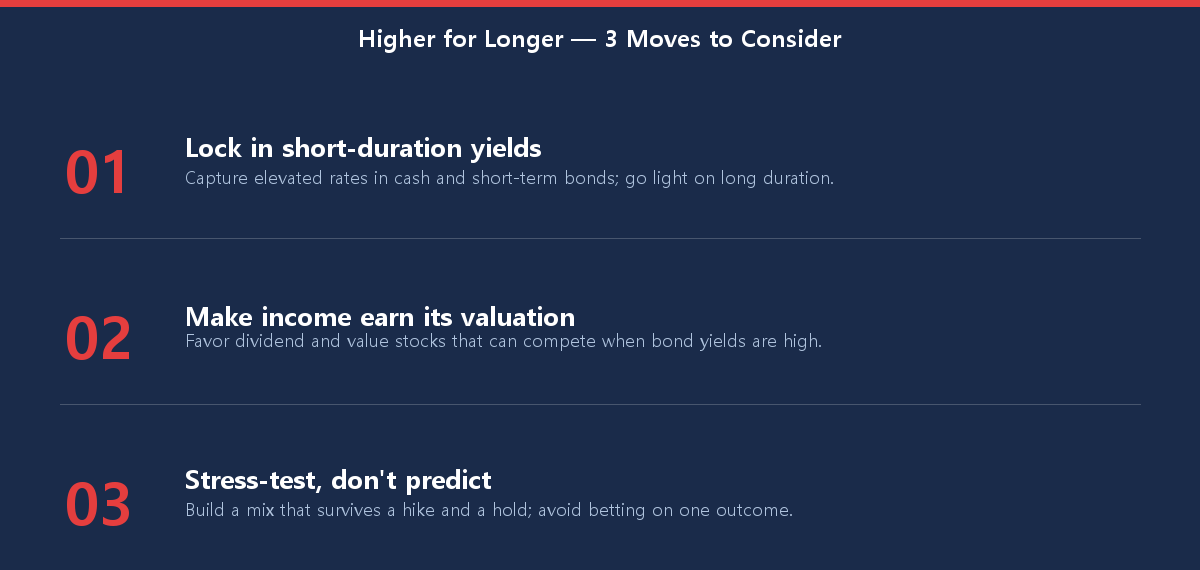

Three Moves to Consider in a Higher-for-Longer World

You do not need to outguess the FOMC to respond sensibly. The goal is a portfolio that behaves reasonably whether the Fed hikes once or simply holds.

Notice that none of these moves is a bet on a specific outcome. They are about positioning for the range of likely paths — locking in today’s yields where it is safe to do so, demanding that income justify a stock’s price, and keeping the overall mix resilient. That discipline is the heart of any durable beginner’s guide to asset allocation.

How Likely Is an Actual Hike?

Here is the part the headlines tend to skip: a dot plot is a forecast, not a promise. The June projections lean toward tightening, but they are a snapshot of opinion on one day. If the energy shock fades and inflation cools through the autumn, the same officials who penciled in a hike can erase it just as quickly — exactly what happened in reverse earlier this year.

The base case priced by markets is modest: at most one quarter-point hike, then a long pause. That is a meaningful shift in tone, not a return to aggressive tightening. So the honest answer to “will the Fed hike rates in 2026?” is *possibly, once* — and the more useful question is whether your portfolio can shrug off either a hike or a hold without forcing you to react.

Conclusion: Position for the Path, Not the Prediction

Will the Fed hike rates in 2026? The committee has clearly opened the door, with nine officials now expecting at least one increase and markets pricing a hike by October. But a higher-for-longer scenario is less about nailing the exact decision and more about accepting that elevated rates may be the backdrop for a while. Keep your cash earning, stay thoughtful about bond duration, ask your stocks to justify their valuations — and let a steady plan, not a single Fed meeting, set your course.

This article is for informational purposes only and is not investment advice. Rate projections and market pricing can change quickly; verify current figures with primary sources before making decisions.