In 2026, the bond market is finally paying you to show up — but it is also asking a sharper question than it has in years. A 10-year US Treasury yields around 4.3%, an investment-grade corporate bond pays roughly 5.3%, and a high-yield (“junk”) bond dangles close to 7.8%. On paper, moving from Treasuries to corporates looks like free money. It isn’t. The whole debate over corporate bonds vs Treasuries in 2026 comes down to one thing: that extra yield is compensation for risk, and right now the market is paying unusually little of it. This guide breaks down exactly how much extra you earn, what you give up to get it, and how to decide whether the trade is worth it for your money.

What’s the Difference Between Corporate Bonds and Treasuries?

A US Treasury is a loan to the federal government. It is considered the safest, most liquid bond on earth, and the yield it pays is treated as the “risk-free rate” — the baseline everything else is measured against. A corporate bond is a loan to a company. Because a company can run into trouble in ways the US government effectively cannot, investors demand extra yield to hold its debt. That extra yield is called the credit spread, and it is the single most important number in this whole comparison.

Put simply: if a corporate bond yields 5.3% and a comparable Treasury yields 4.3%, the credit spread is about 1.0% (or 100 basis points). You are being paid roughly 1% a year to take on the chance that the company stumbles. Whether that is generous or stingy is the heart of the matter.

Investment-Grade vs. High-Yield

Corporate bonds split into two very different worlds, graded by agencies like Moody’s, S&P, and Fitch:

- Investment-grade (IG): bonds from financially solid companies (rated BBB-/Baa3 and above). Lower yield, low default risk. In 2026 these yield roughly 5.0%–5.5%.

- High-yield (HY): bonds from weaker or more leveraged companies (rated BB+ and below), also called “junk.” Higher yield, meaningfully higher default risk. In 2026 these yield roughly 7.5%–8.0%.

Lumping these together is the most common mistake in this debate. An IG corporate is a mild step up in risk from a Treasury; a high-yield bond is a different animal that behaves much more like a stock when markets get scared.

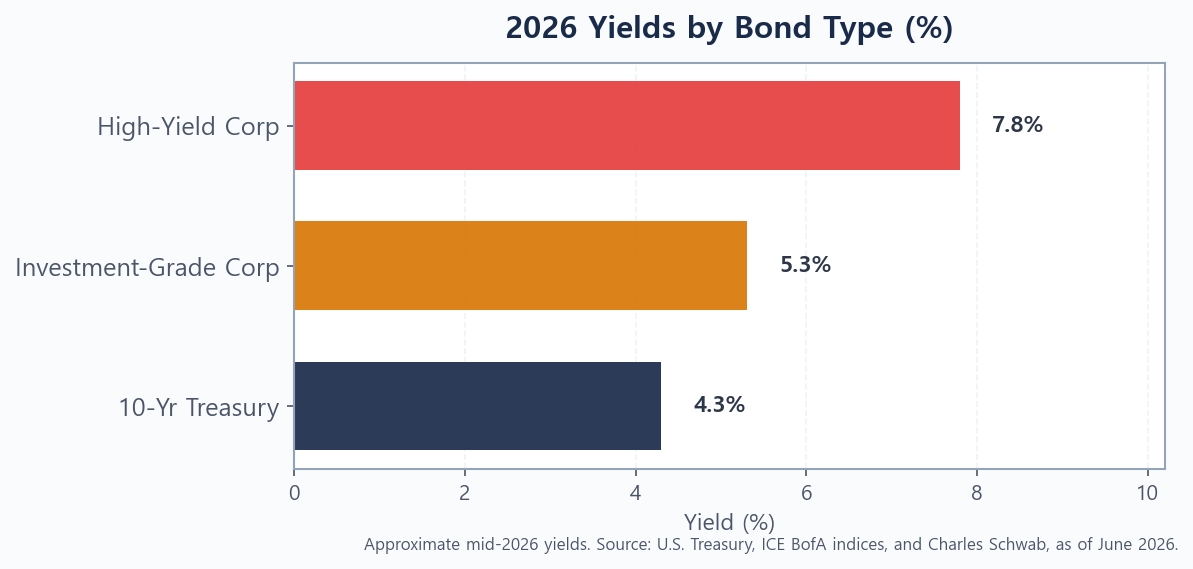

2026 Yields: How Much Extra Do Corporate Bonds Pay?

Here are the headline numbers as of mid-2026. The 10-year Treasury sits near 4.3%, investment-grade corporates yield about 5.3%, and high-yield bonds pay roughly 7.8% (Source: U.S. Treasury, ICE BofA indices, and Charles Schwab, as of June 2026).

The chart shows the reward clearly: about +1% a year for stepping into investment-grade, and about +3.5% a year for stepping all the way into high-yield. Over a decade, an extra 1% compounds into real money, and an extra 3.5% is enormous. But yield is only the part you see. The risk is the part you don’t — until it shows up all at once.

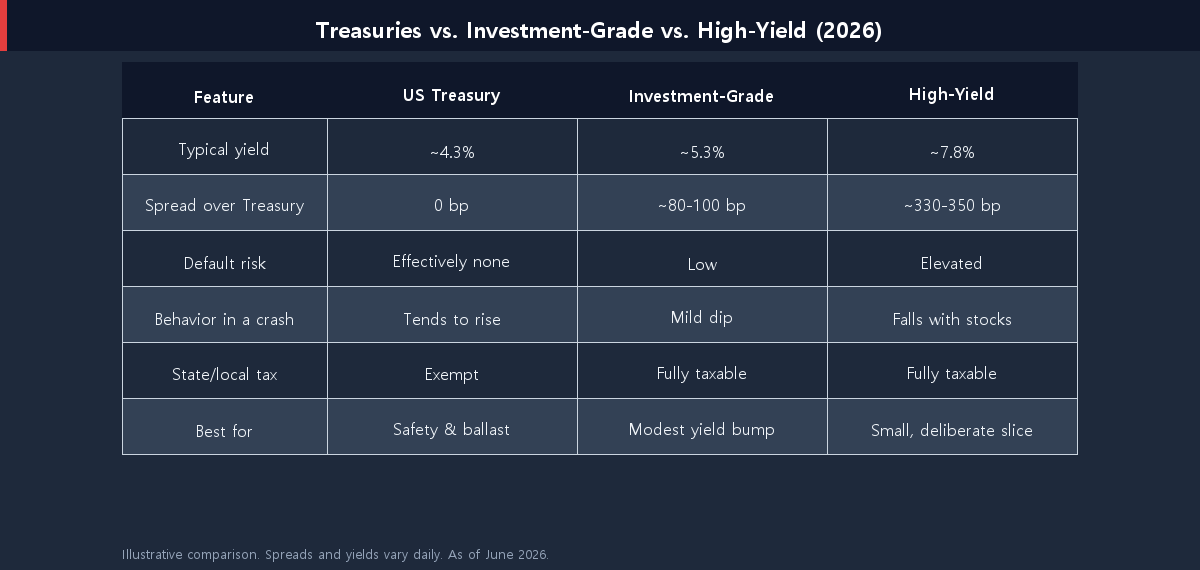

Side-by-Side: Treasuries vs. Investment-Grade vs. High-Yield

Headline yield is one column of many. When you line all three up across the features that actually move your returns, the trade-offs come into focus.

Two columns deserve special attention. First, state tax: Treasury interest is exempt from state and local income tax, while corporate-bond interest is fully taxable. In a high-tax state, that quietly narrows the real after-tax gap between a Treasury and an IG corporate. Second, behavior in a crash: when markets panic, Treasuries tend to rise as investors flee to safety, while high-yield bonds fall alongside stocks. The bond meant to protect you can become the bond that hurts you — exactly when you need protection most.

The Catch — Why 2026 Spreads Are So Tight

Here is the detail most “corporate bonds pay more!” articles skip. The all-in yields are attractive in 2026, but that is mostly because Treasury yields themselves are high. The spread — your actual pay for taking credit risk — is unusually thin.

In early 2026, the investment-grade option-adjusted spread sat near 80 basis points, close to the tightest level in roughly 25 years and well below the long-term average of about 150 bp (Source: ICE BofA / PineBridge, 2026). High-yield spreads have been similarly compressed, with the index closing recent months under 3% versus a 20-year average near 4.9%. In plain terms: you are being paid below-average compensation for above-average uncertainty.

Why so tight? Corporate balance sheets are solid, default rates are low (high-yield defaults are running around 1.5%–2% in 2026 versus a 4.5% long-run average), and demand from pensions and insurers is relentless because the all-in yields look good. That can persist for a long time. The risk is asymmetric, though: when spreads are this narrow, there is little room to tighten further and a lot of room to widen if the economy slows. A move higher in spreads pushes corporate-bond prices down — and that often coincides with the Fed’s path shifting, so it is worth tracking whether the Fed cuts rates in 2026.

If your goal is simply a safe place to earn a solid yield, you may not need credit risk at all. A plain Treasury already pays around 4.3%, and you can learn the mechanics in our guide on how to buy US Treasury bonds.

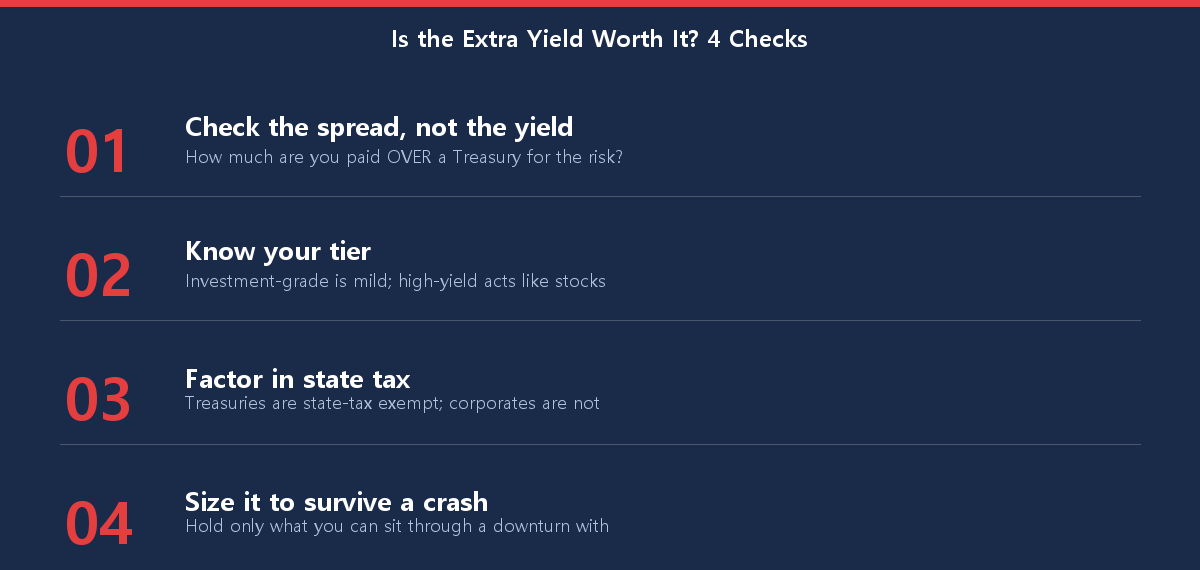

Is the Extra Yield Worth the Risk? A Simple Decision Guide

The honest answer is “it depends” — but it depends on a small number of factors you can actually check. Walk through the steps below before you reach for the higher number.

For most long-term investors, a sensible middle path is to keep Treasuries as the ballast that protects you in a downturn, add a measured slice of investment-grade corporates for a modest yield bump, and treat high-yield as a small, deliberate position rather than a core holding. Where this fits in your overall plan is a question of proportion — see our beginner’s guide to asset allocation for how the safe-money sleeve should be sized.

Three Mistakes Investors Make Reaching for Yield

- Treating high-yield as “just bonds.” Junk bonds can drop 20%+ in a recession. They diversify a stock portfolio far less than Treasuries do.

- Ignoring the spread, chasing the yield. A 7.8% headline means little if you are only paid 3% over Treasuries for genuine default risk. Always ask what you’re being paid over the risk-free rate.

- Forgetting taxes. The state-tax exemption on Treasuries can erase much of an IG corporate’s edge for investors in high-tax states.

Conclusion: Get Paid for Risk You Understand

Weighing corporate bonds vs Treasuries in 2026 isn’t about which one “wins.” Treasuries give you a ~4.3% risk-free yield, state-tax relief, and genuine protection when markets fall. Investment-grade corporates add about 1% for a mild, well-compensated step up in risk. High-yield offers a tempting ~3.5% extra — but with tight spreads and equity-like downside, it asks you to take real risk for below-average pay. The right move is to take credit risk only where you understand it and in sizes you can sit through a downturn with. If your real goal is a safe parking spot for cash, compare the options in short-term bonds vs. high-yield savings before you reach for corporate yield.

Found this helpful? Bookmark it and revisit when spreads move — the answer changes as the cycle does.

This article is for informational purposes only and is not investment advice. Do your own research.