For the first time in years, cash and short bonds actually pay you something. In mid-2026 a short-term Treasury yields roughly 4%, and the question many investors are asking is simple: if I can get 4% with almost no price risk, why would I lock my money into a 10- or 30-year bond for only a little more? That instinct is exactly right. Understanding why short-duration bonds make sense in a 4% Treasury world comes down to one idea most beginners overlook — duration, the hidden lever that decides how much your bonds bounce around when interest rates move. This guide explains it in plain language and shows why staying short is one of the best risk-adjusted deals on the board in 2026.

What “Short Duration” Actually Means

“Duration” sounds technical, but the everyday version is easy: it measures how sensitive a bond’s price is to changes in interest rates. The rule of thumb is that for every 1% rise in rates, a bond falls in price by roughly its duration in percent. A bond with a duration of 2 years drops about 2% if rates rise 1%; a bond with a duration of 17 years drops about 17%.

Short-duration bonds are simply those that mature soon — Treasury bills and notes maturing in roughly two years or less, or short-term bond ETFs that hold a basket of them. Because your money comes back quickly, the price barely flinches when rates move. Long-duration bonds — 10-, 20-, or 30-year Treasuries — do the opposite: they pay a bit more, but their prices swing violently when rates change. So the core decision isn’t really “bonds or no bonds.” It’s how much duration risk you are being paid to take — and in 2026, the answer is “not much.”

The 4% World: Why the Short End Is the Sweet Spot

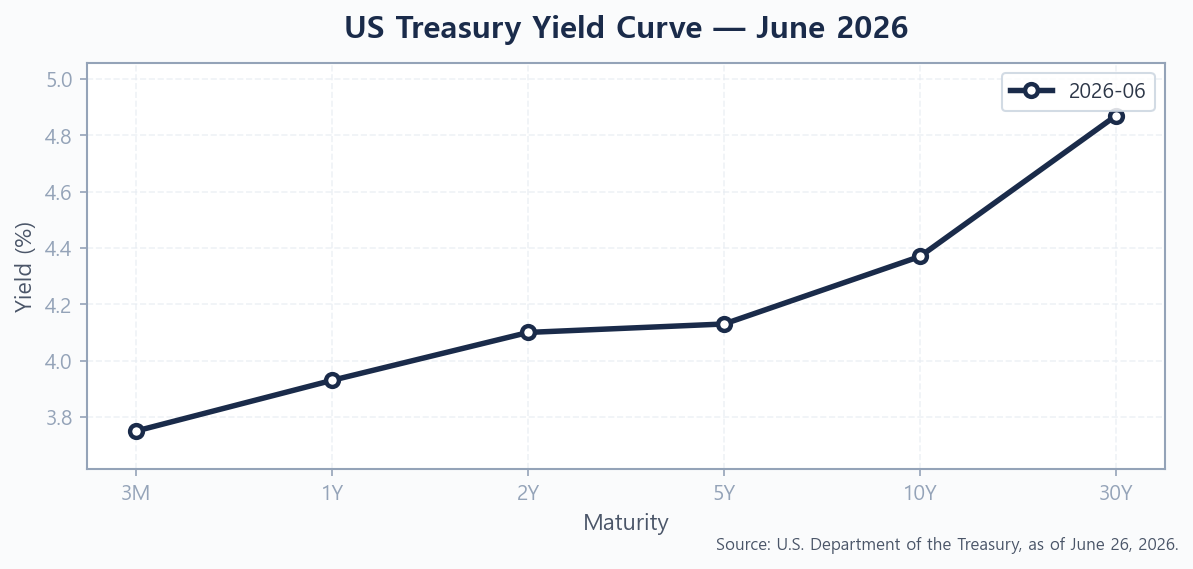

Look at the actual numbers. As of late June 2026, the US Treasury curve runs from about 3.75% on a 3-month bill up to 4.87% on the 30-year bond, with the 2- and 5-year notes sitting right around 4.1% (Source: U.S. Department of the Treasury, June 26, 2026). The curve is upward-sloping but remarkably flat in the middle — you are paid almost the same yield at 2 years as at 5 years.

Here is the punchline of the whole article. Moving from a 2-year note (~4.1%) all the way out to the 30-year bond (~4.87%) buys you less than one extra percentage point of yield — but it multiplies your price risk many times over. You are taking a mountain of duration risk for a hill of extra income. When the short end already pays roughly 4%, the long end has to clear a very high bar to be worth it, and right now it doesn’t. For a deeper look at where the long end might head, see our 10-year Treasury yield outlook for 2026.

Duration Risk: How Much a Rate Move Really Costs

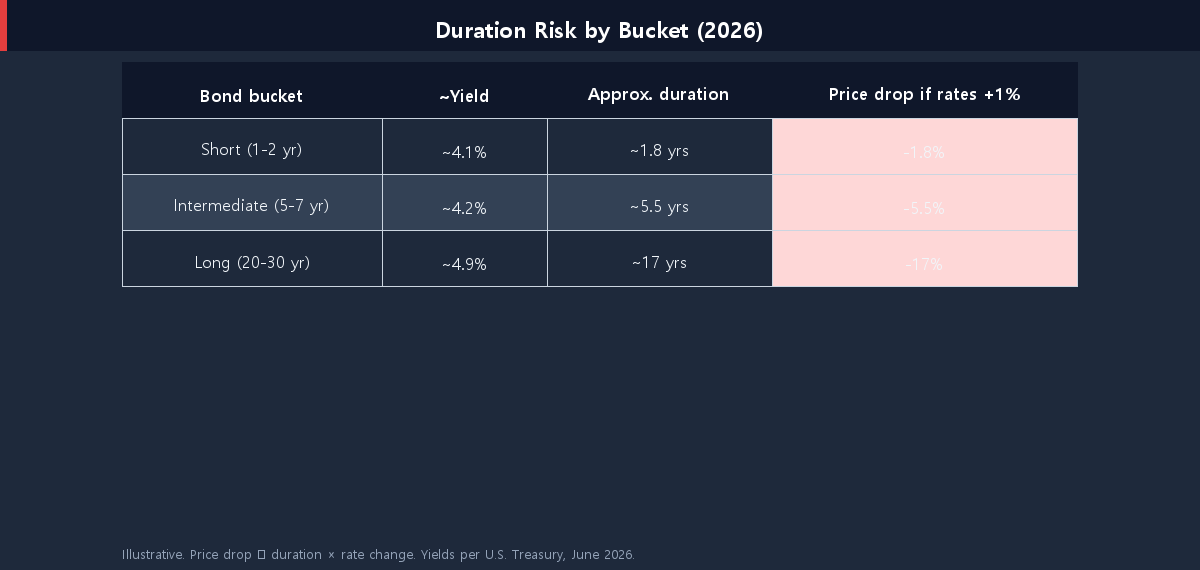

Yield is what you see; duration is what you feel when rates move. The table below lines up three buckets — short, intermediate, and long — across the yield they pay and what happens to their price if rates rise just 1%.

The asymmetry is stark. The long bond pays only about 0.9% more than the short bucket, yet it can lose roughly 17% of its value on a 1% rate increase — more than ten times the short bucket’s drop. In a year when the Fed’s next move is still uncertain, that is a lot of risk to shoulder for a sliver of extra yield. Short-duration bonds let you collect almost the same income while keeping your principal steady, which is why their historical return-per-unit-of-risk (Sharpe ratio) tends to beat longer maturities when the curve is flat like this.

The Trade-Off You Accept: Reinvestment Risk

Staying short is not a free lunch, and being honest about the downside is what separates a strategy from a fad. The price you pay for low duration is reinvestment risk: when your short bond matures, you have to reinvest the proceeds at whatever rate exists then. If the Fed cuts aggressively, the 4% you enjoy today could become 3% — or less — when you roll over.

That is a real consideration, but notice the shape of the bet. With a short bond, the worst case is “I earn a great rate now and a lower-but-still-decent rate later.” With a long bond, the worst case is “rates rise and I’m underwater 15% on paper for years.” For most investors, locking in a strong yield today and accepting some uncertainty about tomorrow is the more comfortable risk. If you think rate cuts are coming and want to weigh both sides, our breakdown of whether the Fed will cut rates in 2026 is a useful companion read. And if your real question is “should this money even be in bonds or just in cash?”, compare the options in short-term bonds vs. high-yield savings.

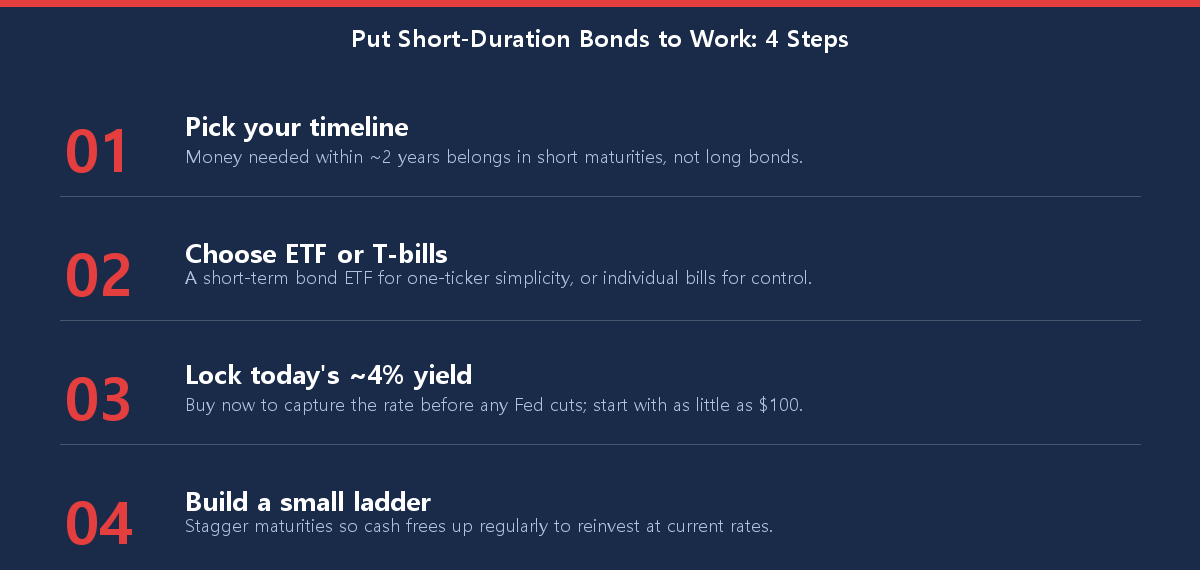

How to Put Short-Duration Bonds to Work

You don’t need a bond desk or a six-figure account to do this. The mechanics are simple, and you can start with as little as $100. Walk through the steps below to build a short-duration position that fits your timeline.

Many investors prefer a short-term Treasury or bond ETF for the simplicity — one ticker, automatic reinvestment, and instant diversification across dozens of maturities. Others build a small “ladder” of individual T-bills so that something matures every few months, giving them regular chances to reinvest at current rates. Either way, the practical steps for buying are covered in our guide on how to buy US Treasury bonds.

Three Mistakes to Avoid With Short-Duration Bonds

- Reaching for yield by going long. Stretching to the 30-year for an extra 0.9% is the classic trap — you take on enormous price risk for income you can nearly match at 2 years.

- Forgetting the maturity wall. If you hold individual bills, plan for what happens when they mature; idle cash earning nothing quietly erodes your edge.

- Ignoring the state-tax break. Treasury interest is exempt from state and local tax, which can make a short T-bill beat a savings account paying the same headline rate.

Conclusion: Get Paid to Be Patient

The case for short-duration bonds in 2026 isn’t a market call or a clever trade — it’s a recognition that the math has changed. When the short end of the curve pays roughly 4%, you no longer have to reach for long maturities and stomach gut-wrenching price swings to earn a respectable return. You can collect almost the same yield with a fraction of the duration risk, keep your principal stable, and stay flexible enough to react when the Fed finally moves. In a 4% Treasury world, the smart money isn’t chasing the long end — it’s getting paid to stay patient and short. If you’re still building the foundations, start with where your cash should actually live and grow from there.

Found this helpful? Bookmark it and check back as the rate picture shifts — the right duration for your money changes as the Fed does.

This article is for informational purposes only and is not investment advice. Do your own research.