Rising interest rates don’t just affect your mortgage payment — they quietly reshape the risk profile of every asset you own. In 2026, with the Fed signaling a higher-for-longer rate path and the 10-year Treasury yield holding above 4.5% (Source: U.S. Treasury, as of July 2026), many investors who haven’t rebalanced in a year or more are sitting on allocations that no longer match their original plan. This guide walks through exactly how to rebalance your portfolio when interest rates are rising — step by step, with specific actions you can take this week.

Why Rising Rates Throw Your Portfolio Off Balance

Most investors know that rates and bond prices move in opposite directions. What surprises many people is how much portfolio drift can accumulate across all asset classes, not just bonds, during a sustained rate cycle.

The bond price paradox — why your bond fund is down

When the Fed raises rates, newly issued bonds offer higher yields. That makes your existing bonds — locked in at lower rates — less attractive to buyers, so their prices fall. A long-duration bond fund like BND or AGG can drop 10–15% in a single rate-hiking cycle. A short-term T-bill fund? Barely moves. Duration — the sensitivity of a bond’s price to rate changes — is the number you need to understand before you rebalance.

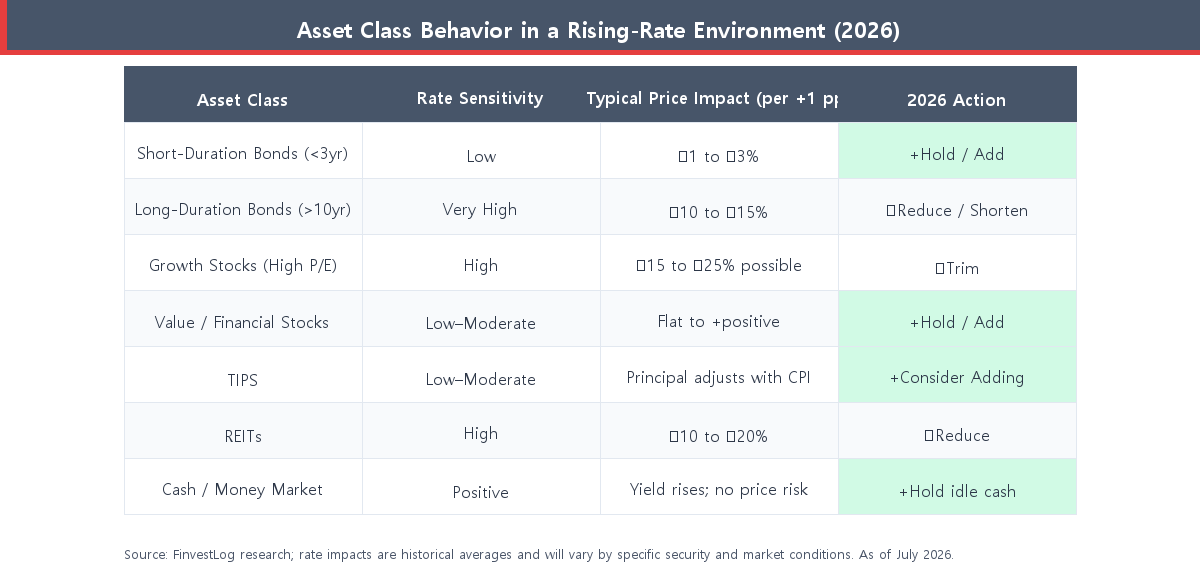

Rate sensitivity by asset class: a quick-reference matrix

Interest rates don’t just hit bonds. Growth stocks with high price-to-earnings multiples get compressed because their future earnings are discounted at a higher rate. Real estate investment trusts (REITs) often fall because their debt costs rise. Meanwhile, financial stocks and energy companies can benefit from higher rates. Understanding how each asset class behaves is the foundation of a rate-aware rebalancing strategy.

If your portfolio hasn’t been touched since a low-rate era, there is a good chance it is now overweight long-duration bonds and rate-sensitive growth equities — two of the weakest performers in a rising-rate environment. The first step is to see exactly where you stand.

Before You Rebalance — Audit Your Current Allocation

Pull your actual numbers (most people are surprised)

Log into every account you own — 401(k), IRA, brokerage, HSA — and record the current market value of each holding. Group them into categories: US stocks, international stocks, bonds (short vs. long duration), real assets, and cash. Calculate each category as a percentage of your total portfolio. Many investors discover their “60/40” portfolio has drifted to something closer to 72/28 after a strong equity run. That gap matters enormously in a higher-rate environment.

If you are building a portfolio from scratch or want to revisit the fundamentals of how to split money across asset classes, A Beginner’s Guide to Asset Allocation covers the core framework and age-based allocation guidelines.

Set your target allocation with rate risk in mind

Your target allocation should reflect your time horizon and risk tolerance — not the current rate environment alone. What the rate environment should change is your composition within each asset class, particularly within the bond sleeve. Define your target percentages now, before you start selling anything. Write them down. This document becomes your rebalancing rulebook.

Step 1 — Shorten Your Bond Duration

Why long-duration bonds hurt most when rates climb

Duration measures how many years it takes to recover a bond’s cost through its cash flows. A 20-year Treasury bond has a duration of roughly 15 years — meaning its price falls about 15% for every 1 percentage point rise in rates. A 2-year T-bill? Its duration is roughly 2 years, so the same rate move only costs you 2% in price. In a rising-rate environment, duration is risk. Shorter duration means less price sensitivity and the ability to reinvest at higher yields sooner.

ETF swaps: moving from BND to shorter-duration alternatives

A practical move for many investors is shifting part of their aggregate bond fund position into a short-term alternative. Instead of holding the entire bond allocation in BND (Vanguard Total Bond Market, average duration ~6 years), consider tilting toward BSV (Vanguard Short-Term Bond, ~2.7 years) or SPTS (SPDR Portfolio Short-Term Treasury, ~1.9 years). This is not a market-timing call — it is a duration-management decision aligned with your risk tolerance. For context on where T-bill yields stand relative to savings account rates, see Short-Term Bonds vs. High-Yield Savings Accounts (2026).

Step 2 — Rotate Within Equities for Rate Resilience

Trim high-multiple growth, add value and financials

Growth stocks — particularly tech and consumer discretionary — often carry price-to-earnings ratios of 30× or higher. When rates rise, those high multiples compress because investors can earn more in safer assets. Value stocks (financials, energy, industrials) tend to hold up better because their earnings are more near-term and their valuations leave less room to compress. Tilting your equity allocation from pure market-cap index weight toward value does not mean abandoning diversification — it means acknowledging that rate environments change the relative attractiveness of segments within the equity universe.

Adding inflation protection: TIPS and real assets

If your portfolio has no inflation-protected allocation, a rising-rate environment — often accompanied by elevated inflation — is the right moment to consider adding TIPS (Treasury Inflation-Protected Securities). TIPS adjust their principal with CPI, so their real yield stays intact even when inflation runs hot. For a detailed comparison of TIPS versus I Bonds for 2026, see TIPS vs. I Bonds: Best Inflation Protection for 2026.

Step 3 — Decide When to Pull the Trigger (Calendar vs. Threshold)

The most common rebalancing mistake is not having a clear rule for when to act. Emotion fills the void — and emotion-driven rebalancing is almost always mistimed. There are two proven frameworks, and a combination of both tends to work best.

The 5/10 rule explained

The threshold method means you rebalance only when an asset class drifts beyond a set limit from its target. A commonly used rule is the 5/10 rule: rebalance when any asset class drifts more than 5 percentage points from its target (relative) or more than 10 percentage points in absolute terms. For example, if your target bond allocation is 40% and it has fallen to 34%, that 6-point gap crosses the 5 pp threshold and triggers action. This approach ensures you only rebalance when drift is meaningful — not in response to every market wiggle.

Calendar rebalancing (reviewing once a year, typically in January or after a major life event) is simpler to stick with and avoids transaction overload. Combining both — annual review with threshold guardrails — gives you structure plus a safety valve for sharp market moves like a sudden rate spike.

Using new contributions to rebalance passively

Before selling anything, direct new contributions toward your underweight asset classes. If stocks are overweight and bonds are underweight, put your next paycheck contribution entirely into the bond fund. This achieves the same rebalancing effect without triggering any taxable event. It is the most tax-efficient rebalancing tool available to investors who are still accumulating assets.

Step 4 — Minimize Taxes While You Rebalance

Rebalance in tax-advantaged accounts first

The correct order for rebalancing matters enormously. Start with your tax-advantaged accounts — 401(k), traditional IRA, Roth IRA. Selling and buying within these accounts generates zero immediate tax liability. Move the dial inside these sheltered accounts first before touching your taxable brokerage. If you can achieve your entire target rebalance inside the tax-advantaged bucket alone, you have effectively rebalanced for free from a tax standpoint. Understanding how to structure accounts for this purpose is one of the core arguments for using a Roth IRA or 401(k) as your rebalancing engine.

Tax-loss harvesting to offset any gains

If you must sell appreciated positions in a taxable account, look first for positions sitting at a loss in the same asset class. Selling the loser (realizing the loss) can offset the gain from selling the winner, reducing your net capital gains tax bill. This is called tax-loss harvesting. Be mindful of the wash-sale rule: you cannot repurchase the same or a substantially identical security within 30 days before or after the sale. Switching from one S&P 500 ETF to a comparable but not identical total-market ETF sidesteps this restriction.

Step 5 — Rebuild and Monitor Your Drift Bands

After executing your rebalance, document your new allocation and set your drift bands. A simple annual calendar reminder — “Review portfolio allocation: first week of January and July” — is enough for most investors. If a major market event occurs in between (a sudden 20% equity sell-off, or a rapid 150 bp rate move), check your drift bands against the 5/10 rule. If the drift is within bands, do nothing. Discipline is the point.

The simplest structure to maintain going forward is a low-cost three-fund portfolio with explicit duration management in the bond sleeve. See How to Build a Simple 3-Fund Portfolio in 2026 for a step-by-step setup guide.

Common Rebalancing Mistakes to Avoid in 2026

- Rebalancing too frequently. Monthly rebalancing generates transaction costs and tax friction with little benefit over quarterly or annual reviews.

- Ignoring duration within the bond sleeve. Cutting bonds as a whole class is not the same as managing duration. A portfolio heavy in short-term Treasuries behaves very differently from one holding a 20-year bond fund.

- Chasing rate headlines. The Fed’s stated path and the actual path often diverge. Build a rebalancing strategy that does not require you to predict rate moves — because no one consistently can. For context on where Fed policy currently stands, see Will the Fed Hike Rates in 2026? and How Fed Rate Decisions Affect the Stock Market.

- Selling everything. A 100% cash position has its own risk: inflation erosion and the difficulty of deciding when to re-enter.

- Letting perfect be the enemy of done. A rebalance that gets you from 73/27 to 62/38 is better than waiting for the ideal moment that never comes.

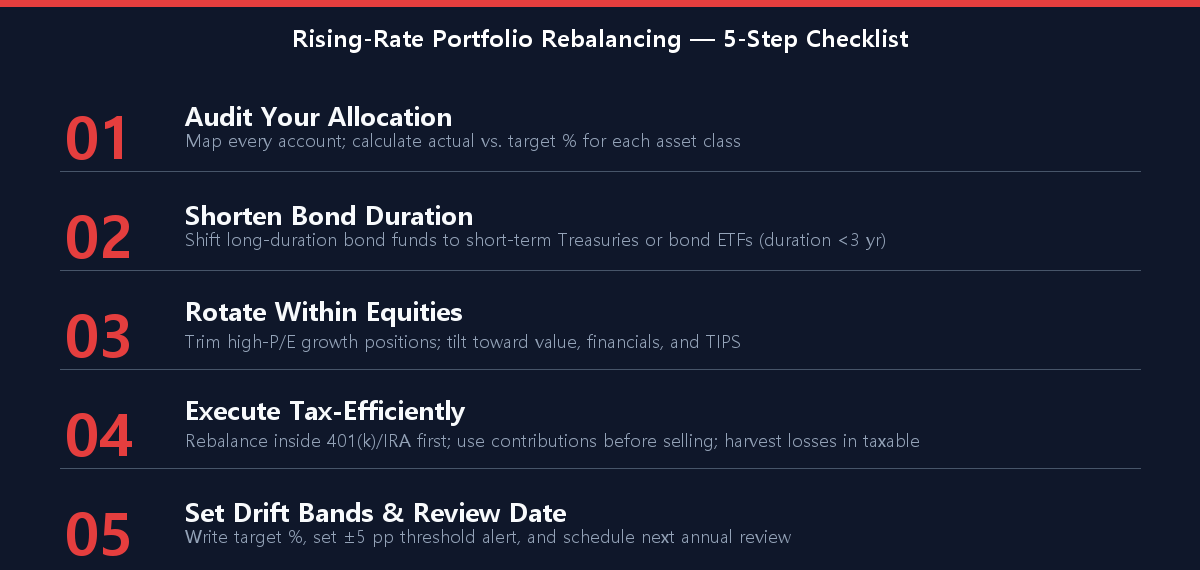

Your Rising-Rate Rebalancing Checklist (Print & Keep)

Use the checklist below as your decision framework each time you review your portfolio. No step should take more than a few hours across a weekend — and for most investors, this annual exercise is the highest-value action they will take all year.

Conclusion

Rebalancing when interest rates are rising is not about predicting the market. It is about systematically maintaining the asset allocation you chose when you were thinking clearly — not in the middle of a rate shock or a market correction. The five steps in this guide — auditing your allocation, shortening bond duration, rotating within equities, executing tax-efficiently, and setting drift bands — form a repeatable framework you can apply in 2026 and in every rate cycle that follows.

Markets move. Rates change. The investors who stay the course with a disciplined, rules-based approach tend to come out ahead of those who try to time each twist. Found this useful? Bookmark this page so you can revisit it the next time a headline about rate hikes lands in your feed.

Worth reading next: Dollar-Cost Averaging vs. Lump-Sum Investing: Which Wins in 2026? — if you are still deploying cash into the market while rebalancing, the DCA vs. lump-sum question matters more than most investors realize.

This article is for informational purposes only and is not investment advice. Do your own research before making any investment decision.