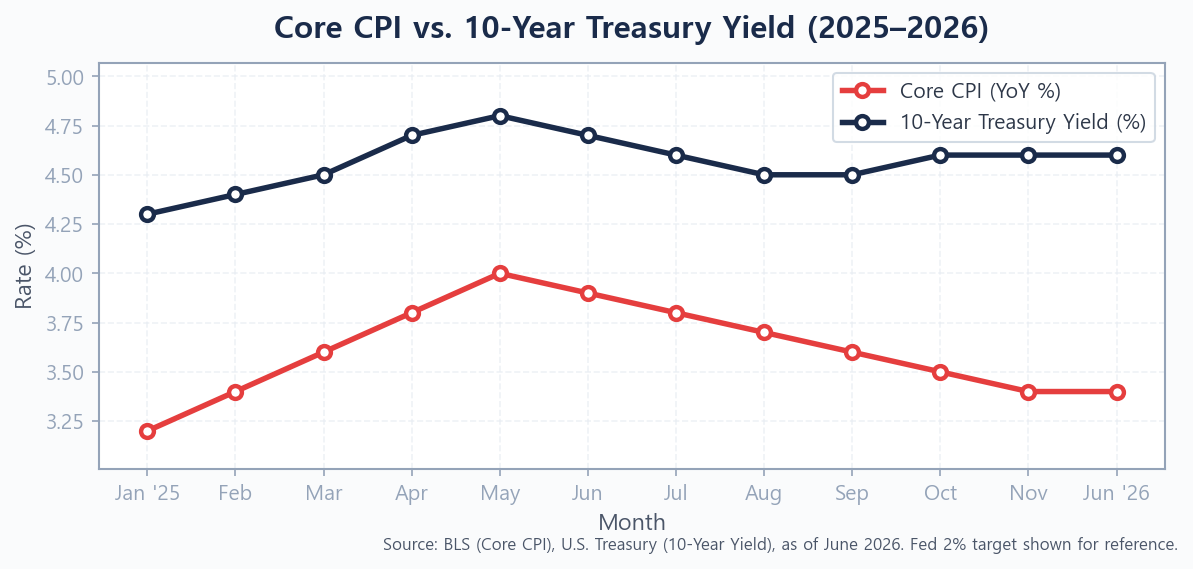

Inflation was supposed to be a 2022 problem. The Federal Reserve raised rates aggressively, supply chains normalized, and by late 2023 the consensus view was that the disinflation path was clear. Then tariffs changed the equation. As of mid-2026, core CPI sits at 3.4% — the highest reading since October 2023 — and the 10-year Treasury yield hovers near 4.6%, forcing bond investors to rethink assumptions they made when the hiking cycle peaked. The culprit, more than any other factor, is tariff-driven structural inflation that refuses to fade.

This guide explains exactly how tariffs are transmitting into persistent price pressure, what that means for bond math, and — most importantly — five concrete moves you can make in your bond allocation today.

Why Inflation Is Still “Sticky” in Mid-2026

The Tariff-to-CPI Transmission Chain

Tariffs work differently from demand-driven inflation. When the economy overheats, the Fed raises rates, demand falls, and prices follow. Tariff inflation is a supply-side shock: costs rise at the import stage regardless of consumer demand. The transmission chain looks like this:

- Import costs rise — tariffs raise the landed price of goods at the border.

- Producer prices climb — businesses absorb some costs, pass the rest to downstream buyers. The Atlanta Fed found that US firms attribute roughly 40% of their total unit cost growth in 2025–2026 to tariffs.

- Consumer prices follow with a lag — companies work through pre-tariff inventory first, then re-price. This lag is why inflation stayed muted in early 2025 and only re-accelerated in late 2025 and into 2026.

- Services inflation lingers — once wages rise to offset higher living costs, services prices rarely retreat quickly, creating the “stickiness” the Fed struggles to address with rate policy.

The result is an inflation regime that isn’t easily killed by keeping the Fed funds rate at current levels. Rate hikes cool demand; they don’t lower the cost of a tariffed steel coil or semiconductor.

What the Numbers Show: Core CPI and PPI in 2026

The data tells a clear story. Core CPI — which strips out food and energy — came in at 3.4% year-over-year in May 2026 (Source: Bureau of Labor Statistics, June 2026). Producer Price Index readings for finished goods remained elevated throughout the first half of the year, suggesting the pipeline for further consumer price pressure is not empty. Meanwhile the Fed’s 2% target remains a theoretical destination rather than an imminent arrival.

How Sticky Inflation Reshapes the Bond Market

Duration Risk Returns — Bond Math 101

Bond prices move inversely to yields. The longer a bond’s duration, the more its price falls when yields rise. In a world where inflation stays above 3% and the Fed signals “higher for longer,” long-duration bonds are exposed to two headwinds at once: yields already elevated and the risk they go higher still.

Consider the math on a 30-year Treasury. A 50-basis-point yield increase on a bond with 18-year modified duration produces roughly a 9% price loss — wiping out more than two years of coupon income. For investors who entered long-duration positions expecting rapid rate cuts, the tariff-inflation reality has been painful. The case for why short-duration bonds make sense right now has never been stronger from a risk-adjusted perspective.

The 10-Year Treasury Yield in Mid-2026: Where We Stand

The 10-year Treasury yield reached 4.6% in late May 2026 — capping its biggest weekly rise in over a year — as investors priced in a stickier Fed path after the May CPI print (Source: Bloomberg, May 2026). Term premium, the extra compensation investors demand for holding long-dated bonds rather than rolling short-term bills, has been rising as fiscal concerns and persistent inflation erode confidence that the Fed will cut aggressively anytime soon.

For a fuller picture of where 10-year yields are likely to move through year-end, see our detailed 10-year Treasury yield outlook for 2026.

The Bloomberg segment above captures the exact market reaction to the May 2026 inflation surge — a useful real-time illustration of the mechanism we’ve been describing before we turn to the tactical playbook.

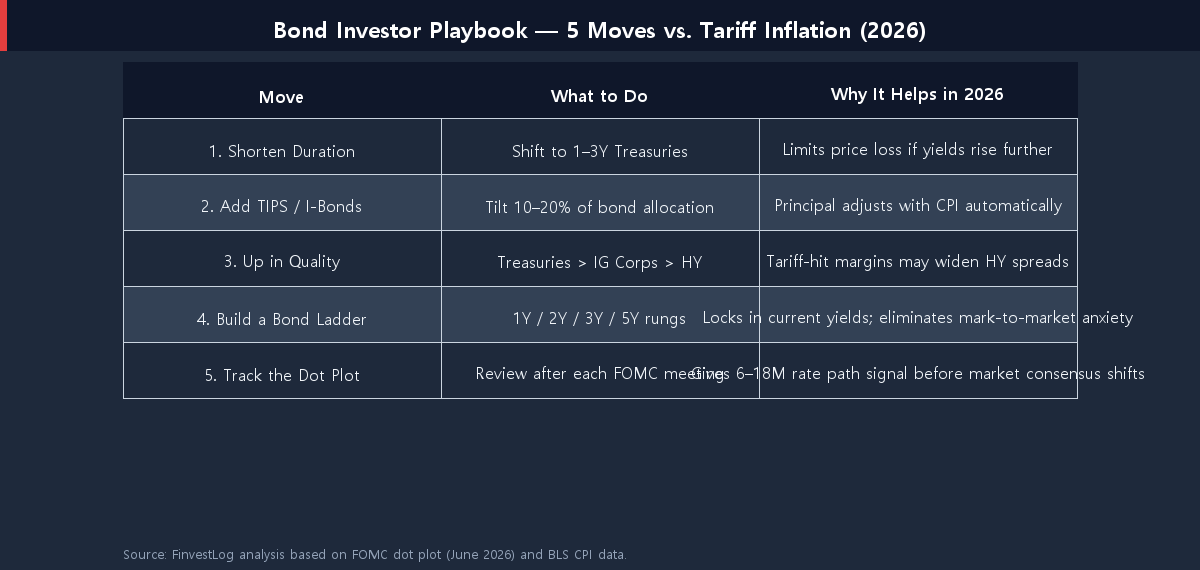

5 Tactical Moves for Bond Investors Right Now

The following moves are not a single prescription — different investors hold bonds for different reasons (income, stability, diversification). Think of these as a prioritized menu based on the current tariff-inflation environment.

1. Shorten Duration Aggressively

If your bond allocation skews toward 10-, 20-, or 30-year maturities, the risk/reward has shifted unfavorably. Short-term Treasuries — 3-month to 2-year maturities — currently yield nearly as much as long bonds (the yield curve is flat to slightly inverted in 2026), while carrying a fraction of the duration risk. You give up almost nothing in yield while eliminating the price-loss exposure to a further rate rise.

For a structured look at the short-end opportunity, read our piece on why short-duration bonds make sense right now.

2. Tilt Toward Inflation-Protected Securities (TIPS and I-Bonds)

TIPS (Treasury Inflation-Protected Securities) adjust their principal with CPI, meaning the real yield is what you actually earn after inflation. With core CPI above 3% and real yields on 10-year TIPS near 2%+, TIPS now offer a meaningful inflation buffer without sacrificing quality. I-Bonds remain an option for smaller allocations, with the fixed rate component now at a competitive level relative to recent years.

The choice between the two depends on your time horizon, purchase limits, and liquidity needs. Our TIPS vs. I-Bonds: which inflation hedge wins in 2026 breakdown covers the comparison in detail.

3. Stay Up in Quality — Treasuries Over High Yield

When tariffs slow economic growth while keeping inflation elevated — the dreaded “stagflation lite” scenario — corporate credit spreads tend to widen as default risk rises. High-yield bonds that look attractive on a nominal yield basis can underperform badly if credit quality deteriorates. In 2026, the quality premium of Treasuries over corporate bonds is a rational trade-off, not just a conservative instinct.

Investment-grade corporates occupy a middle ground — they currently pay around 1 percentage point over comparable Treasuries, but that spread may not adequately compensate if tariff-driven margin compression spills into earnings. See our analysis of corporate bonds vs. Treasuries for the full spread picture.

4. Build or Extend a Treasury Bond Ladder

A bond ladder — owning individual Treasuries maturing at regular intervals — solves two problems simultaneously. First, it locks in current yields rather than leaving you exposed to reinvestment risk if rates fall. Second, it removes price-mark-to-market anxiety: held to maturity, a Treasury returns 100 cents on the dollar regardless of what yields do in the interim.

At current yield levels, a laddered portfolio of 1-, 2-, 3-, and 5-year Treasuries can deliver a blended yield of roughly 4.3–4.6% while maintaining high liquidity and zero credit risk. We walk through a real $100,000 ladder example in our Treasury bond ladder vs. bond ETF comparison.

5. Watch the Fed’s Dot Plot, Not Its Headlines

The Fed communicates through press conferences, but it signals through the dot plot — the quarterly projection of where each FOMC member expects the fed funds rate to go. In June 2026, the dot plot shifted toward fewer cuts than markets had priced in, driven by sticky core inflation data. Following the dot plot gives you a 6-to-18-month rate path estimate that is more reliable than parsing Chair press conference language.

If the dot plot shows rates staying above 4.5% through 2027, the case for long-duration bonds remains weak. If tariffs are reduced or CPI surprises to the downside, the dot plot will shift too — and that’s when adding duration becomes a better trade. Our piece on Will the Fed hike rates in 2026? tracks the current dot plot in detail.

Two Scenarios to Stress-Test Your Portfolio

Bond strategy should be built around probability-weighted scenarios, not a single forecast. Here are the two scenarios most relevant for tariff-driven inflation in 2026.

Bull Case: Tariffs Rolled Back, CPI Falls Below 3%

If trade negotiations succeed in rolling back the most economically damaging tariffs — especially those targeting consumer electronics and finished goods — the import-cost pressure eases. CPI has a clear path toward 2.5%–3% by Q1 2027, and the Fed regains room to cut. In this scenario, long-duration bonds outperform dramatically: a 100-basis-point yield decline would produce a ~15% price gain on a 15-year duration bond. Short-term bills underperform as their coupons reset lower.

Probability assessment: possible, but requires a significant political shift. Maintain some long-duration exposure as an option on this scenario, not as a core positioning.

Bear Case: Tariffs Expand, CPI Re-accelerates Past 4%

If retaliatory tariffs broaden, supply chain adjustments prove inflationary rather than deflationary, and a wage-price loop begins, CPI could re-accelerate to 4%+ by late 2026. The Fed would be forced to consider additional hikes. The 10-year yield could push toward 5–5.5%, and long-duration bond holders would face severe mark-to-market losses. Short-duration Treasuries, TIPS, and money market funds would be the clear winners.

This scenario makes the case for robust bond portfolio rebalancing now. For a step-by-step framework on how to reposition, see our guide on how to rebalance your portfolio in a rising-rate environment.

Frequently Asked Questions

Are tariffs more inflationary than demand shocks?

In terms of Fed response options, yes — supply-side inflation from tariffs is harder to cure with interest rates alone because rate hikes suppress demand without addressing the cost input. This is why the inflation from the 2025–2026 tariff cycle has proven stickier than initially expected.

Should I avoid bonds entirely in a sticky-inflation environment?

No. Bonds still provide portfolio stability and income. The key is to own the right bonds — shorter duration, higher quality, inflation-protected where appropriate — rather than abandoning fixed income altogether. Even in a 4.5% yield world, bonds diversify equity risk meaningfully.

When will long-duration bonds become attractive again?

When the Fed either cuts rates or signals a credible path to cuts — driven by CPI clearly trending back toward 2.5% or below, or by economic weakness forcing the Fed’s hand. Watching core CPI monthly and the quarterly dot plot will give you earlier signals than any market commentator.

What about bond ETFs vs. individual bonds?

ETFs offer liquidity and diversification but don’t hold to maturity, meaning their NAV fluctuates with yields. Individual Treasuries eliminate that price risk if held to maturity but require more capital and management. The right choice depends on your account size and income timing needs.

The Bottom Line

Tariffs are not a temporary shock that bond markets will simply wait out. They represent a structural shift in the cost of imported goods that is proving persistently inflationary — and the data from mid-2026 confirms that core CPI remains far above the Fed’s 2% target as a result. For bond investors, the playbook is clear: shorten duration, tilt toward inflation protection via TIPS or I-Bonds, stay up in quality, consider a ladder at current yields, and track the Fed dot plot for signals that the calculus has changed.

The worst outcome for a bond investor in 2026 is holding long-duration bonds on the assumption that inflation will quickly normalize, while tariffs continue to keep it elevated. Position defensively for the base case, and keep some optionality for the bull case where tariffs are rolled back. That balance — not a binary bet — is what durable bond portfolio management looks like in a tariff-inflation world.

Found this useful? Bookmark it so you can revisit when the market moves. I publish practical investing breakdowns regularly — check back soon.

This article is for informational purposes only and is not investment advice. Do your own research before making any investment decisions.