The Fed cut rates three times in 2025, bringing the federal funds rate down to 3.50–3.75%. For dividend investors, that stretch felt comfortable — yields looked attractive, REITs recovered, and SCHD surged 26% over the following twelve months. Now the script has flipped. The June 2026 dot plot signals one to two potential rate hikes ahead, and the 10-year Treasury yield is hovering between 4.5% and 4.75% (Source: U.S. Treasury, as of July 2026). Understanding what rising Fed rates mean for dividend stocks — and what to actually do about it — can be the difference between defending your income and watching it erode.

This guide breaks down the mechanics of how Fed rate hikes pressure dividend stocks, identifies which categories hold up best historically, and walks through three concrete strategies to protect your dividend income in the months ahead. For broader context on where rates are headed, see our full analysis: Will the Fed Hike Rates in 2026?

How Rising Fed Rates Squeeze Dividend Stocks

Rate hikes don’t hurt all dividend stocks equally, but the pressure they create is real and runs through three distinct channels: yield competition, discount rate expansion, and higher borrowing costs. Most dividend investors focus only on the first — and get blindsided by the other two.

The Bond Yield Competition Effect

When the 10-year Treasury yield climbs toward 4.75%, it competes directly with dividend yields. A stock yielding 3.5% (like SCHD) looks less compelling against a risk-free government bond yielding nearly the same amount. Investors don’t have to take equity risk to earn a comparable payout, so capital migrates toward bonds. The result: dividend stocks see valuation compression even if underlying earnings are healthy.

This is exactly the dynamic that historically ends dividend-stock leadership cycles. Analysis of SCHD’s price behavior suggests that if the 10-year breaks sustainably above 4.75%, the ETF’s recent outperformance over the S&P 500 tends to reverse. SCHD’s current yield of ~3.5% provides diminishing cushion as Treasury yields climb. For a deeper look at how Fed rate decisions affect the stock market across all equity categories, that post covers the four core transmission channels in detail.

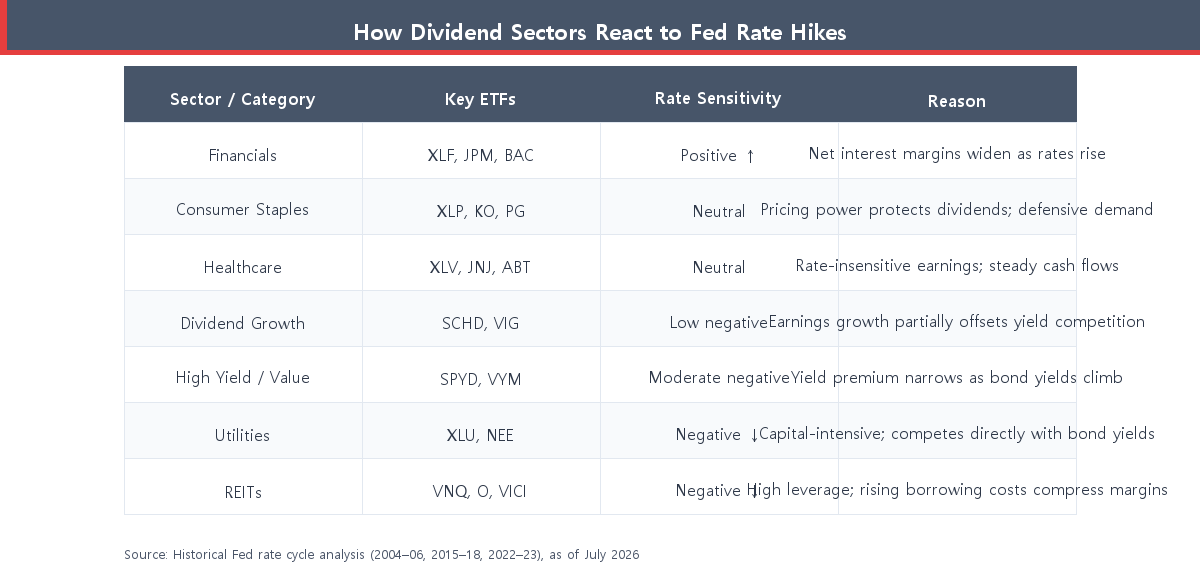

Sectors Hit Hardest — REITs and Utilities

Not all dividend sectors are created equal when rates rise. Two categories face compounded headwinds:

- REITs: Real estate investment trusts carry heavy debt loads. When borrowing costs jump, margins compress and refinancing becomes painful. During the 2022 rate-hike cycle — the sharpest in four decades — VNQ (the broad REIT ETF) fell roughly 26%. That’s not just price pain; it’s a signal that the income thesis was temporarily impaired.

- Utilities: Capital-intensive by nature, utilities borrow constantly to fund infrastructure. Rising rates increase those financing costs, and their relatively stable (but unspectacular) dividend yields lose appeal against risk-free alternatives. XLU underperforms in a Fed-tightening environment more often than not.

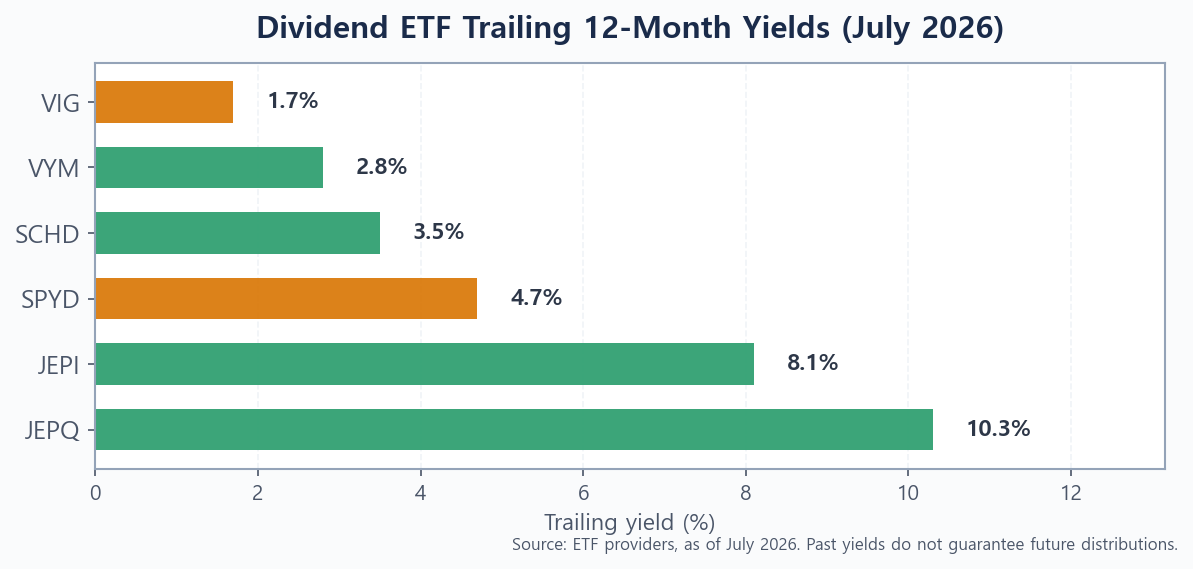

High-yield-focused ETFs like SPYD (trailing yield ~4.7%) are disproportionately loaded with REITs and utilities. That concentration means they face the steepest headwind when the Fed signals a hawkish pivot. See our SPYD vs VYM vs SCHD comparison for a full breakdown of how each ETF’s sector mix positions it in different rate environments.

Which Dividend Stocks Hold Up When Rates Rise?

History offers a clear answer: dividend growth companies outperform high-yield names during Fed tightening cycles. The key is that earnings growth, not a static yield, is what sustains and grows the payout. This video stress-tests the thesis across every Fed rate shock since 2000:

The bar chart above highlights a key insight: yield alone doesn’t tell you which ETF is rate-resilient. JEPQ’s 10.3% distribution is generated largely through options writing, not underlying dividend growth. VIG’s 1.7% yield, on the other hand, comes from companies with 10+ consecutive years of dividend increases — earnings-compounders that can keep raising payouts even when the Fed hikes.

Dividend Growth ETFs: The Rate-Resilient Choice

SCHD and VIG screen their holdings for consistent dividend growth rather than maximum current yield. In a rising-rate environment, this distinction matters enormously. Companies raising dividends year after year typically have the pricing power and cash flow strength to absorb higher borrowing costs. Their stock prices may still face short-term pressure from valuation re-rating, but their underlying income streams remain intact — and often keep growing.

SCHD’s screen requires 10 consecutive years of dividend payments and applies filters on cash flow to debt, return on equity, and dividend growth rate. That quality tilt has helped it deliver roughly 19% year-to-date through mid-2026, far ahead of the S&P 500’s ~7% gain (Source: ETF provider data, as of July 2026). For a detailed head-to-head on quality versus yield, our SCHD vs VIG comparison is the right next read.

Financials — the One Sector That Actually Benefits

Here’s the counterintuitive part: one major dividend-paying sector actually does better when rates rise. Banks and diversified financials (XLF) widen their net interest margins as borrowing costs increase — they earn more on loans while deposit rates adjust more slowly. JPMorgan, Bank of America, and similar institutions have seen earnings estimates revised upward with each hawkish Fed signal in 2026.

Financials carry modest dividend yields (typically 2–3%), but their total return during rate-hike cycles has historically compensated. An allocation shift toward XLF or individual financial names can partially hedge rate risk while keeping equity exposure.

3 Strategies to Protect Your Dividend Income in 2026

Understanding the risk is one thing. Here are three concrete moves dividend investors are considering to defend their income as rates potentially move higher. As always, assess your own situation and timeline before making any changes — and consider reading our step-by-step guide on rebalancing when interest rates are rising before executing.

1. Rotate Toward Dividend Growth ETFs

If your portfolio is heavy in SPYD, VNQ, or utility stocks, a partial rotation toward SCHD or VIG shifts your exposure from yield-chasing to earnings-compounding. You give up some current yield — SCHD’s 3.5% versus SPYD’s 4.7% — but you gain quality companies that have consistently raised dividends through previous rate cycles. The total return history since 2012 consistently favors quality over raw yield across most market environments.

This doesn’t require selling everything. Even shifting 20–30% of a SPYD or VNQ allocation into SCHD meaningfully reduces rate sensitivity while keeping your income base largely intact. Our full Best High-Yield Dividend ETFs for 2026 roundup covers the complete opportunity set if you’re shopping for alternatives.

2. Trim Rate-Sensitive Positions (REITs, Utilities)

Not all REIT or utility exposure is bad — but sizing matters. A 20–30% REIT allocation, common in income-focused portfolios, carries meaningful downside risk if the Fed hikes twice and the 10-year breaks 4.75%. Consider trimming to 10–15% and reinvesting the proceeds into shorter-duration bonds or dividend growth equities.

Within utilities, companies with regulated monopoly businesses and multi-year rate cases locked in (NextEra Energy’s regulated Florida utility segment, for example) hold up better than merchant utilities exposed to spot power prices. Screening at the individual holding level — rather than simply exiting XLU entirely — can preserve your best utility names while reducing the most rate-sensitive exposure.

3. Add Covered Call ETFs for Buffered Income

Covered call ETFs like JEPI (trailing yield ~8.1%) and JEPQ (~10.3%) generate income from options premiums on equity holdings. In a sideways or modestly declining market — which often accompanies a Fed-tightening cycle — the options premium provides a significant income buffer that partially offsets price pressure. The tradeoff is capped upside: if dividend growth stocks surge, covered call ETFs participate only partially.

A 10–15% allocation to JEPI or JEPQ as a complement to a SCHD core can boost overall portfolio income while reducing pure price-return dependency. For a full analysis of how these ETFs work and what to watch out for, see our Best Covered Call ETFs for Monthly Income post.

The Bottom Line

Rising Fed rates don’t mean dividend investing stops working. They mean which dividend stocks you hold starts to matter far more than it did when rates were near zero. REITs, utilities, and pure high-yield plays face the sharpest headwinds. Dividend growth companies — those compounding their payouts year after year — have historically demonstrated the resilience to navigate tightening cycles without sacrificing income. Financials are worth a closer look as a rate-beneficiary segment.

The three-part playbook — tilt toward dividend growth, right-size rate-sensitive sectors, and consider covered call income buffering — is not about abandoning dividend investing. It’s about making sure your income strategy is built for the rate environment that’s actually in front of you, not the one from 2024.

Found this useful? Bookmark it so you can revisit when the market moves.

This article is for informational purposes only and is not investment advice. Do your own research.